$ASTS was up 5% pre market on the $AMZN $GSAT news and has since given it all back and then some being down over 10% since the pre market top

That is the market being irrational in real time and I want to explain why this news is actually one of the most bullish things that has happened for the entire D2D sector this year.

$AMZN is acquiring $GSAT Globalstar for roughly $9 billion. Let that sink in.

Globalstar does $272 million in revenue. Has a basic LEO network. Powers Apple Emergency SOS. Limited direct to device capability. The technology is miles behind $ASTS.

$AMZN is paying $9 billion for the inferior version of what $ASTS has already built.

This is not bearish for $ASTS. This is the most powerful sector validation imaginable.

The largest e-commerce and cloud company on earth just told you that direct to device satellite connectivity is worth acquiring at any price.

They looked at the competitive landscape and decided they needed a satellite network immediately regardless of cost.

They picked the worst horse in the race and still paid $9 billion for it.

$ASTS has 50+ carrier partners covering 3.2 billion existing subscribers. 120 Mbps speeds directly to unmodified smartphones. BlueBird 7 on the launchpad right now. $3.9 billion in cash. Fully funded constellation buildout.

$GSAT has Apple Emergency SOS and a fraction of the technology.

The market is selling $ASTS on news that just proved the entire thesis.

Every major tech company on earth is now in a race to own D2D connectivity and $ASTS is the only pure play publicly traded company that has actually built it at scale.

The pullback is a gift.

Hi @elonmusk Dr. Barbacid, the Spanish doctor who found the cure of pancreatic cancer in rats, is begging for funding to keep researching so it can actually save humans. He needs 30M €.

Of course the Spanish Government chooses to fund "other priorities"

$ASTS Having read the full thing now I think it's fair to say that this is not an analyst note, but that this reads like a complete short report.

Clearly Andres Coello has been talking to the shorts, who are desperate after multiple face ripping rallies.

This short report just feels disingenuous and everything is framed in a way to justify the negative rating, instead of keeping an open mind. This analyst is literally grasping straws probably in a coordinated manner.

Let's start with the basics: 90% of the arguments in this short report are framed as SpaceX vs AST Spacemobile, but in reality the market is big enough for both. Just with that realization 90% of the analyst short thesis falls apart.

But let's dive into the details regardless, because not only is the notion above wrong, the details are full with hallucinations:

What he got right:

> The company has been delayed multiple times, but instead of also calling delays out on Starship and Starlink D2C next version birds this is supposedly only negative for AST... Because if SpaceX delays its ok, but if AST delays its really bad right? 🤣

This was basically the only thing he got right...

What he got wrong: (long list)

> Starlink fixed broadband has nothing to do with the D2C efforts, except for maybe in India where Airtel / Reliance Jio might bundle both. Using stats from this buildout is completely irrelevant for D2C.

> User adoption is slow/ ARPU modest, because SpaceX decided to push a faulty architecture that is available on limited phones, only works outside, text, voice and limited data and you need to point your phone to the sky at all times. Don't extrapolate demand based on a beta service.

> Starlink is two year ahead of AST Spacemobile. Here Andres is framing Starlink's beta service versus AST's current birds in the sky, but he completely misses the point. The real race is not for spotty beta coverage, but to provide broadband internet from space to a very large set of phones with minimal disruptions that do not require pointing your device in the sky and can even work indoors (one wall)

In that race as of today Starlink has zero satellites that are capable of doing that. Realistically AST needs ASIC birds for that as well so also zero, so this race is still completely open, so the 2 year frame is completely wrong.

> Regarding CAPEX he now frames the low band and mid band constellation as duplicative efforts, which is crazy because the low band constellation is the major differentiator compared to Starlink (this will make you not have to point your phone at the sky and let this work somewhat in doors (one wall)

Next we go into the speculative section to add extra FUD to the short report:

> Speculates American Movil (Telcel) could partner with Starlink, but he conveniently forgets to mention that Elon Musk called Carlos Slim a drugdealer working for the cartels and that Slim cancelled all relationships with Starlink in the process. He also forgets to mention that Slim and Abel Avellan know eachother relatively well and that AST is already beta testing in Mexico.

> Virgin O2 (Liberty & Telefonica) has an agreement with Starlink, because AST is exclusive with Vodafone in the UK. Telefonica will be an AST partner, 100%. That Andres did not know this is crazy. Do your homework!

> Next goes onto the laser mesh network of over 9000 satellites as standalone network in space. That supposedly so superior AST should basically give up. Except Andres has zero clue how most of these MNO's operate. With a bent pipe architecture you get sovereign communications, which is extremely important for EU, Middle East and anyone who cares about its communications. SpaceX is operating a massive NSA spy satellite network in orbit, not a lot of MNO's will have the appetite to run on that if they want to keep their government business. That's why Telefonica, Orange and Telenor will all sign up with AST. Watch!

To conclude: Let's call a duck a duck. This is a short report written by someone who is on purpose misframing information to justify is negative price target.

Let's all save this one, because in one year we are absolutely go to laugh our pants, when it will become so obvious this is an extremely dumb take.

Todo apunta a que el sector más explosivo del 2026 será sin duda el sector espacial!!

El motivo ?

Durante 2026, nuestro genio loco favorito, Elon Musk, sacará SpaceX a bolsa

convirtiéndola en una de las IPOs más esperadas

y MÁS cara de la historia

Y que compañías se verán indirectamente MAS beneficiadas ??

Te cuento 👇🏻🧵💣

Correct.

My Tesla and SpaceX shares, which are almost all my “wealth”, only go up in value as a function of how much useful product those companies produce and service.

This means my “wealth” can only increase due to producing more products and services for the public. Moreover, anyone else who is a shareholder in Tesla and SpaceX, which incudes employees, participates in the upside of stock appreciation.

That is because I am a maker, not a taker like the Bernie Sanders type politicians of the world. They take and they’re on the take, because they cannot or will not make.

🔥 $PLTR

"To all supporters of Palantir, Merry Christmas and Happy New Year and to all people who hated on us, ENJOY YOUR COAL"

-Palantir CEO Alexander Karp

Qué vender cuando ya estás contento y tranquilo con la cartera actual, cuando los rangos de TIR esperadas son amplios y similares. Está bien que las ideas compitan por formar parte de la cartera, pero son decisiones difíciles.

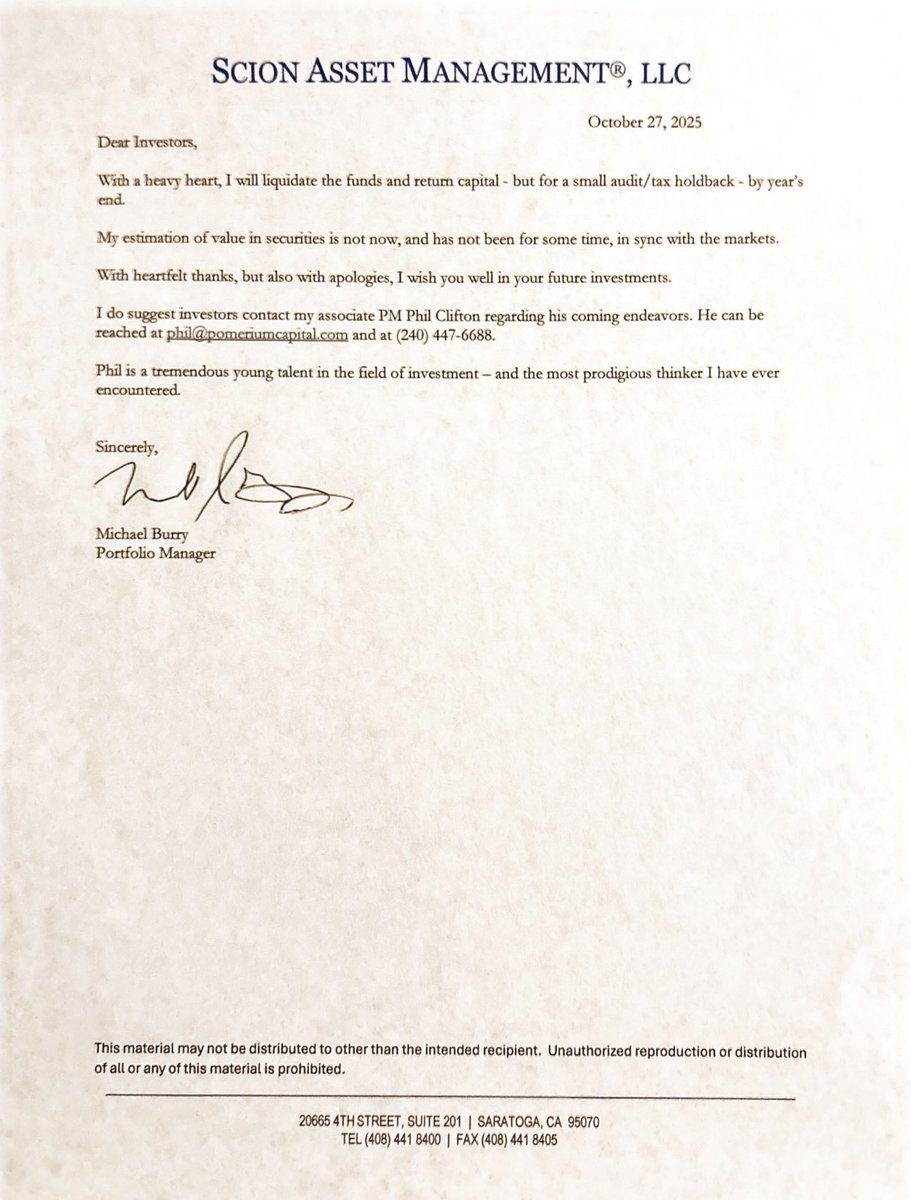

🚨 MICHAEL BURRY CERRARÁ SU HEDGE FUND A FINALES DEL 2025:

Traducción: "Estimados inversores:

Con gran pesar, liquidaré los fondos y devolveré el capital —salvo por una pequeña retención de auditoría/impuestos— para finales de año.

Mi visión no está alineada con la valoración de los activos desde hace tiempo.

Con sincero agradecimiento, pero también con disculpas, les deseo lo mejor en sus futuras inversiones".

----

Coincide con su aviso de la burbuja de la IA y sus últimas publicaciones aquí en X.

¿Quiere decir esto que se retira como inversor? No lo parece. Burry lleva comentando en los últimos días que el 25 de noviembre contará las mayores novedades y puede que tenga que ver con los siguientes pasos a seguir. Veremos.

- Es fácil, ves este círculo? OpenAI instala 6 GW de GPUs de AMD, AMD factura, y AMD le da a OpenAI hasta el 10% de sus acciones, que suben to the moon. Además, OpenAI instala 10 GW de Nvidia, y Nvidia invierte $100 bn en OpenAI para que se haga. Nvidia factura.

- Espera Espera, a ver si lo he entendido, entonces Nvidia es proveedor e inversor a la vez?, pero ¿Nvidia tiene $100 bn de caja para invertir en OpenAI?

- No, pero tú tranqui, OpenAI le dará $300 bn a Oracle por cómputo en la nube, Oracle factura y to the moon, y Oracle lo usará para comprar chips de Nvidia. Nvidia factura, su valoración se dispara y ya puede invertir en OpenAI. Lo llamamos ChatCDO, ¡Infinite money glitch !

- Y cuánta caja tiene que generar OpenAI para que se sostenga el círculo, digamos, hasta 2030?

- Nada, unos pocos trillones

- QUÉ?!?!

He hecho periódicamente simulaciones de Montecarlo con la cartera actual y mis estimaciones de TIR por escenarios de cada empresa, e introduciendo volatilidad aleatoria típica del mercado, para ver cómo interaccionan con los límites de diversificación distintas estrategias, comparando con el ideal sin límites. A 10 años. Me suelo fijar en la rentabilidad total y en el ratio de Sortino. Pero al final hay que tener en cuenta que sólo son mis estimaciones y que el verdadero riesgo es el de pérdida permanente. Lo que queda claro al final es que lo mejor es dejar margen a las empresas para que puedan avanzar en la cartera sin estar cerca de los límites.