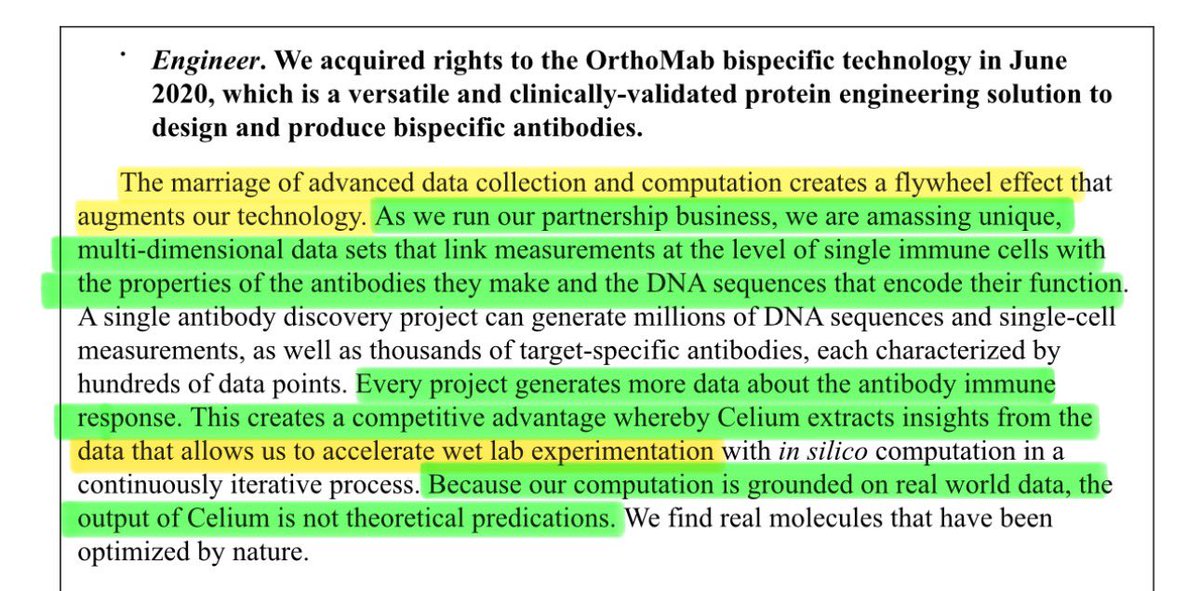

$ABCL platform molecular efficiency is starting to look really beautiful.

From 1 molecule in the clinic in 2020 to 19 by 2025, 17 partner-led, 2 Abcellera-led.

$ABCL might be showing early biotech business operating leverage: compounding output and derisking in real time.

$ABCL earnings (Q4 2025)

Revenue : $44.9M vs. $6.67M [est] (beat by +570%)

EPS: $-0.03 vs -$0.134 [est] (beat by +77%)

Cash : $700 million

ps : will share more details shortly :)

Jane Street's entire business model is generating fake price directionality through constant, repeated HFT momentum ignition (huge leverage on small positions), and luring retail in. Then it rugs everyone right after it cashes out.

It’s been a little over a year since I wrote my first article on AbCellera. Here’s an update of what I’m looking at for the rest of ’26 and beyond:

A development over the past year has been the company’s shift towards prioritizing in-house molecules. They successfully moved ABCL635 & 575 into the clinic in 2025.

With 575 being a treatment for atopic dermatitis and other immunology/inflammation areas by targeting OX40L, the company had mentioned many times on calls that they’d be looking at clinical trial readouts from Sanofi’s Amlitelimab as a sort of benchmark for how effective 575 might be. The sentiment around amlitelimab’s readouts seemed to be that it was rather underwhelming. And being that the space of this drug is crowded, I do not have my heart set on 575 moving forward. The plan is likely for AbCellera to finish phase 1, and if the readouts are favorable, look to hand it off to a partner. But who knows if a partner would want it at this point. Those readouts should come near the end or ’26. We’ll see what happens. If it doesn't get handed off to a partner, it has no impact on my overall thesis.

ABCL635 is what really excites me. While the company hopes 635 will be a first-in-class antibody therapy for women’s hot flashes, the part I’m really excited about is the fact that it’s GPCR-targeting. There have only been 3 GPCR targeting antibodies approved in history. The molecule has already moved into phase 2 with readouts expected to be late ’26/early ’27. If readouts are positive, the molecule would move into phase 3. This is where I believe we would start seeing real momentum behind the stock, although I don’t have a price target. What I’m looking for here with 635 is validation of the company’s GPCR platform. One of the major obstacles with targeting GPCRs with antibodies is the process of obtaining highly pure GPCR antigens to generate an immune response from. AbCellera acquired Tetragenetics in 2021 to expand its capabilities for generating antibodies against difficult to drug transmembrane proteins like GPCRs.

Not long after ABCL635 entered the clinic the company accounted ABCL688, another GPCR-targeting molecule that will be entering the clinic this year. This period is a make-or-break moment for AbCellera. And given there’s only been 3 GPCR-targeting antibodies approved in history, it seems to me like AbCellera is highly confident in their GPCR platform. Out of the 4 in-house molecules they’ve announced, half of them are GPCR targeting.

I believe something like 36% of approved drugs are GPCR-targeting. But they’re pretty much all small-molecules. So, if AbCellera can prove their GPCR platform works, I believe the company will be off and away towards success. More information on GPCRs: https://t.co/JGbHeuZfa9 “With more than 800 members, GPCRs are one of the most diverse and important families of human proteins”.

Because of this, ABCL635 is my biggest focus for now.

Another exciting development has been the recent accouncement of ABCL386, another in-house molecule by the company. This one is in the area of oncology, but the exact details are not yet disclosed. Due to the company’s ongoing posters published of their work in T-Cell engagers, I wonder if it could be a T-Cell engager.

Speaking of T-Cell engagers (bi-specific), I continue to keep the AbbVie x AbCellera partnership (expanded in Jan’ ’25) in the back of my mind. In July of 2025, AbbVie and IGI announced a licensing agreement for a partnered trispecific antibody. This included an upfront payment of $700M and up to $1.225B in milestone payments with double digit royalties on net sales. If AbCellera could strike a deal anywhere remotely close to this one IGI did with AbbVie, it would be massive for the company.

Lastly, regarding the pipeline, I continue to keep an eye on AbCellera’s founding partnership with Abdera (https://t.co/SA09S9r9i2). AbCellera discovered Abdera’s radiopharmaceutical ABD147 and the phase 1 study is estimated to be complete in Jan’ ’27. The molecule targets small cell lung cancer. Another molecule in Abdera’s pipeline that I believe was discovered by AbCellera is ABD-320, which is another radiopharmaceutical biologic.. this one is for solid tumors and is anticipated to enter clinical development in the first half of 2026.

Some other news over the past year that is somewhat significant was AbCellera’s win over Bruker regarding the ’408 microfluidic cell culture patent family. While in my initial article I declared this as a potential thesis-breaker if AbCellera lost, I changed my mind over time as I continued to think about the value of their head start on the vast amount of in-house data from discovery campaigns and the feedback loop as a result(https://t.co/PU5ZBQCpff).

Nevertheless, AbCellera successfully defended their IP, so I don’t have to worry about it anymore. The settlement was somewhere around $36M I believe as well as future royalty payments on the sales of Broker’s Beacon optofluidic platform. The up-front of $36M is not much. I am curious to see what the royalty payments could look like but am seeing my expectations limited.

Finally, the great Stephen Quake has joined AbCellera’s board of directors. The relationship between Quake and CEO Carl Hansen was one of the original pieces that helped me start building my ABCL thesis. Quake is considered to be one of the most famous researchers and a pioneer in microfludics, in which Hansen worked under him as a postdoctoral fellow in Quake’s labratory. He basically said Hanen was one of the brightest students he ever worked with: https://t.co/G6u7CHlJcE and given Quake’s ties to Priscilla Chan and the Chan Zuckerberg Initiative, I believe he will be a great addition to AbCellera’s board. I also found a scholarly article last year highlighting the importance of Quake's mentorship to Hansen: https://t.co/9DTOCFcZJT

Speaking of Quake’s ties to Priscilla Chan, I found this conversation between the two of them to be interesting: https://t.co/xg0h9pqZP3 This is regarding the “AI Virtual Cell”. Given Quake’s ties to this and his new position on AbCellera’s board, it makes me wonder if the company’s massive amount of data generated from its discovery campaigns could be useful for this virtual cell effort in the long term. While my thesis is based on my belief that using a natural immune response from Mother Nature as a database and doing a deep search through it via microfluidics in superior to de novo AI design (due to human biology being infinitely random and complex), I do believe that if any company in the antibody space will be able to leverage AI for some sort of testing/design (long term), it will be AbCellera, do to the massive amounts of high quality data they’re constantly generating.

Since I published that article in Dec ’24, the stock is up about 14%. So basically it’s been dead weight in my portfolio. As of today, I’m down about 18% from my $3.89 average. I increased my position by about 30% earlier this year @ $4.42, bringing the stock weight to about 15% of my portfolio. When I wrote that article last year, I already had way more shares than I ever thought I would... I have since increased that position by about 2.6X again. $ABCL is the only stock I’ve been purchasing over the past two years and I will look to continue to add when possible. In retrospect, I should have waited to buy and the opportunity cost has hurt. But I continue to believe this company has an incredibly bright future and believe this year will be the inflection point.

In summary, there's a lot I'm excited about but I'm mainly looking for positive ph 2 readouts on 635 end of year, moving it into phase 3. If that happens, I believe the company is on its way to success.

Long and strong.

![10xValueMind's tweet photo. $ABCL earnings (Q4 2025)

Revenue : $44.9M vs. $6.67M [est] (beat by +570%)

EPS: $-0.03 vs -$0.134 [est] (beat by +77%)

Cash : $700 million

ps : will share more details shortly :) https://t.co/IbubKxUe0X](https://pbs.twimg.com/media/HB9I93LaMAk4bMm.jpg)