Bengaluru Development Minister @krishnabgowda on Thursday announced a special grant of Rs 2,000 crore for upgrading damaged ward roads across five city corporations under Greater Bengaluru Authority (GBA).

Officials have been directed to identify poor roads, prepare estimates, float short-term tenders and begin work immediately, with a target to complete projects within four to six months.

The minister also reviewed Bengaluru’s garbage crisis, directing officials to strictly enforce door-to-door waste collection, mandatory wet-dry waste segregation, GPS tracking of garbage vehicles, and stronger action against littering. A special drive will clear roadside garbage, debris and weeds.

He said visible improvements in waste management should be achieved within three to four months through better implementation of the existing system and greater citizen participation @GBA_office@GBAChiefComm

JNK India Ltd

Concall guidance 25-30% topline with 14-15% Margin.

First New International Order win worth 200cr and few more big orders are expecting soon in 1-2 months from Russia/middle east/US

If these orders are materialize ? 50-60% topline possible, that is huge.

The stock is currently trading near its 21 EMA after a healthy retracement following a strong run-up.

#JNKINDIA

https://t.co/NGohqWznVZ

Man Industries:

The reason I got interested in this company is that they recently pulled of a great strategic acquisition -

National Pipe company (NPC) of Saudi Arabia

The acquisition was done at a very attractive valuation of 1.5X EV/EBITDA.

NPC is highly profitable cash rich company

Not sure how they pulled if off.

But, looks like this can be a game changer for Man Industries.

Also, NPC has approvals for all the marque customers like - Saudi Aramco, Saudi Water Authority,Kuwait Oil Company,Qatar Petroleum,Saudi Water Partnership Company

The acquisition is funded by $70Mn Debt at 6.5% interest and $32Mn internal accruals.

The interesting thing is that NPC generates enough cash to take care of the debt, so it won't put any pressure on Man Industries' standalone balance sheet.

But, this is something which needs to be monitored closely.

-------------

Apart from the acquisition, Man industries is in the process of completion of 2 major capex in next 12 months -

1> Coating facility in Saudi, which allows it to get into high value add high margin business (25%+ EBITDA margins)

2> Stainless steel seamless pipes facility at Jammu - again a high margin high value add business than the tradition LSAW/HSAW pipes.

-----------

I am aware that the promoters' track record is not great and there is some shady stuff which happened. I haven't done enough deep dive on this, will dig further.

But, something to be aware of.

Disc: in watchlist

no buy/sell reco

do your own research

If you have been in Bangalore since a few years, you must have observed the changing climate and reducing green cover in the city.

Many streets in Koramangala and HSR are still so densely green and breezy that one enjoys just walking there without any purpose.

Thanks to the previous generations of Bangaloreans who planted these trees.

Now it's our time to act!

On 27th June, a tree planting drive is being conducted where you will not only get to plant trees, but will also be given refreshments, snacks, etc.

Let's join hands and make the city greener!

Details in next tweet ⬇️

Man Industries

#ManInd#ManIndustries

1000cr order

Domestic+ International

To be executed within 6-9 months

700cr International

4100+cr unexecuted orderbook

Provides good visibility

@SureshKBN Nai Sir, i will be clueless, people like you have helped so much with the process of investing, and it will be difficult to come to terms with when it is gone.

The boring thing keeps winning.

In life, it’s rarely the hacks, shortcuts, or dopamine hits that create extraordinary outcomes. It’s eating clean, sleeping on time, waking up early, reading consistently, exercising regularly, and repeating those habits for years.

The same is true in investing.

The market makes trading look exciting. Every day there’s a new breakout, a new prediction, a new chart pattern, a new reason to act. But wealth is usually built by doing the boring things well—understanding businesses, buying quality companies, staying invested, and waiting patiently for quarterly results to validate the thesis.

Most people overestimate what excitement can achieve and underestimate what consistency can achieve.

The world sells the idea that happiness comes from constant stimulation. Reality often works the other way around. The habits that feel boring today are usually the ones that compound into health, wealth, and peace of mind tomorrow.

Boring doesn’t get likes.

Boring doesn’t go viral.

But boring keeps winning.

The Congress government’s ₹39,000-crore garbage scam in Bengaluru is a clear case of massive corruption. By handing over a 30-year waste management monopoly to a single favored company, this administration has put the city's financial future at serious risk. They have artificially hiked the waste processing fees by 950% from ₹260 to an unjustified ₹2,400 per tonne. It is obvious that this massive price increase is designed to generate thousands of crores in kickbacks. Even worse, the Chief Minister and Deputy Chief Minister completely ignored the red flags raised by the state's own Finance Department, which warned that this deal would bankrupt the civic body. We have to ask: whose pockets are being filled at the cost of Bengaluru’s taxpayers?

@citizensforblr@NammaBengaluroo@CivicOp_india@bengalurupost1@BalagereConnect@WFRising@GBA_office@RisingVarthur@MTH_Rising

#BengaluruGarbageScam #CongressCorruption #SaveBengaluru

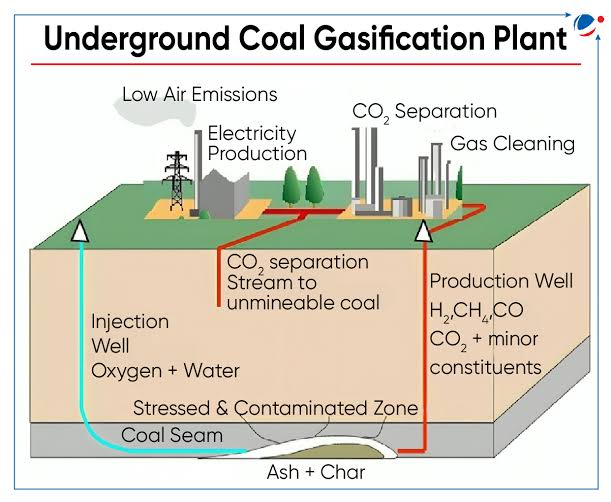

🧵 India's Coal Gasification Value Chain – Listed Stocks Ranked from Feedstock to Chemicals

1. Coal gasification = Coal/Lignite → Syngas → Methanol/Ammonia/H₂ → Chemicals/Fertilizers/Industrial Products.

The biggest winners may not be miners, but companies controlling engineering, conversion & downstream chemicals.

2. NMDC

Primarily a mining giant. No direct coal gasification role today, but could participate in future mineral and industrial ecosystem expansion. Low direct exposure.

3. GMDC

One of the strongest lignite-linked plays. If lignite gasification scales in Gujarat, GMDC becomes a key feedstock supplier.

4. NLC India

Among the most direct beneficiaries. Focused on lignite resources and actively evaluating lignite gasification opportunities.

5. NTPC

Potential future coal-to-syngas, coal-to-hydrogen and coal-to-chemicals operator. One of the highest-conviction long-term plays.

6. Sarda Energy & Minerals

Could become a syngas/hydrogen consumer in steel and ferro-alloy operations. Indirect beneficiary.

7. Godawari Power & Ispat

Industrial consumer angle. Benefits if domestic syngas, hydrogen or ammonia-based inputs become cheaper.

8. Jindal Stainless

Future user of hydrogen/syngas solutions for decarbonization and energy efficiency. Downstream beneficiary.

9. South West Pinnacle Exploration

Coal drilling, exploration and resource development. Benefits if new coal blocks and underground gasification projects expand. Jharkhand coal block allotment in 2027.

10. Asian Energy Services

Field services, exploration and energy infrastructure support. Indirect beneficiary through higher resource development activity.

11. Deep Industries

Gas handling and energy services. Possible supporting role but not a core gasification beneficiary.

12. Prabha Energy

Potential EPC/service participant. Limited direct coal gasification exposure currently.

13. Engineers India (EIL)

One of the most important names in the chain. Feasibility studies, engineering design, FEED and project management.

14. Larsen & Toubro (L&T)

Likely builder of large coal gasification complexes. EPC execution powerhouse.

15. Power Mech Projects

Construction, erection and commissioning opportunities from large gasification projects.

16. SEPC

Potential balance-of-plant construction participant. Smaller exposure versus L&T or Power Mech.

17. Thermax

Utilities, boilers, steam systems, waste heat recovery and environmental solutions. Strong supporting beneficiary.

18. BHEL

India's flagship gasifier and technology player. One of the most important coal gasification stocks overall.

19. JNK India

Process heaters and thermal equipment. Niche equipment supplier to chemical and gasification projects.

20/ Kirloskar Pneumatic

Compressors and gas-handling equipment. Essential supporting equipment supplier.

21/ Elecon Engineering

Coal handling, material movement and conveying systems. Infrastructure beneficiary.

22. IFGL Refractories

High-temperature refractory materials used in gasification and chemical plants.

23. Vesuvius India

Advanced refractory and thermal solutions for high-temperature industrial operations.

24. MSTC

Possible role in coal/resource auctions but negligible direct earnings linkage to gasification.

25. Refex Industries

Very limited direct connection. More of a peripheral energy/environment play.

26. Sustainable Energy Infra Trust

No major direct coal gasification linkage identified currently.

27. Hi-Green Carbon

Focused on recovered carbon black/pyrolysis. Adjacent circular economy theme, not coal gasification.

28. Rashtriya Chemicals & Fertilizers

Major ammonia and fertilizer beneficiary if coal-derived ammonia scales in India.

29. Deepak Fertilisers

Strong downstream ammonia, nitric acid and ammonium nitrate linkage. One of the best chemical beneficiaries.

30. Alkyl Amines and Balaji Amines(Chemical Winners)

Coal → Syngas → Methanol → Amines. Among the most attractive downstream value-add beneficiaries. Long-term winner if India becomes self-sufficient in methanol.

31. Linde India Limited and INOX Air Products

Gasification consumes huge amounts of oxygen. Many Chinese Big coal gasification plants have dedicated oxygen units.

🏆 My Coal Gasification Watchlist:

Balaji Amines | NTPC | NLC India | Engineers India | L&T | Thermax | Deepak Fertilisers | Alkyl Amines | GMDC | BHEL | RCF | South West Pinnacle Exploration Ltd

Indirect Beneficiaries

-Aegis Logistics Limited

-Linde India Limited

-GAIL (India) Limited

These benefit if volumes rise.

Fertilizers theme become beneficiaries if domestic coal-derived ammonia replaces imports

The biggest wealth creation historically happens in chemicals for future, not mining.

Coal → Syngas → Methanol/Ammonia → Specialty Chemicals is where margins compound.

Not a buy sell recommendation. Not Sebi registered advisor, DYOR before taking any investment decision.

What is HRSG and why are investors suddenly talking about it?

1/ HRSG (Heat Recovery Steam Generator) is one of the biggest hidden beneficiaries of the AI and Data Center boom.

And it may become one of the largest growth drivers for DEE Development.

A thread 🧵👇

see One scanner is enough for life

Top gainers of the day.

Rest all are children, grandchildren and useless cousins of the same scanner.

But scanner is not edge.

Any one can see which stock is up 10%.

Real edge is asking

Why did it move?

Who is buying?

Is FA supporting TA?

Is this earnings re-rating or just operator circus?

Is volume real or trap?

Is sector waking up or one candle drama?

Scanner only shows movement.

Your brain decides whether it is opportunity, noise, or bait.

axiscades came as part of PEAD way back while analyzing Q results

I was here from 2010.

Life was cool when I was not known, or when I had less than 500 followers.

I started posting more after quitting my job three years back, and even more after my knee ACL surgery.

I did every mistake a new investor does.

You name it, I might have done it.

Bought stocks from Moneycontrol discussion boards 20 years ago without understanding the business or risks.

After some initial success, got false confidence, took a ₹2 lakh personal loan, invested it, and burned almost everything.

Averaged down thinking price has to come back.

Bought penny stocks and low market-cap names thinking they will rise fast.

Followed TV recommendations.

Every stupid mistake a beginner investor makes, I have done it.

In Telugu there is a line:

“Bhogi kaanivaadu Yogi kaaledu.”

One who has not gone through indulgence, mistakes, burns and temptations cannot become wise like a yogi.

So when I say something today, it is not theory.

It is burn marks speaking.

--------

Other mistakes I did as a new investor:

Buying just because the stock had fallen 50%, thinking it had become cheap.

Confusing low price with cheap valuation ₹10 stock looked cheaper than ₹1,000 stock.

Looking only at profits, not cash flow, debt, pledging, dilution or promoter quality.

Selling winners too early and holding losers forever.

Thinking every operator-driven move is “smart money accumulation.”

Believing every turnaround story without checking whether the balance sheet can survive.

Buying because some big investor entered, without understanding their time horizon or position size.

Taking allocation too big in stocks I did not understand properly.

Not respecting liquidity — easy to enter, impossible to exit.

Getting emotionally attached to stocks and defending them like family members.

Mistaking bull market luck for personal skill.

Thinking more information means better decision-making.

Watching price every day but not watching business progress.

Ignoring opportunity cost holding dead stocks while better stocks kept moving.

Learning risk only after losing money.

Timepass talk on Sunday

1. Sudeep Pharma

Sudeep Pharma is a manufacturer of excipients and specialty ingredients catering to the pharmaceutical, food, and nutrition industries. With a portfolio of more than 100 products, the company serves over 1,100 customers across 100 countries.

What are excipients?

Think of an excipient as the "delivery vehicle" or the supporting cast in a pharmaceutical formulation. While the Active Pharmaceutical Ingredient (API) is responsible for the therapeutic effect, it often constitutes only a small portion of a tablet or capsule. Excipients are the inactive ingredients, such as binders, fillers, stabilizers, and coatings, that provide the medicine with its structure, improve shelf life, enhance absorption, and ensure consistent delivery of the active drug.

If you have been tracking the Indian pharma ancillary space closely, the word 'excipients' should immediately bring two more names to mind: Sigachi Industries and Accent Microcell.

However, the structural economics of these businesses diverge completely based on their core chemistries. While Sigachi and Accent dominate the organic, cellulose-based excipient market (primarily Microcrystalline Cellulose), Sudeep Pharma operates in the inorganic, mineral-based excipient domain (Calcium and Magnesium salts).

To put their operational moats into perspective:

Cellulose-Based: Hard to engineer, but easier to qualify. Success depends on complex polymer physics and precision spray-drying, but the organic raw materials carry low regulatory risk.

Mineral-Based: Easier to synthesize, but brutal to purify. The chemical reaction is textbook, but stripping out mined heavy metals down to safe parts-per-million (ppm) levels requires an elite purification infrastructure.

We will leave it at that for now; a detailed forensic comparison of their manufacturing economics, margin profiles, and asset turns is a topic for another day!

Coming back to Sudeep Pharma, they currently operates across two established verticals and is building a third growth engine.

i) Pharmaceutical, Food & Nutrition (PFN): 56% of Revenue

Under this segment, Sudeep manufactures high-purity mineral-based ingredients such as calcium, zinc, iron, potassium, magnesium, and sodium compounds. These ingredients are critical inputs for regulated pharmaceutical, nutraceutical, and food applications.

The company is the first and only Indian manufacturer to receive USFDA approval for mineral-based ingredients, providing it with a strong competitive advantage in regulated markets.

ii) Specialty Ingredients: 44% of Revenue

The Specialty Ingredients division focuses on technology-driven, customized ingredient solutions designed to meet specific customer requirements. These products help improve nutritional delivery, enhance taste and texture, increase bioavailability, and ensure product stability across a variety of end-use applications.

This is the company's higher-growth and higher-margin segment, benefiting from increasing customer demand for differentiated and value-added ingredient solutions.

iii) Battery Materials: The Emerging Growth Driver

Sudeep is making significant progress in battery-grade iron phosphate, a key raw material used in Lithium Iron Phosphate (LFP) batteries.

The company expects to complete Phase-I of its battery materials project by the end of FY27, creating 25,000 TPA of capacity through an investment of approximately ₹300 crore. Management has outlined plans to invest a further ₹600 crore over the subsequent three years, taking total capacity to 100,000 TPA.

Customer engagement appears encouraging. The company is already working with 42 global customers, and six of them have successfully completed commercial validation.

Why are Q1FY27 margins expected to be under pressure?

Phosphoric acid, one of the company's key raw materials, has witnessed a sharp increase in prices. While Sudeep has initiated price hikes to pass on these higher costs, certain customer contracts incorporate a lag before revised pricing becomes effective.

As a result, Q1FY27 is likely to reflect only a partial benefit of the price increases, leading to temporary margin compression. Management expects margins to normalize from Q2FY27 onwards as the full impact of the price pass-through is realized.

2. Divgi Torq Transfer Systems

Divgi-TTS is a premier Indian automotive component manufacturer specializing in advanced drivetrain solutions, including engineered transfer cases, torque couplers, and transmission systems. It positions itself as an independent, high-tech player at the forefront of the automotive industry's structural shift toward electric vehicles (EV), dual-clutch transmissions (DCT), and advanced four-wheel-drive (4WD) systems.

After a prolonged slowdown, Divgi is entering a strong structural turnaround driven by a sharp recovery across its core verticals and an aggressive expansion into global markets

The Near-Term Trajectory (FY27): Financial growth is highly visible, anchored by a lucrative, exclusive one-time Indonesian government export order for 70,000 transfer cases. Split equally through its key domestic OEM partners, Mahindra & Mahindra and Tata Motors, this single program is projected to deliver an incremental ₹170–180 crore in revenue for FY27.

The Long-Term Sustainability (FY28 & Beyond): To counter the cyclical cliff of the one-time Indonesian order, management is scaling multiple independent, multi-year growth triggers. These include upcoming vehicle platforms like the Tata Sierra 4WD program, increased export volumes to the US via a Ford-related application, and entry into the high-volume electric 3-wheeler segment. Furthermore, its EV transmission vertical is poised to capture underpenetrated market share as newly approved proprietary designs ramp up for Tata Motors' Nexon and Curvv EV platforms.

3. Anthem Biosciences

Anthem Biosciences is a fully integrated CRDMO with capabilities spanning the entire drug discovery, development, and manufacturing value chain. It is among the few Indian companies offering services across both New Chemical Entity (NCE) and New Biological Entity (NBE) programs. Over the years, the company has built expertise across several advanced technology platforms, including RNA interference (RNAi), Antibody-Drug Conjugates (ADCs), peptides, lipids, and oligonucleotides.

The CRDMO segment contributes over 80% of Anthem’s revenues and enjoys industry-leading profitability. EBITDA margins stood at 43.4% for FY26 and expanded to 48.1% in Q4 FY26. No other listed Indian CRDMO operates at a comparable margin profile. Management attributes these margins to structural advantages arising from backward integration, process efficiencies, and disciplined cost control rather than any one-off benefit.

Rimegepant, the active ingredient in Pfizer’s blockbuster migraine therapy Nurtec ODT, is estimated to contribute nearly 20–25% of Anthem’s CRDMO revenues. With Nurtec generating more than $1.4 billion in sales during 2025, Rimegepant remains one of Anthem’s most commercially significant molecules.

Anthem is currently undertaking the largest capacity expansion program in its history. The company also added two new global Big Pharma customers during FY26, further strengthening its client base.

Over the last two to three quarters, Anthem commercialized four new molecules, taking its portfolio of globally commercialized products to 14. For each of these molecules, Anthem serves as the sole-source manufacturer of either the final Active Pharmaceutical Ingredient (API) or a critical regulatory intermediate.

External analysts estimate that the peak global commercial opportunity associated with the four newly commercialized molecules is approximately $10 billion. In addition, Anthem currently has 10 molecules in Phase III clinical trials, providing a strong foundation for future commercial launches and long-term growth.

That said, valuations are screamingly expensive at this point.

4. The WuXi AppTec Euphoria

The news that the Pentagon has added WuXi AppTec to its list of companies allegedly linked to the Chinese military dominated discussions across financial Twitter this week. However, much of the broader narrative appears either misplaced or misunderstood.

i) What happened?

The Pentagon updated its annual 1260H list, adding roughly two dozen entities, including high-profile Chinese companies such as Alibaba, Baidu, BYD, and WuXi AppTec, one of the world's largest CRDMO players.

The 1260H designation identifies companies that the U.S. government believes are either assisting China's People's Liberation Army (PLA) or are linked to Beijing's military-civil fusion strategy.

WuXi AppTec responded immediately, calling the designation "clearly a mistake" and reiterating that it is neither controlled by nor affiliated with any military or government entity, nor does it provide services to China's armed forces.

ii) How significant is WuXi's U.S. exposure?

Very significant.

Approximately 75% of WuXi AppTec's revenues are derived from U.S. customers. Sell-side analysts, including Bloomberg Intelligence, estimate that as much as $30.4 billion (206 billion yuan) of U.S.-linked revenue could be at risk between 2027 and 2030 if customers aggressively diversify away from the company.

iii) Does this mean U.S. pharma companies will stop working with WuXi immediately?

The simple answer is no.

The 1260H designation itself does not impose immediate sanctions, asset freezes, or commercial restrictions. However, it gains significance through its interaction with the Biosecure Act, which was signed into law in December.

The legislation restricts U.S. government agencies from contracting with organizations that rely on services provided by companies appearing on the Pentagon's Chinese military companies list.

Importantly, the framework includes a five-year grandfathering period, allowing existing pharmaceutical clients sufficient time to wind down contracts, transfer manufacturing processes, and establish alternative supply chains without jeopardizing eligibility for federal healthcare programs such as Medicare and Medicaid.

There is another important nuance. The restriction primarily applies to federally funded programs. If a pharmaceutical company operates both federally funded and privately funded projects, only the government-funded programs face direct compliance challenges. While maintaining separate supply chains introduces significant regulatory complexity and compliance costs, private commercial programs can technically continue working with WuXi.

iv) WuXi's reshoring strategy

WuXi is not standing still.

WuXi AppTec continues to expand its Delaware manufacturing footprint, with the objective of locating roughly 20-30% of its global capacity within the United States. Similarly, WuXi Biologics is relocating an estimated 30-40% of its capacity to U.S. facilities in an effort to mitigate future cross-border restrictions and reassure customers.

v) So, are Indian CDMOs immediate beneficiaries?

Not necessarily in the short term.

This development is unlikely to create an overnight revenue windfall for Indian CRDMOs. However, it does accelerate a trend that was already underway: supply-chain diversification away from China.

As large pharmaceutical companies reassess long-term manufacturing dependencies, Indian CRDMOs are likely to become key beneficiaries of incremental outsourcing mandates. The opportunity is less about immediate contract transfers and more about becoming part of the next-generation global supply chain architecture.

For example, Eli Lilly maintains substantial exposure to Chinese manufacturing partners but already works with companies such as Divi's Laboratories and Sai Life Sciences. The ongoing WuXi situation could encourage Lilly to gradually increase sourcing from Indian partners as part of a broader risk-mitigation strategy. Similar dynamics could play out across several large U.S. pharmaceutical companies, including Pfizer and others.

The key takeaway is that the WuXi episode is not an overnight revenue event for Indian CDMOs. It is, however, another catalyst pushing global pharma companies toward geographic diversification, and India remains one of the most credible alternatives available at scale.

5. Aegis Logistics

Aegis Logistics is one of India's leading logistics and supply-chain companies, specializing in the storage, handling, and distribution of clean energy products such as liquefied petroleum gas (LPG), ammonia, and liquid chemicals. The company operates a strategically located network of cryogenic and liquid storage terminals across major ports on both the western and eastern coasts of India.

Why the excitement?

Recent geopolitical developments and volatility in global energy markets have highlighted Aegis' unique business model. Through its VLGC-compliant infrastructure, extensive import capabilities, and strong global partnerships, the company can source LPG from the most economical global markets rather than being dependent on a single region. This flexibility enables Aegis to expand distribution margins during periods of supply disruption and price dislocation, turning market volatility into a competitive advantage.

That said, the bigger story is not the short-term opportunity, it is the long-term infrastructure platform that Aegis is building.

i) Significant Commissioning of Growth CapEx

Aegis is entering a phase where several large projects are expected to begin contributing simultaneously.

Liquid Storage Expansion

The first phase of a ₹1,675 crore expansion project at JNPT, comprising approximately 318,100 cubic meters of additional liquid storage capacity, is scheduled for commissioning in H1 FY27. In parallel, the Mumbai terminal will add another 64,000 kiloliters of liquid storage capacity during the same period.

Integrated Pipavav Ecosystem

Pipavav is evolving into a fully integrated LPG logistics hub. The new VLGC-compliant jetty is expected to be commissioned during CY2026, while the associated pipeline connectivity is scheduled to become operational in Q2 FY27.

Full-Year Asset Contribution

Cryogenic infrastructure commissioned at Pipavav and Mangalore during FY26 operated only for part of the year. FY27 will be the first year in which these assets contribute for the full twelve months.

ii) Multi-Modal Connectivity to Unlock Higher Throughput

For any terminal operator, storage capacity is only one side of the equation. The speed at which products can be evacuated determines overall throughput and asset utilization.

Several key connectivity projects are expected to come online during FY27:

The Jamnagar-Loni pipeline connection at Kandla has already been completed.

The Kandla-Gorakhpur LPG Pipeline (KGPL) is expected to connect Kandla in H1 FY27 and Pipavav in Q2 FY27.

New LPG rail gantries are under construction at both Mangalore and Pipavav, creating efficient and cost-effective evacuation routes into Central, Southern, and Western India.

These projects should significantly improve terminal utilization and throughput volumes across the network.

iii) Scaling the High-Margin Gas Distribution Business

Historically, Aegis' gas distribution operations were concentrated primarily around Mumbai and Kandla. Over the past few years, the company has transformed into a multi-regional platform with operations spanning Mangalore, Haldia, Pipavav, and other strategic locations.

Supported by this expanded infrastructure footprint, management is targeting a substantial increase in distribution volumes, with an ambition to reach approximately 2 million tonnes by FY28.

As distribution volumes scale over a largely fixed infrastructure base, operating leverage could become an increasingly important earnings driver.

iv) Early-Mover Advantage in India's Emerging Ammonia Economy

Aegis is also positioning itself to participate in India's evolving ammonia and clean-energy value chain.

The company is developing India's first independent ammonia terminal at Pipavav, with a static storage capacity of 36,000 metric tonnes. The project is expected to be commissioned in H1 FY27.

Importantly, approximately one-third of the terminal's capacity is already backed by a 15-year take-or-pay agreement with Hindustan Zinc, providing strong revenue visibility from day one. The remaining capacity will be available for third-party customers, creating opportunities for higher-margin throughput and distribution revenue.

The long-term opportunity could be substantial. CRISIL estimates that India could face an ammonia supply-demand gap of nearly 3 million tonnes by 2029. Through its strategic partnership with ITOCHU Corporation, which has acquired a stake in the Pipavav ammonia terminal, Aegis is positioning itself at the center of this emerging opportunity.

v) The Bigger Picture

Aegis Logistics is gradually transforming from a traditional storage terminal operator into a diversified clean-energy logistics platform. Between large-scale capacity additions, improving pipeline and rail connectivity, a rapidly expanding gas distribution business, and a first-mover position in ammonia infrastructure, the company appears to be entering a period where multiple growth drivers could begin contributing simultaneously over the next two to three years.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes.

Everyone talks about cash flow.

Every Twitter expert instantly says, iska cash flow negative hai, yeh bekaar company hai.

Bhai, pehle cash flow ko samajh to lo.

Let me explain how cash flow actually works. Not every company with negative cash flow is bad some can eventually become multibaggers. 👇

Cashflow is heavily driven by your working capital cycle, which depends on three main pillars:

1⃣ EBITDA margin

2⃣ growth rate

3⃣how much cash gets locked up in the business as you scale.

Now here is where most people miss the plot completely.

For any given margin and working capital structure, there is a specific growth rate above which even a highly profitable company becomes operating cashflow negative.

This happens because when revenue grows, your working capital needs grow proportionally.

Every 100 rupees of new revenue locks up cash in your inventory and receivables before you ever see a single paisa of profit.

The threshold where growth starts consuming more cash than the business generates is driven by a simple relationship:

Maximum Cash Sustainable Growth = EBITDA Margin x (365 / Net Working Capital Days)

Where Net Working Capital Days = Inventory Days + Receivable Days - Payable Days.

Let us do the actual math to see how this traps people. Say a company does 100 crore rupees in revenue with a 10% EBITDA margin, meaning it makes 10 crore rupees in profit. Its net working capital days are 90 days, which means roughly 25% of its revenue is always locked up in operations.

If this company decides to grow aggressively by 50% next year, revenue jumps to 150 crore rupees. On the P&L, everything looks amazing. EBITDA jumps to 15 crore rupees.

But look at the cash flow statement. To support that 50 crore rupees of new revenue, the company must lock up an additional 25% of that growth amount into inventory and customer credit. That is a massive 12.5 crore rupees sucked out of the bank account instantly just to fund operations.

Once you subtract that 12.5 crore rupee working capital drain from your 15 crore rupees of EBITDA, and then pay for basic things like taxes and interest, your actual net cash flow flips negative. Even though EBITDA is positive throughout. The P&L looks fine. The cashflow statement is screaming.

This is why Infosys and TCS are such incredible cash machines by the way. Infosys runs 20% plus operating margins and collects cash from clients incredibly fast, leaving them with low working capital days. Their structural math protects them, meaning even at high revenue growth they consistently generate operating cashflow that equals or exceeds their reported profits.

Now take Zaggle Prepaid. Strong growth story. 40 to 50% revenue growth, EBITDA margins in the 9 to 10% band. When you grow that fast on tight margins, you are operating right at the knife edge. One quarter where growth accelerates and collections slow even slightly and operating cashflow flips negative. This is not a bear thesis on Zaggle, their prepaid float gives them a genuine structural offset. But it does mean EBITDA alone tells you nothing here. You have to track their cash conversion cycle every single quarter without exception.

Now the part everyone gets wrong. Is cashflow negative always bad?

No. And this is the nuance that separates good investors from average ones.

There are two completely different types of cashflow negative companies. The first is chosen negative cashflow. Management made a deliberate decision to grow faster or invest heavily because the returns justify it. The second is forced negative cashflow. The business structurally cannot generate cash at its current parameters. No choice involved.

Same number on the cashflow statement. Completely opposite implications.

Think about what Jio looked like in 2017 and 2018. Reliance was burning tens of thousands of crores on spectrum, towers, and fiber. Operating cashflow was fine because telecom is a upfront prepaid model, but their free cashflow was deeply negative due to massive investments. That was 100% chosen burn. Every rupee of capex was creating a hard physical asset with a 20 year earning life. When it turned, it was one of the greatest value creation stories in Indian corporate history.

Byju's is the exact opposite. For years the revenue line looked impressive. But collections were not matching reported revenues. Operating losses were structural, not cyclical. Unit economics were deteriorating with scale, not improving. Marketing spend to acquire customers who churned. Cashbacks to generate GMV that evaporated the moment you stopped spending. Every rupee of burn was creating liabilities, not assets. Management never gave a credible timeline for cashflow positive because there probably wasn't one. The cashflow statement was telling the truth the entire time. Nobody listened.

So before you form a view on any cashflow negative company, ask five questions.

Is the burn chosen or forced? Are unit economics improving or deteriorating as scale increases? Is the balance sheet moving from net cash to net debt and how fast? Is the capex creating real durable assets or is it pure opex with nothing on the other side? And does management have a specific credible timeline for when the business turns cashflow positive?

If you get good answers to all five, cashflow negative is fine. Even exciting sometimes. The re-rating when cashflow turns in a well-run high growth company is where some of the best returns in smallcap investing get made.

If you get vague or evasive answers? Pass. Regardless of how good the growth story sounds on the surface.

EBITDA is an opinion. Cashflow is a fact. But even cashflow needs context to be understood correctly.

Next time a management team brags about EBITDA growth, ask them what their working capital cycle is doing. And ask them when they plan to be free cashflow positive.

The answer, or the absence of one, will tell you everything you need to know.

Parag Parikh Flexi Cap Fund -

Rank in category:

- No 1 in 10Y time frame

- No 6 in 5Y time frame

- No 13 in 3Y time frame

- No 25 in 1Y time frame

- No 36 in 6M time frame

Among 44 Flexi Cap funds today.

Long term winner, but recent performance has been average.

(Source: Advisorkhoj)

The past 8–9 weeks have been exceptionally rewarding for small and mid cap investors. However, if market volatility returns and the correction gathers pace, these are ten themes worth keeping on the radar.

That said, many of the stocks within these themes have already rallied significantly and may not be available at reasonable valuations. The price at which one is comfortable investing is a personal decision and should be backed by independent research and due diligence.

1. CDMO/Specialty Pharma - Sai Life, Laurus Labs, Shilpa Medicare, Gland Pharma (In the middle of a multi-year earnings cycle)

2. Recycling - Gravita (Consistent compounding theme, incremental capacities to help, plus copper foray)

3. Electrification - Quality Power, Atlanta Electricals, Yash Highvoltage, Hindusthan Insulators & Industries

4. Growth Theme - Timex, DEE Development, Prizor Viztech, SBCL

5. Precision Engineering (expensive bucket) - Sansera Engineering, Omnitech Engineering, Sedemac and OBSC Perfection

6. Image makeover - Fineotex Chemical (The CrudeChem slingshot), PVP Ventures (Real Estate to Healthcare), Viyash Scientific ("the next big thing") and NPST (international aspiration)

7. Tier 2/3 Pharma - Sakar/Sudeep/Kwality Pharma/Venus Remedies

8. Exports Bucket - Garware Hi Tech and Goldiam

9. Logistics - Aegis Logistics

10. Defence - Apollo Micro and Paras Defence

Disclaimer: Not a buy or sell recommendations. Shared for further research and study.