Gold miner margins have reached multi-year highs even as sentiment has weakened sharply.

The Sound Money Report guest post by @RonStoeferle shows how this reflects the fundamental picture in IGWT26’s mining chapter.

Full read at @SoundMoneyRpt:

Gold is down roughly 25% from its January high. Sentiment has turned sharply negative.

@GOLDCOUNCIL's survey shows central banks averaged 1,000 tonnes per year over four years, double the prior decade, and 89% expect more. The Dow Theory map says corrections and bearish sentiment are what the accumulation phase looks like from the inside.

The mania phase has not arrived yet.

BREAKING: US margin debt jumped by +$112 billion in May, to a record $1.42 trillion.

This marks the 2nd consecutive monthly increase, totaling +$195 billion.

Margin debt has surged +$495 billion, or +54%, over the last 12 months.

Adjusted for inflation, this metric rose +7.9% MoM and +47.4% YoY.

Real margin debt has now grown +550% since 1997, far outpacing the S&P 500’s real gain of +357.7% over the same period.

Market leverage continues to rise at a historic rate.

I've never had a guest open with this:

"I totally blew the call."

Then @LawrenceLepard doubled down and told me why he's buying more gold right now.

Full interview out now on @KitcoNewsNOW

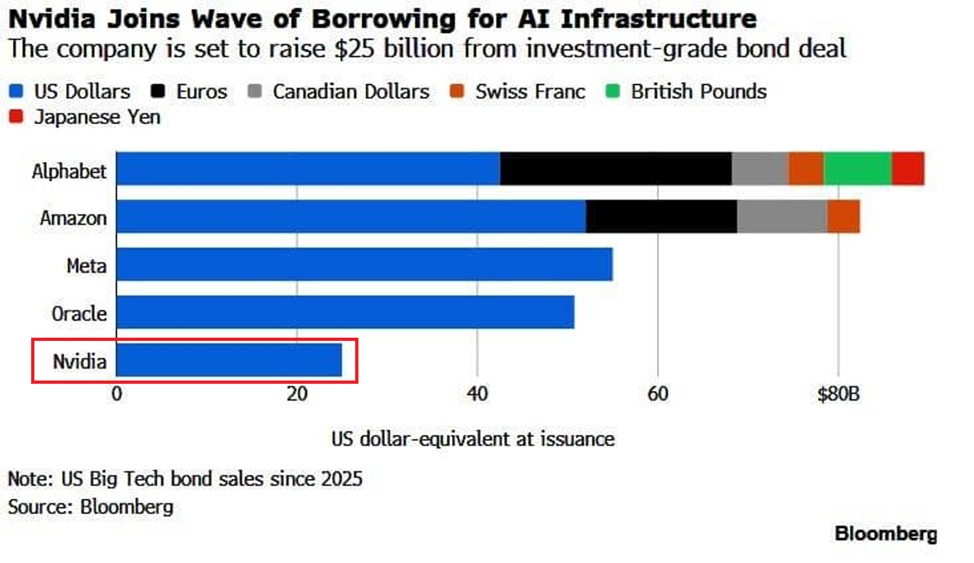

Nvidia is joining the AI debt financing boom:

Nvidia, $NVDA, sold $25 billion of investment-grade bonds on June 15th, its first debt offering since 2021.

This ranks as the 2nd-largest US high-grade bond sale of 2026.

The deal attracted ~$85 billion in investor orders, more than 3 times the offering size, leading the company to increase the offering from an initial target of ~$20 billion.

This follows Alphabet, $GOOGL, Amazon, $AMZN, Meta, $META, Oracle, $ORCL, and Salesforce, $CRM, collectively raising ~$132 billion in investment-grade bonds this year alone.

Debt is becoming a key source of AI infrastructure funding.

The next challenge to dollar dominance won’t start with a currency.

It will start with a payment network.

Project mBridge has already processed $69 billion.

The plumbing of global finance is changing.

Trump is not lying

There is a >$300B reconstruction fund for Iran, but it did not specifically to be paid by US govt. The money will be raised from willing participants (namely GCC) as they are the one who want to restart SOH flow and not get bombed anymore

But it will impact US

GCC do not have infinite wealth. If they spend $300B on Iran reconstruction, they need to cut spending on other areas like

1. Investment in US AI companies and other stocks

2. Buy UST to keep Treasury market afloat

3. Rebuild US military bases devastated in the region

Selling assets in (1) and (2) for liquidity will impact asset value in US, could trigger domino effect

Not spending in (3) will lead to decline of US presence

Even if US taxpayers do not foot the bill, the impact will be felt

With some comparing Trump's Iran deal to Obama's Iran deal, wanted to highlight this section of the 4/17/26 edition of Tree Rings showing Pres. Obama & Sec. State Kerry both saying NOT doing the Iran deal would threaten USD reserve status.

That Obama & Kerry said this within 6 days of each other suggests they had received a talking point memo on the threat to USD reserve status.

@txghost91 I've long said USD would not stop being reserve currency, but UST will cease to be reserve asset.

Pretty much there already.

What data series are you watching on eurodollar balances that you cite above? thx!

With some comparing Trump's Iran deal to Obama's Iran deal, wanted to highlight this section of the 4/17/26 edition of Tree Rings showing Pres. Obama & Sec. State Kerry both saying NOT doing the Iran deal would threaten USD reserve status.

That Obama & Kerry said this within 6 days of each other suggests they had received a talking point memo on the threat to USD reserve status.

Because my newly created “task force” is going to redefine inflation downward allowing us to cut, but saying that would blow my inflation fighting credibility. LL: There, fixed it for you Kevin.

The market is dropping in response to the Fed's first meeting with Kevin Warsh as Fed Chair for one key reason:

We will have far less information going forward.

During the press conference today, Fed Chair Warsh announced that the Fed has "dropped" forward guidance.

He even hinted that the "dot plot" could be changed or eliminated along with all forms of Fed communication, such as the policy statement and press conferences.

In other words, the market will now have less Fed outlook which means more uncertainty.

On top of this, the five new "task forces" established by Warsh were said to have grand objectives with minimal guidance on what to expect.

As markets have repeatedly proven, uncertainty and volatility go hand-in-hand.

The new era of Fed policy will come with more volatility.