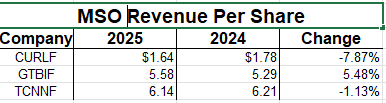

$GTBIF had positive growth in revenue per share of 5.48% in 2025 because its revenue rose and shares declined, while $CURLF & $TCNNF had respective revenue per share declines of 7.87% & 1.13% because their revenues declined & their shares increased. $MSOS

@TJTheWheelDeal I never understood why people listen to other who have made such poor decisions in their life

listen to the ones who haven't you'll learn a lot more.

@TJTheWheelDeal im going through a divorce and have lost all my money. Spent over 20k on attorney fees and shes still going for custody. she gets 225k of my port and Im paying all bills we used to split!

She want my kids! Never!

A true dad never quits, never goes away! I'll never stop!!

I’ll have to adjust this goal post trade for the next couple of years in order to manufacture the win.

Zero intention of owning shares here unless new CEO makes some very compelling moves.

In the meantime, I will keep grabbing massive naked call premiums every 30 to 45 days until she rebounds.

If she doesn’t rebound in a year, I’ll roll the puts out and down another year at that point.

I’ll feature this position every month or so just to keep tabs. Not a lot to see here until we get closer to naked call expirations.

$GRAB Conversation with a Friend abt Shortie🧵

My friend called this morning and asked why short sellers keep shorting this company?

Context: He owns a large position on $GRAB too, I think he said 20% of his portfolio with low average as he bought heavy during April selloff.

Roughly $1 billion is used to short $GRAB now. Very high conviction for the last 16 months.

I asked, tell me more about the company. How much Cash Grab is generating excluding Financial lending?

I asked how was GRAB service during his trips to SEA?

It seems most still don't understand how much Cash Grab is generating. By Q3 2026, when GrabFin is profitable, Grab will probably Generate $1.5B from Q3 2026 to Q3 2027.

Adjusted FCF

Q2 2025: $112m

Q3 2025: $203m

To generate this kind of significant cashflow proves GRAB MOAT is strengthening and dominating most market share (70-75%) and soon to be 90-95%. Meaning "Bottom of Pyramid" is not a concept/theory anymore, it is financial viable and sustainable.

Grab is only 6.5% penetration in 700m population, and only 14% thesis of 5B people.

As far as shorting, short sellers were correct that SEA economies are in bad time, especially from 2022, when our @federalreserve and other central banks started the most aggressive QT program in monetary policy's history.

SEA economies continued to worsen and these countries are running $50B+ in stimulus. Lots of disruption, but it is showing signs of great recoveries and resilience, particularly this Q4 2025.

Looking back, $GRAB still manages to grow 54% average 2022,2023,2024 and 2025. And the business is projected to grow 30% or higher without $GOTO Mobility/Delivery, or 76%-80% if acquired $GOTO on-demand segment.

What short sellers failed to see, all GRAB competitions are burning cash or accumulating debt at a crazy pace that would push them to bankruptcy in 2- years. FoodPanda would have $0 today if they pay all debt, interest and liabilities. $GOTO would have 3-4 quarters of cashburn if they pay all debt today. And Xanh is not a serious competitor, so I wont bother.

GRAB MOAT is its ecosystem that will push market share to 90-95% in 2-3 years or after Goto acquisition. Then we get into quick-commerce, which is another Trillion dollar TAM to delivery within 15-60 minutes. I will link the detail thread below, since I dont want to make this thread too long.

So after the conservation, it turned out my friend couldnt answer most of fundamental questions. He followed my suggestion on GrabUnlimited and Travel Package, he was able to save $400-$500 and got to try some awesome "Dine-Out" places. I was not trying to test him or anything, but you have to know what you own.

Short sellers are paying $6-$10m margin interest per month now, who care. I'm not paying interest on my shares. I'm here for the long term. If you deduct the cash and equity investment, GRAB is trading at less than 1 P/S for FY 2026. This is the multiple for a bankrupting business with collapsing revenue.

GRAB is the opposite:

~$7.4B Cash with very little debt

~$4.4B Equity Investment

~30%+ Growth

~Positive Operating leverage

~About to generate $1.2-$1.5B in FCF

~Core Fin segment is abt to be profitable in 5 months

This is during "bad" time in SEA, what about 2026-2036 are all "good" time? that will mean 40-50% growth with massive Cash Generation that will go to long term shareholders. And that is why I don't care about short sellers or near-term price action.

Find me a US company with this kind of balance sheet, Equity Investment(up 400% in 3 years), and this kind of growth + FCF generation at $19B MC with soon 90-95% market share in a very young population of 700m people. And this is why GRAB is a major position for me. And I like my core position at beautiful discount like today.

Alright, that is it.

Not Financial Advice!

@TJTheWheelDeal This a sign or what?! I'm doing it right now. My wife is divorcing, and I'm asking him, how can I be okay when I'm alone and excluded? I'm praying in bed.