The @metmuseum made history today, launching its first blockchain initiative ever on @base. 🎨💙

Check out Art Links, a blockchain based art connection game ft over 140 works of art from the MET’s collection.

Payment support @MoonPay. Developed in partnership with TRLab. 🧵⬇️

Are banks facing a generational shift?

Fintech startups have sparked innovation, but banks have remained pivotal in embedded finance with their compliance expertise. Their users want both.

🙌🏻 Coexistence

Fintechs have reshaped how we interact with money, introducing features like digital wallets, peer-to-peer payments, and earned wage access. Take Uber as an example: drivers now manage earnings, track expenses, and even get cashback on gas — all in one place. These innovations have filled gaps left by traditional banks, offering transparency, control, and expanded access to underserved demographics.

But none of these offerings would exist without banks. Sponsor banks, which can accept FDIC-insured deposits, provide the regulatory and operational backbone for fintechs — and even power their own digital banking brands.

👩🏼🤝👨🏽 Consumerization

Consumers, as well as businesses, want speed, personalization, and convenience. And they’re not shy about seeking it elsewhere. 46% of Gen Z are already using third-party money management apps in addition to their core bank (Tink/Visa), and 57% want better financial visibility from their primary bank. A staggering 75% of consumers are ready to switch banks for quicker processing, lower fees, and personalized tools (up from 52% 3 years ago, according to PYMNTS).

To stay relevant, banks need to adapt. They must embrace modular, API-driven systems that can enable instant payments (57% of US banks are integrating FedNow), embed financial services directly into non-financial platforms, and seamlessly integrate fraud protection and compliance with core systems.

✅ Compliance

Banks, with their compliance expertise, are becoming indispensable partners in scaling fintech innovations. Their robust risk management infrastructure allows fintechs to operate securely within regulations. This isn’t just for the big players: community and regional banks are increasingly embracing this approach to generate new revenues (fee income) and diversify their customer base.

Why? Embedded finance partnerships drive, on average, 51% of sponsor banks’ revenue and deposits (according to Alloy). But to scale compliantly, banks are taking control back. They are moving away from third-party "black box" middleware and opting to bring key transactional and compliance capabilities in-house. This approach ensures they scale responsibly while maintaining trust with regulators and Fintech partners.

In short: banks are forced to evolve with their next generation of customers. These demand contextual, tech-driven access to financial services. Banks’ compliance expertise remains unmatched, but the next challenge lies in leveraging technology to meet modern expectations.

Is profitable scaling the new frontier?

Startups are re-discovering the value of profitable scaling as a more sustainable path to success.

🔥 Ignition: the philosophy of "growth at all costs" isn’t new. During the dot-com boom, many experts claimed the “new economy” would defy traditional financial principles, believing massive upfront spending would lead to lasting success. While this approach worked for some, like Amazon, it left a trail of failed dot-com ventures in its wake.

Fast-forward, history is repeating itself — especially in Fintech. A recent report by Silicon Valley Bank on the “Future of Fintech” paints a sobering picture of today’s market. The once-straight path across funding stages now requires resilience and discipline. For Fintechs aiming to move from Seed rounds to Series A, the graduation rate has dropped from ~15% in 2019-2021 to ~ 5% in 2022-2023. It’s a reality check, especially for companies heavily reliant on high user volume and take-rate models. They are vulnerable to rising capital costs, increased delinquencies, and lower-than-expected LTV.

🚀 Ascent: Fintechs are facing more than high interest rates. Their rising CAC are putting added pressure on margins. Many are adapting their offerings and operations by refocusing on B2B, partnering with established brands, obtaining bank charters, and diversifying revenue streams to reduce their dependence on a single product.

Robinhood’s or Coinbase’s evolution from trading platforms to multi-product ecosystems shows how diversifying revenue can better insulate against market pressures. But these strategies are only effective if companies have two essential assets: a scalable platform that can support multiple offerings, and sufficient runway to sustain growth through turbulent times.

🪐 Velocity: success depends on mastering efficiency. According to SVB, 80% of US fintechs reported improving EBITDA margins YoY -- a significant improvement from their low point in Q2 2022. Burn rates, an indicator of efficient growth, are also moving in the right direction, but remain elevated: the median burn rate stands at 3.7x for the top quartile.

In the lower tiers, many are still consuming capital at unsustainable rates. For them, efficiency is an urgent imperative: improve unit economics and secure enough cash runway to support profitable scaling. As ~30% of US fintechs now have only 6-12 months of runway left (up from 20% last year), time is of the essence.

In short: for startup founders and executives, the challenge is to recalibrate their business models for profitability and partner with investors who bring not just capital but operational acumen. A clear path to profitability is the best way to stay in orbit, or at a minimum ensure a soft landing.

Is SaaS becoming "Service as a Software"?

The SaaS landscape is poised to shift from purely product-driven to outcome-focused services.

🌥️ SaaS evolution

Software delivery has evolved through different waves. First, on-premises software was purchased outright, with low alignment between customer and vendor interests. In the early 2000s, a second wave of cloud-native SaaS brought in subscription-based models, shifting maintenance to vendors and easing deployments. Yet, many SaaS contracts still lock customers into paying for unused features.

The third wave will see SaaS enhanced by AI agents. As "copilot" and "autopilot" capabilities help complete tasks previously handled by people, SMEs will have more bandwidth to focus on the actual quality of services delivered to their internal users and customers, using SaaS platforms as a vehicle for business outcomes rather than process execution. In parallel, business users may have greater flexibility to switch providers as AI enables lower data migration and integration costs. McKinsey estimates that churn may increase by 1 to 3 percentage points as buyers explore new vendors, or even self-built solutions.

☝🏻 Human edge

AI agents are transforming industries: they accelerate lead validation in sales, or data crunching for risk assessment in finance. Yet, when complex decisions are required, human insight fills the gaps. For instance, fraud detection relies on AI to flag suspicious activities, but human analysts are needed to refine algorithms and adapt to new fraud tactics.

This human-machine synergy enhances outcomes. As AI tools take on repetitive tasks, human intelligence adds strategic value, helping companies move beyond “getting it done” to excelling at each step of service delivery. A 2020 survey from Deloitte showed that 60% of companies planned to use AI to assist workers, rather than to replace them (12%).

💰 New monetization

With AI adoption, outcome-based pricing models will become more prevalent, focusing on measurable results that align with customer goals. Salesforce's decision to charge $2 per conversation, instead of by user or seat, for Agentforce signals an interesting pivot (despite being more usage- than outcome-based).

This will require changes in delivery and billing models. Metrics will be needed to transparently link outcomes to specific SaaS functionalities, a challenge when external factors contribute to results. Vendors may also need to absorb financial risks if outcomes aren’t achieved.

In short: this evolution will impact how early- and mid-stage companies approach building their solutions. While it may push back their break-even points, it positions them for long-term growth by delivering value-as-a-service at the right margins and scale. They will need the backing of growth-focused investors who bring an operator mindset and understand that the path to success will be less linear and require profitable scaling with a high level of adaptability.

Can AI agents outsmart SaaS?

For nearly two decades, SaaS has been the go-to for businesses seeking efficiency and reduced IT overhead, driving the global SaaS spend from $31B in 2015 to ~$250B this year. But AI agents are reshuffling the deck.

🤜🏻 Klarna’s AI push

One striking example is Klarna’s decision to abandon major SaaS vendors, including Salesforce and Workday, to build its own AI-powered systems. Using OpenAI’s enterprise ChatGPT, Klarna automates tasks that used to require entire teams or SaaS solutions. Its AI-driven customer service assistant replaced 700 employees and handled 2.3 million interactions in its first month. AI offers a lifeline to profitability to a company trying to claw back from a $1B loss in 2022 (down to $32M in H1 2024).

SaaS pioneers are taking notice too. At Dreamforce 2024, Salesforce introduced Agentforce, a move from "human-in-the-loop" to “human-at-the-helm”, with autonomous agents capable of managing customer interactions independently. These bots seamlessly integrate data across Salesforce’s unified platform.

⛽️ The new efficiency paradigm: people-light, systems-light, data-smart

A trend is emerging: businesses will be people-light, systems-light, and data-smart. Organizations are not just looking to automate tasks; they’re aiming to consolidate data, eliminate costs and redundancy, and increase agility. According to Bettercloud’s State of SaaS Ops 2024 report, organizations now use an average of 112 different SaaS tools, down from 130 last year - a first-time decline.

Startups will have more options to embrace modular, low-code platforms to compose AI-driven workflows handling specific tasks. In fintech, AI-powered platforms that dynamically adjust credit risk in real-time can slash the need for third-party solutions.

📊 Three Implications for Startups Operations

While this shift won’t happen overnight, startups should rethink their approach to product architecture, operations, and human capital. This transition also calls for capital solutions that support lean, right-sized growth.

- Data-centric solutions: startups must architect their solutions around data. Capturing, securing, and processing data intelligently is a competitive edge.

- Operational efficiency: startups must increase operational efficiency while keeping costs down. AI/LLM agents and modular platforms can provide agility without the cost of complex systems.

- Human expertise still matters: AI won’t replace human insight and creativity. In fact, with the right AI tools, employees can deliver not just products but better business outcomes—turning the human touch into a new differentiator.

In short: businesses and startups should reimagine their product and operational strategy around data, efficiency, and the right capital solutions to sustain growth. The companies that thrive will be the ones that move beyond automating tasks to re-engineering entire workflows, making them smarter, leaner, and more human-centered.

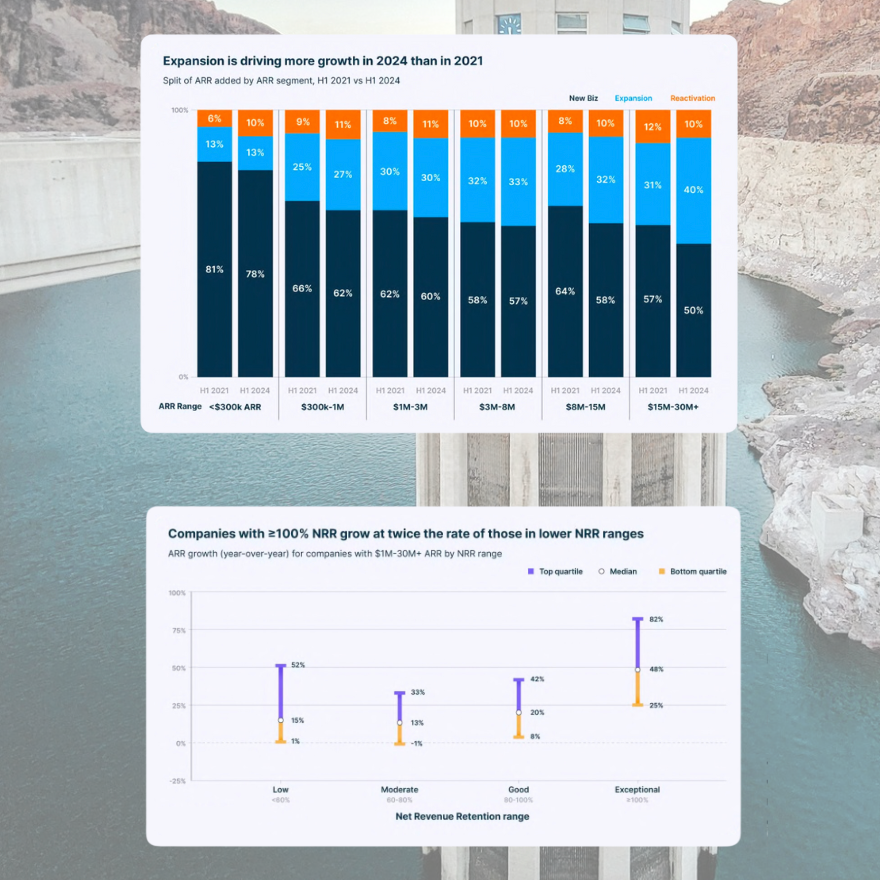

If they come, will they stay?

In the financial domain and beyond, SaaS companies have spent the past few years obsessing about how to get more customers. As it turns out, retention is the real game.

🧲 Retention: the new growth engine

High growth doesn’t matter if your customers don’t stick around. A recent ChartMogul report shows that companies with ARR between $15M and $30M are now getting 40% of their growth from existing customers, a sharp jump from 30% just 3 years ago. If they want to survive the long haul, founders and managers need to focus on the customers they’ve already signed up and have them renew — and expand — year after year. The fact that Net Revenue Retention (NRR) is slipping to 78% on average for companies with large subscriber bases is a sobering reminder that acquisition is meaningless without retention.

⛽️ Efficiency: the new paradigm

Gone are the days of burning through money in a race to the top. Today, frugality is a competitive edge. Metrics like Customer Lifetime Value (LTV) and unit economics make the difference between thriving and barely surviving. The best SaaS companies aren’t chasing vanity metrics anymore. This is where the right capital solutions make all the difference. Founders don’t need investors who just write checks; they need ones who can give the runway and expert advice to build disciplined, retention-focused growth.

🔏 Indispensability: the new competitive moat

The key to SaaS success is not about building a product people like — it’s about building something they can’t live without and are willing to pay for because it solves their pain points and adds measurable value to their work. Companies with ARR over $1M, focusing equally on retention and acquisition, saw the strongest growth rates in 2024, despite a slowdown in new customer acquisition. Companies that hit 100% NRR in the first half of 2024 grew at 48% year-over-year, double the growth of those with lower NRR.

In short: founders and companies who succeed will be the ones who go back to basics: building indispensable products, running lean operations, and partnering with investors who bring more than just capital to the table. The efficiency paradigm, paired with capital solutions that offer real operational expertise, is the new playbook for increasing company value. It’s a simple but powerful formula: retention-first companies are built to last.

Don’t throw the baby out with the BaaS water

Imagine if any business could offer banking services without the headache of building their own payment, lending and settlement infrastructure – this is the power of BaaS (Banking as a Service). By granting third parties access to bank systems, BaaS allows companies to integrate banking functions directly into their products effortlessly. This transformation, often termed “Embedded Finance,” is reshaping how financial services are consumed and delivered.

💸 Embedded Finance at Scale

By 2026, embedded finance revenues in the U.S. are projected to more than double, reaching $51 billion, and worldwide revenues are expected to quadruple to over $160 billion (source: Bain & Company). More impressively, over $7 trillion in transactions will be processed through embedded financial services. This growth underscores the vested interest both banks and users have in making these services ubiquitous and continuously modernized.

⛔️ The Middleware Misstep

Not all implementations of BaaS have been successful. The middleware approach to BaaS has faced significant challenges. It's not BaaS itself but the middleware architecture that has faltered, as illustrated by the recent struggles of Synapse. The BaaS model may be stronger without the middleware layer that Synapse represented (👉🏼 https://t.co/oQa9Sj1TQM). The industry's evolution from these challenges has made it more resilient and robust.

🏦 Banks are Back

The pendulum is swinging back to incumbent banks, which are regaining their lead role in the ecosystem. While Fintech players initially propelled embedded financial services, incumbent banks, with their robust compliance and risk management practices, are indispensable. These banks are now augmenting their existing transactional and risk infrastructures (AML, KYC) to enable new Fintech offerings swiftly and in line with regulatory standards. This shift provides immediate alternatives to struggling middleware players and lays the groundwork for a new enablement layer atop core banking systems.

☁️ The Platform Approach

Financial institutions would benefit from pivoting from the BaaS middleware provider model towards developing their own platforms. Why? This internal approach mitigates the risks and compliance gaps inherent in middleware. By collaborating with vetted software vendors, banks can build resilient and scalable platforms addressing key areas of compliance, risk management, documentation, resilience and transparency - all in real-time.

In short, the BaaS model is far from broken. It simply needs a refined approach, leveraging the strengths of incumbent banks to build a more resilient, compliant, and innovative financial ecosystem. Let's not throw the baby out with the BaaS water.

Is WealthTech the future of advisory?

WealthTech is shaking up the financial advisory world. But does it mean the end of traditional wealth managers, financial advisors and RIAs?

🌎 Macro opportunity

The Great Wealth Transfer is upon us. Over the next 25 years, around $68T will pass from Baby Boomers to younger generations (Cerulli Associates). This massive transfer is a golden ticket for Fintech companies ready to transform financial advice. Using technology can democratize access to top-tier advice, boost efficiency, and offer ultra-personalized strategies. This goes beyond what robo-advisors like Betterment (over $29B in assets, 700,000+ clients) have done in the past decade.

📊 Market Trends

WealthTech startups raised ~$4B in 2023 and $500M in Q1 2024 (CBInsights). Several trends are driving this rapid adoption:

- Hyper-personalization: today’s clients want unique advice. With Plaid or MX, RIAs can aggregate financial data from multiple sources to deliver personalized advice.

- Behavioral finance: platforms like Addepar, Nitrogen Wealth or Vanilla deliver tailored strategies and help advisors align investments and estate planning with clients' risk tolerance, using behavioral finance to guide decisions.

- Democratization of alternative investments: Securitize/Onramp Invest lets RIAs include crypto assets in portfolios, modernizing wealth management.

💥 Impact on Business Models

WealthTech is transforming RIA operations in several ways:

- Efficiency and automation: Vise or Orion automate portfolio management tasks. Advisors can manage more clients without a proportional increase in costs, boosting profitability and market share. Cost savings may be passed on to clients.

- Comprehensive planning: advanced analytics and data aggregation help RIAs craft more holistic plans. Tools like Envestnet or Asset-Map improve client engagement and visualization of financial situations. This often translates into stronger client retention and can justify higher fees or fee-for-service models.

- Tax planning: other tools automate tax return analysis, integrating into broader financial plans.

WealthTech also enables more flexible pricing structures. Traditional AUM fees are being supplemented by subscription-based models, flat fees, and performance-based fees. This allows RIAs to attract a broader range of clients, including those with lower AUM.

In short: WealthTech isn’t about pushing traditional wealth managers out, but augmenting them. With technology, they can blend high-tech and high-touch services. This shift may be gradual, and many WealthTech companies will need a longer runway to crystallize this opportunity. Partnering with investors who seek durable expansion is key. By balancing capital and operational discipline, structured growth equity might help them stand the test of time — through the Great Wealth Transfer.

Move money or make money?

From embedded finance to real-time payments (RTP) to tokenization, payment technology is changing not just how transactions occur, but also the payment ecosystem as we have known it so far.

🌎 Macro opportunity: according to McKinsey, payments revenues surpassed $2.2 trillion in 2022 (an all-time high), with electronic transactions growing at nearly triple the overall rate of payments revenue over the past 5 years. This growth trajectory is fueled by digital adoption, particularly through mobile devices, consumer demand for fast, contactless and secure payment options, and even regulatory support for cashless economies.

📊 Market trends: with the integration of financial services into non-financial platforms, any business can now offer payment, rewards, BNPL or insurance directly to users. New integration modalities like Open Banking also enable non-banking entities to offer financial services via APIs. Partnerships between fintech firms and traditional banks are increasing, although regulatory scrutiny may intensify following recent incidents (read: Synapse). Real-Time Payments (RTP) are making instant transactions the new standard, and tokenization is enhancing security and reducing fraud. Technology also allows for tailored payment solutions across industries (checkout for e-commerce, patient medical billing for healthcare, illustrated by the recent Waystar IPO).

💥 Impact on business models: by automating processes, digital payment technology expands access and cuts transaction costs. Businesses can better serve and retain customers by embedding payments and value-added services in their user flows. For solutions providers, the traditional take-rate model may prove its limits, despite increasing volumes, as efficiency and sometimes regulations are driving transaction fees down.

In short: RTP and A2A (Account-to-Account) on the one hand, web3 and its disintermediation on the other hand, will lead to a gradual erosion of interchange fees. Neo payment businesses solely relying on take-rate may be caught in a race to the bottom, challenged to maintain decent net revenue growth despite higher processing volumes. Unless they add a compelling service layer that can justify minimum commitments or subscription from their client base, or unless they solve a uniquely complex problem in specific (regulated) verticals, many may end up being “consolidated” on unfavorable terms. They should revisit their revenue model and recalibrate their current operations with new backers able to provide capital runway and operational support. So they can make money by moving money.

When it's not primary, is it secondary?

Recent trends in investment activity present a mixed outlook for different types of investments and investors’ risk appetite.

☁️ Primary: global venture funding amounted to $66B in Q1 2024, per Crunchbase. While it increased by 6% from the previous quarter, it is down by 20% from the same quarter in 2023 and marks the second-lowest quarter for global startup funding since early 2018. AI ($11.4B, or 17% of the total global funding) and healthcare & biotech ($15.7B, or 24% of the total) remained prominent. This data also suggests a shift to earlier-stage investments: $7B raised by seed-stage startups (down from 2023 but higher than 2020), and $29.5B by early-stage companies (up 6% YoY). Late-stage experienced the most significant pullback, with ~$29B raised (down 36%).

🌤️ Secondary: the allocation of funds towards secondary strategies reached nearly $118B across all asset classes in 2023, underscoring their growth potential and investor interest. By asset class, PE secondaries represented 85%, at almost $100B. Secondaries allow GPs, LPs and employees to sell their stakes without waiting for traditional exits like IPOs or M&A. This resurgence is influenced by improved valuation spreads, and investors looking for high-quality, proven assets.

In short: venture capital investors remain cautious and selectively optimistic amidst a backdrop of economic adjustments. On the secondary side, there seems to be a growing appetite for alternative liquidity options. Structured growth equity strategies could enable investors to diversify into a less volatile asset class with stronger risk-adjusted profiles. By providing capital and operational assistance, they help recalibrate businesses in a non-ZIRP environment, making them self-sustaining and attractive for future M&A exits.

Is venture liquidity in stagnant waters?

The venture capital market is experiencing a significant bottleneck in the United States, with about a billion dollars of illiquid capital.

⛓️ Illiquidity: the value of mature U.S. startups awaiting exits nearly hits the $1 trillion mark through Q3 2023 according to PitchBook data. The backlog predominantly consists of companies that are in the "venture growth" stage (Series E or later), or companies over 7 years old with at least six VC funding rounds.

- SaaS: $532.4B

- AI/ML: $240.7B

- Fintech: $208.4B

🌵 Challenges: with more than 1,500 unicorns waiting for an IPO (Crunchbase data), the exit bottleneck is a critical issue for venture capitalists, impacting their key performance metrics like distribution to paid-in capital (DPI). LPs' sentiment is influenced by the backlog, affecting their future investment decisions in the venture capital space.

📉 Exits: in 2021, the market saw $157.6B in exits from venture growth-stage SaaS companies alone. The 2023 exit activities are significantly lower, with only $28.2B in IPOs, indicating a drastic slowdown compared to previous years.

In short: the current pace suggests a prolonged delay in exits for mature startups, exacerbating the capital lock-up issue for investors, and runway concerns for many founders. The ongoing stagnation in the IPO market has broader implications for the VC ecosystem and its stakeholders. Structured growth equity strategies could be a solution to the current overhang by providing founders the capital and operational assistance to continue building, giving investors access to a long-term structural opportunity, and making the startup ecosystem stronger.

When it’s low, how can it bounce back?

The recent fluctuations in venture capital funding have impacted the Fintech industry, confronting companies with valuation challenges and existential questions.

🤑 VC Funding: venture capital investment in fintech decreased substantially, from $141 billion in 2021 to $39 billion in 2023, according to CB Insights. This reduction has prompted many Fintech startups to conserve cash to avoid fundraising at much lower valuations.

📉 Delayed IPOs: in response to the market conditions, many mature Fintech companies have postponed their initial public offerings. The value of already-public Fintech firms has fallen by approximately 50% from their peaks despite the S&P 500 and Nasdaq’s recent new highs. Some reputable public companies, like Bill, are down ~80% since their late 2021 peak.

🧮 Private valuations: @CaplightData, a San Francisco startup that tracks secondary-market trades of private tech companies, has shared with Forbes its estimates confirming the declines in value from fundraising peaks. Valuation drops can be dramatic (~79% for Klarna and ~74% for Chime) and illustrate persistent volatility. To be fair, the accuracy of secondary market valuations can be affected by the small transaction sizes and various seller motivations.

🚦Industry Insights: signs are emerging that valuations in the Fintech industry may be stabilizing or even improving for certain leading players, hinting at a potential market recovery. While the optimists might see a bottom, it remains tough to call without more fundraises or exits. This might leave many mid-stage Fintech scrambling to explore their options.

In short: buying time through down or insider rounds might be untenable for most Fintech startups. More founders and investors should consider alternatives for startups that don't exhibit the potential for IPOs or fund-returning outcomes. Structured growth equity strategies could offer investors better liquidity options and keep mid-stage startups in business by injecting capital and recalibrating their operations until their economics, not just market, bounces back.

Can founders get a second bite at the apple? 🍏

Many founders, particularly in Fintech, are at a crossroads. While their startups demonstrate solid revenue and product-market fit, their tapering growth disqualifies them from traditional VC follow-on funding. How can they extend their runway?

🏛️ Capital raise: with Fintech VC investments down 44% in 2023, funding remains tight despite more positive signs in Q1. Many venture-backed startups find it hard to secure follow ons as VC firms tend to focus on their best performers to maximize returns and DPI. Startups with modest or linear growth face less appealing fundraising options: insider or down rounds, harsher terms, and sometimes no funding at all.

💵 Non-dilutive financing: revenue-based financing and term loans have emerged as a popular alternative for startups keen on preserving their equity. However, these options require startups to sustain revenue growth that significantly surpasses capital costs to avoid jeopardizing repayment and financial stability. The same logic applies to venture debt to a large degree.

🏷️ Company sale: it offers another avenue for founders (and their investors), but they need to find a suitable counterpart. There are early signs of renewed M&A activity, but smaller companies might surprisingly wrestle to find buyers even at lower valuations. Founders should consider putting extra work to recalibrate and operationalize their business before selling: it will make it more acquirable, hence valuable, compared to a quick sale.

🙌🏻 Structured growth equity: this innovative option involves selling a controlling stake (majority or minority paired with preferential rights) to a fund or qualified sponsor, enabling the founder to retain substantial equity in the new venture. This approach provides capital for growth and a potential future payout for the existing founders and investors once the business has been rebooted then exited at a higher valuation.

In short: funding is a propellant for (business) rocket ships: it accelerates the growth of exceptional teams and ventures, and delivers similarly exceptional returns. But most startups, in Fintech and beyond, are meant to be steady businesses with robust growth. For founders who won't achieve a venture scale outcome, structured growth equity is a viable financing solution that combines capital with operational expertise. It preserves significant upside for founders, so they can get their fair bite at the apple 🍎.

Is AI eating the venture world?

AI investments took the lion’s share of global VC funding last month. Those who apply AI to specific use cases and industry sub-sectors might be the ultimate winners.

📈 Trends: global venture capital funding was $21.5B in February 2024, stable compared to January 2024 and slightly up from February 2023, according to Crunchbase. The investments were distributed across different stages, with over $2B in seed-stage, ~$10B in early-stage, and ~$9.3B in late-stage.

🤖 AI: with $4.7B, AI companies captured 20+% of venture funding in February 2024, up from $2.1B in February 2023. Some companies closed massive rounds (~$1B for China-based Moonshot AI, $675M for Figure, $320M for Lambda, $200M for Glean) in hope of big returns. AI could double or triple the current $600B software spend over the next 5-7 years, according to Dharmesh Thakker from Battery Ventures.

🏦 Fintech: in Fintech, AI goes beyond mere automation: it can unleash new approaches to predictive analytics, personalized investment strategies, real-time financial decision-making and fraud avoidance. By integrating and analyzing diverse data sets, it supports swifter decision-making, new business models, and expands access to banking, brokerage and insurance services.

In short: let’s not forget that AI is an enabling technology; a means, not the end. Success and adoption happen when they are tied to novel, compelling use cases that drive higher efficiency and better user experiences. In Fintech, the injection of new AI-driven processes could help reverse the current down sentiment. But reconfiguring these companies’ operations will require new structured growth equity investments and the support of experts who can marry capital with operational expertise, and orchestrate Fintech’s next chapter.

had v interesting convos with community bank (CB) executives at FTMU2024. CBs are the expression of a diverse & decentralized banking system; their vibrancy is a key to competitive and accessible credit, & a safety against increased vertical integration between government & credit.

two things will happen

1. Community banks embrace differentiating technology in this cycle

2. Technology adoption is key to relevance

https://t.co/XT6fpEVVwl

When clouds are low, who keeps flying?

Fewer Fintech VC deals drive a flight to quality and a diversity of exits.

📊 Trends: Fintech VC investments dropped by 43.8% to $34.6 billion in 2023 (PitchBook data). Payments, alternative lending, capital markets and CFO stack startups received most funding, with generative AI and open banking supporting their attractiveness. Pre-money valuation step-ups declined across all deal stages with a median of 1.5x, a 26.8% decrease from 2022. The trend towards lower valuations may continue into 2024, if companies keep depleting their cash reserves.

📎 B2B: in 2023, Fintech VCs showed a marked preference for B2B companies. They received 72.1% of the total funding, up from 40.6% in 2019, while B2C fintechs garnered only 27.9%. This shift reflects investor confidence in B2B's superior exit opportunities, the over-saturation of B2C fintech, with a backdrop of high interest rates and geopolitical tensions. These economic pressures have impacted consumer financial stability, whereas B2B firms seem to have more reliable revenue streams and access to larger markets.

🛫 Exits: with $5.9 billion in Fintech VC exit value across 185 exits, 2023 had the lowest exit value since 2016 and the fewest exits since 2020. M&A activity also fell by 33.6% to $47.1 billion. Despite these downturns, there has been relatively robust levels of (late-year) M&A and buyouts. It suggests a Fintech market potentially poised for consolidation.

In short: while volumes are markedly down at the top of the Fintech investment funnel, the liquidity overhang and transaction backlog might start clearing if IPO conditions improve and if startups reset both their valuation expectations and operations to adjust to normalized conditions. Alongside stronger M&A and buyout exit trends, structured growth equity strategies could offer investors better liquidity options and keep challenged startups flying at revised altitude.

The past 2 years have been brutal to the Startup ecosystem.

Darwin is back and capital has become less available and more expensive.

Many startups haven’t gotten “far enough fast enough” and can’t raise the capital they need to survive.

So it shouldn’t come as a surprise that M&A is a topic that’s coming up more and more frequently in Board rooms as a way of “landing the plane”.

A few thoughts:

One framework that I’ve found useful when helping Founders and Boards figure out if M&A is possible is based on a concept that I call “Climbing the Relevance Curve”.

At the core of “relevancy” are two simple questions:

1) Will anyone care if the startup closes shop?

2) How much money is the startup burning?

The questions might seem incredibly basic on the surface but the answers to these questions speak volumes about a startup’s options.

Will Anyone Care?

At the foundation of “relevance” is the concept that a business is either relevant or irrelevant through the lens of a counterparty.

The all-important question to ask is who (if anyone) would be significantly hurt if the business were to go away tomorrow?

When a startup would be missed it has intrinsic value. When a startup is serving a necessary function for its customers then if it were to disappear its customers would have to seek a replacement. And the worse the replacement options are the more a startup is worth.

How Much Money is Being Burned?

The second piece of the framework requires understanding how much money a startup is burning and how much total capital it will need to turn profitable.

There’s a fine line between buying an asset and buying a liability.

The answers to these questions should crystalize who the “today” buyers are as well as a rough idea of when a startup becomes relevant to “tomorrow” buyers.

Relevancy matters because buyers won’t go through the brain damage of acquiring a startup that isn’t relevant TODAY.

If a startup has no deep-pocketed counterparty that deems them as “relevant” then it has no choice but to rely on Investors or free cash flow for support while it continues to climb the relevance curve and wait out bad market conditions.

Distance from relevance is very important because the best VC backed startups grow at an amazing pace. Many startups can deliver 2X+ annual growth rates which implies that relevance is a function of time for high growth startups.

Investors can choose to infuse capital into a startup if it isn’t relevant yet but is climbing the relevance curve quickly.

But the converse is also true. If a company isn’t becoming relevant quickly enough then new capital might increase exposure rather than generate value.

A low growth startup that’s burning fistfuls of cash will be seen as an albatross while a high growth startup that needs a small amount of capital might be seen as an asset.

Being “default alive” with a few tweaks is a strong position to be in while being “default dead” isn’t.

What about proprietary tech? What about an embedded user base? What about IP?

A rule of thumb about the value of these assets is simple.

In “risk on” markets, value can be ascribed to “soft assets”. Good money will be paid for well built tech and sizeable customer bases.

But value them at zero when market conditions aren’t favorable. In “risk off” markets, assets that aren't "cash equivalents" or "immediately sellable" that are owned by money losing startups typically normalize to a valuation of zero. This is sad but true.

While some may think I’m being overly harsh and too “black or white”, the relevancy framework is based on real conversations I’ve had in the past with sophisticated acquirers. And FWIW, I’m having similar conversations today that make me believe that the framework is valid.

The TL;DR: I’ve watched this climb many times across many different business models and business cycles and the story is the same. Becoming “relevant” is not just important, it might actually be the most important metric for a startup to track.

And FWIW – I feel like these concepts are critically important for the entire ecosystem to internalize. If you agree, the best thing you can do is like and share. If you don’t agree, I’d love to hear your feedback in the comments!