Call option volume is skyrocketing:

Call options now reflect 70% of total options market volume, the highest in at least 4 years.

Since early April, this percentage has risen +25 points, the largest 2-month increase on record.

This also exceeds the previous brief surge of ~68% seen in late 2025.

To put this into perspective, the average over the last 2 years was ~55%.

Furthermore, the total notional value of S&P 500 call options relative to the S&P 500's market cap is up to a record 4.1x, doubling over the last 2 months.

Bullish appetite is rapidly surging.

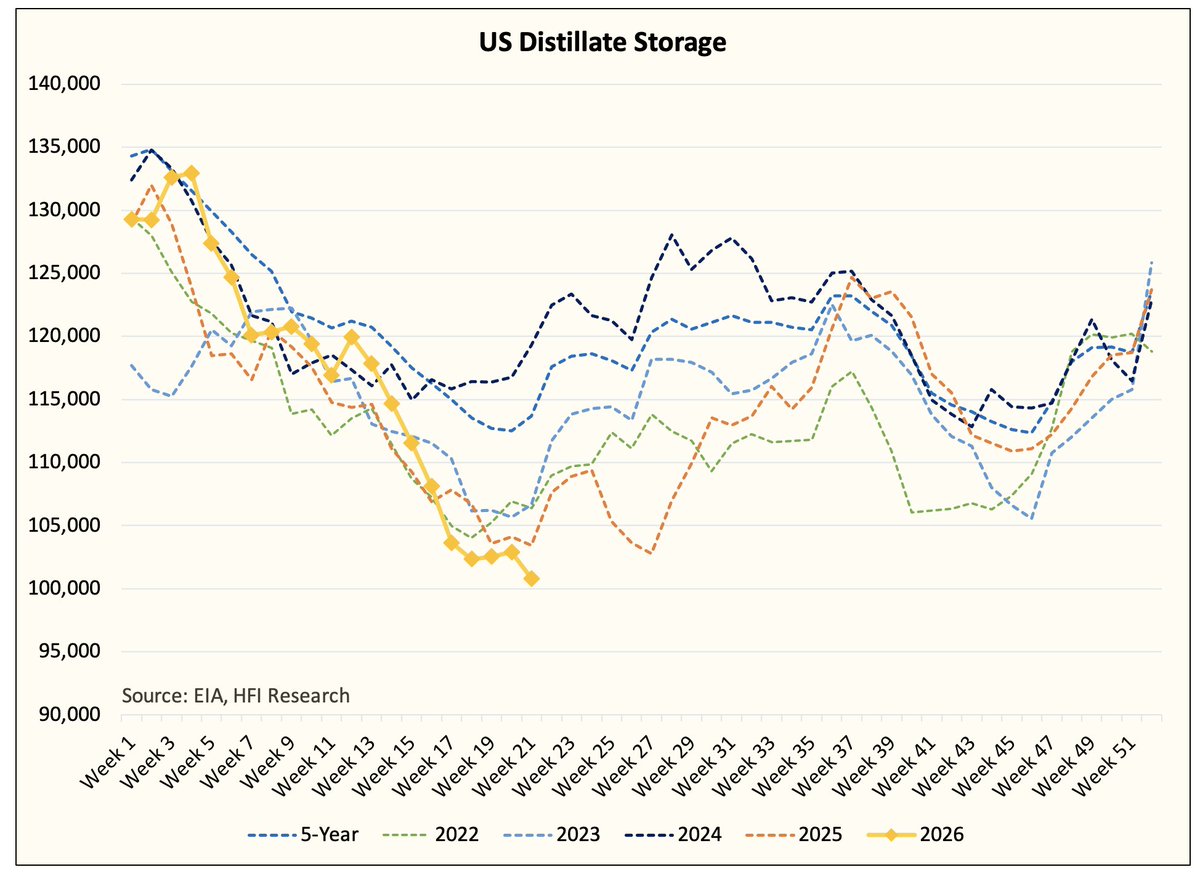

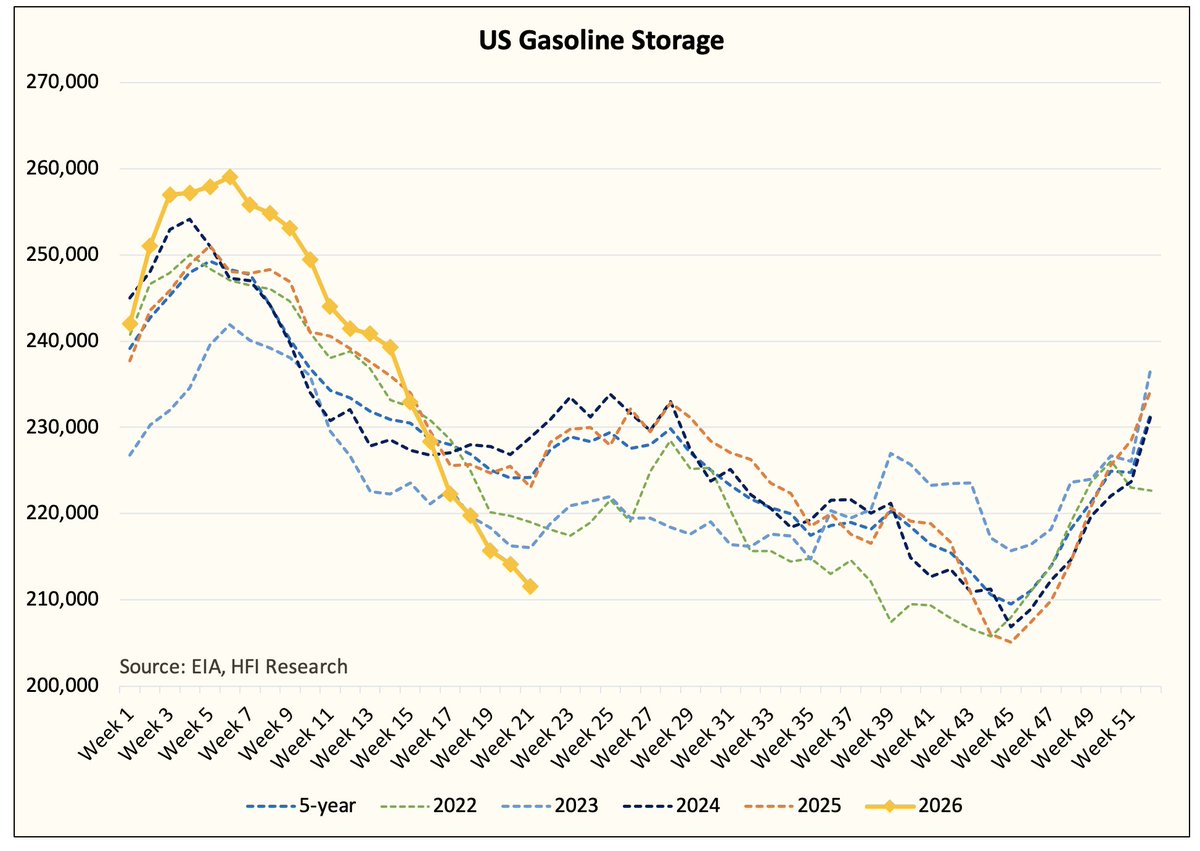

We are ~9 million bbls away from hitting a storage level that's the equivalent of living paycheck to paycheck for gasoline and distillate.

Once we get there, even a minor disruption (any sort of outage) will result in gasoline lines at gas stations.

I guess we are really doing this.

@macrocephalopod I subscribe to the recommendations from OP, what would you recommend going beyond all those?

what do you think about a list like this:

The Misbehavior of Markets: A Fractal View of Financial Turbulence by Mandelbrot

Why stock markets crash by Sornette

The second leg down

3/4

But if the y-axis is extended to the NEXT (future) 5-year REAL (after inflation) return, then THERE IS NO EXAMPLE, OVER THE LAST 150 YEARS, OF THE STOCK MARKET BEATING INFLATION OVER THE NEXT 5-YEARS WHEN THE CAPE IS ABOVE 34.

Restated, valuation is an expectation tool. Unless one makes the case that corporate earnings are going to have their most significant surge in history, the stock market is destined to disappoint over the next several years.

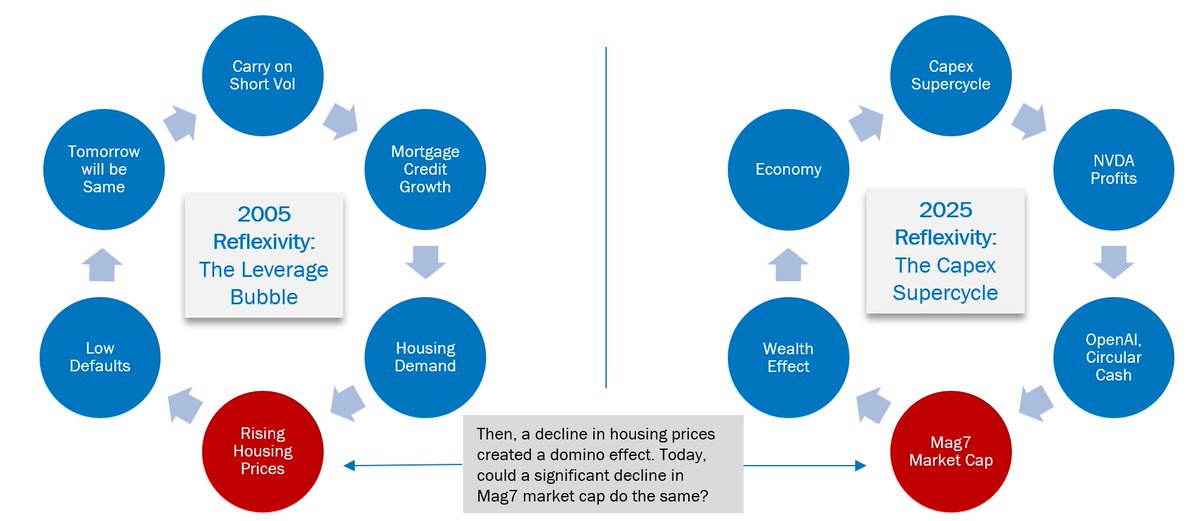

TLDR: the economy --> market feedback loop today is similar to that of the pre-GFC period. It's the market that will take the economy down, not vice versa as is traditionally the case.

Today's SPX can be summarized as "highly concentrated with highly volatile, highly valued but remarkably uncorrelated tech stocks".

A good argument can be made that the market is not properly identifying the linkages, cross-holdings, investments, and extent to which customer/supplier relationships underpin the correlation in outcomes for AI focused stocks. We are still in the leveraging period and stock price changes have been vastly idiosyncratic.

A similar argument could be made for home prices in pre-GFC era. Housing price appreciation was clearly driven by a common factor: the bottomless extension of mortgage credit. But that did not show up in city to city correlations until there was a break in the circularity. Once defaults picked up, the credit machinery failed and the correlation of housing prices surged.

In the aftermath of large drawdowns, investors consistently realize they’d underestimated the degree of “sameness” in assets. It took us until 2008 to recognize that the huge run up in housing prices was linked to a common driver: the vast supply of mortgage credit.

Today, are we missing the vulnerability to a Mag7 sell-off? The negative wealth effect would be substantial. If market cap is the “currency” to fund Capex and that same Capex is driving economic growth, a sell-off in Mag7 has multiple pathways for spill-over.

Below, a few pieces picking up on the same idea.

Construction employment has been rolling over and every piece of anecdotal evidence we have suggests it’s getting worse. That typically means elevated recession risk and has never ever meant economic reacceleration:

This is an excellent article to understand what @SteveMiran is all about.

This opening and closing paragraph struck a chord with me. I have called the US economy post-COVID, which follows on it previously being post-Crisis (2008). We need to understand how things are working now. I have short-handed this as "we are not going back to 2019."

---

From the Compact opening (about Miran):

The problem with the Fed isn’t wrong technique or bad data, he suggested, but rather that the very structure of its models is embedded in the economic and political assumptions of a bygone era. The world the forecasts are trying to measure no longer exists.

---

I hope Jay Powell and the Fed staff are carefully listening to Steve, because these statements by Powell are at the heart of the post-COVID policy errors.

January 31, 2024. Powell said, “The economy is broadly normalizing, and so is the labor market—but not totally back to normal."

Powell's statement is based on a belief that we not only can return to "2019" but are actively doing so. Is this the correct model of the economy for the Fed? Or are they from a previous cycle that no longer applies?

I agree with Miran that the Fed models are wrong (which is why I have also been critical of the most prominent defender of the old status quo models, New York Fed President John Williams)

What are the new models? Here we can debate. But let's at least acknowledge that the current models (i.e., Williams R*) and rules need to be revamped.

The article concludes with this.

---

From the Compact (my emphasis):

Whether Miran’s prescriptions will work is another question. Perhaps his arguments are incorrect and his predictions wrong. But they point to a deeper reality: The neoliberal order that kept markets and politics apart is gone. If we are living through a transformation in capitalism, it would behoove us to consider the urge behind this need for new economic thinking and why it is plausible. To return to Miran’s injunction, we should take him seriously, not literally.

Will have various responses later but I invented your day job:

https://t.co/5wy1zQDnzT

https://t.co/f4hP2Mbfzu

https://t.co/OZLJDGsdDv

https://t.co/WOz5zeGZsP

We literally invented the “charge less and do the simple hedge fund strategy” idea. But we actually do the strategies, we don’t “replicate” them with a few securities or just copying other’s positions as that has always been nonsense. And we charge barely any more than the “replicators.” 95-100 basis points for “replication” is a rip-off. A rip-off while lecturing me is mildly annoying.

In recent years (5-10 years was the research, new stuff has only been trading for a few years, hard to get nuance across on TV) we just figured out how to make it better (we believe we did — compliance makes me add those kind of weasel words). And that annoys some people. Particularly those who’s entire business model is disagreeing while hypocritically accusing others of ignoring their intellectual foundations for their business model.

More later. But here’s one hint. You forgot to regress on the market. You can always argue what factors to put on the RHS of a regression in evaluating performance, but the market should pretty much always be there. Then compare us to SG who love carry/beta too much. Go ahead. I’ll wait.

The debasement trade is a new thing and we're only learning about what it really is in real time. The biggest surprise for me is how quickly the precious metals rally restarted on headlines the government shutdown is ending. A crisis for fiat currencies...

https://t.co/9RhgbAYsLe