$SIVE is the most compelling CPO exposure stock to me.

Despite the volatility.

You probably won’t find something like this again until the next architectural shift in photonics years later.

Out of the core laser suppliers, they’re all tens of billions?

$AAOI = $15B

Furukawa = $26B

$MTSI = $29B

Sumitomo = $59B

$COHR = $73B

$LITE = $74B

Then there’s $SIVE as one of the core CPO laser chokepoints at $2.3B MC.

Earnings are usually confirmation of all the little volume ramp hints like Jabil fireside transcripts for 1.6T LRO.

And most returns are typically made before, not after official confirmation is just a rule of thumb.

The "unusual flow" that many of you saw on Ballard Power $BLDP last week on May 15th, was us. The stock is breaking over $5 today, and our $5 calls for August are already up +130%

This is the thesis I shared with our members on 5/15, highlighting Ballard Power's datacenter validation at Microsoft $MSFT Cheyenne, Wyoming datacenter:

OVERVIEW: I believe this is one of the most compelling charts on the entire market and also one of the most compelling sympathy trades, as one of the only peers to both Bloom Energy $BE and FuelCell $FCEL, which have both been parabolic stocks.

Ballard is a high-optionality hydrogen fuel-cell platform with a unusually strong cash balance for its size, improving gross margins, and credible OEM relationships in buses, rail, marine, and stationary/data-center power. In the last earnings call, Ballard's CEO Marty Neese explicitly said that the data center opportunity is an area of deep exploration for the company and they plan to pivot into it going forward.

Diesel generators face emissions, permitting, noise, and runtime concerns. Data-center operators still need reliable backup power. Hydrogen fuel cells can provide zero on-site emissions.

Ballard’s data centers use case shines where PEM fuel cells can support reduced time-to-power, backup power, complementary power, rapid ramping, cycling flexibility, reliability, low noise, and modular multi-MW deployment. The company has a real business and trades at just 2.3x cash and 2x book with revenues +26% Y/Y. But more importantly, the technical picture has an extremely powerful setup, and in light of the recent BE sympathy bidding behind FCEL lately, there is a legitimate angle here.

It's also worth noting that while the market is currently pumping FCEL as the BE sympathy, BLDP & FCEL have basically the same EV/sales multiple while BLDP is currently reporting a POSITIVE consolidated gross margin (9%), while FCEL is reporting a NEGATIVE consolidated gross margin (-16%).

TECHNICAL PICTURE: On the daily, $BLDP is flagging retesting the breakout from a 9-month base. On the weekly, the stock has aggressively broken thru the 200-week moving average for the first time since 2022 (when it was trading $12+). On the monthly, the stock is pushing into the flat 200-month moving average overhead with the 9&21-month EMAs curling up below price. This is a drop-dead gorgeous chart and I think one of the nicest SMID cap charts in the entire market.

TECHNOLOGY VALIDATION: Ballard and Vertiv $VRT one of the nation's biggest power & cooling infrastructure players in the datacenter theme (a $144 billion market cap) announced a strategic technology partnership in June 2024 focused on backup power for data centers and critical infrastructure. The initial solution integrated Ballard fuel-cell power modules with Vertiv’s Liebert EXL S1 UPS platform at Vertiv’s Ohio facility. The system was designed to scale from 200 kW to multiple megawatts.

In the North American market as a validation of their fuel cell engines, Ballard announced a commercial agreement with New Flyer for 500 FCmove-HD+ fuel cell engines, totaling 50 MW. Deliveries are expected to begin in 2026, and the engines will power New Flyer’s Xcelsior CHARGE FC hydrogen fuel cell buses across North America. Ballard said this is New Flyer’s largest single commitment since the partnership began, and the relationship spans more than a decade.

In January of this year, they announced perhaps their biggest validation ever: Caterpillar, in collaboration with Microsoft and Ballard Power Systems, was recognized for its work in datacenter hydrogen fuel cell technology, winning the ‘Systems Development and Integration’ award at the U.S. DOE's Hydrogen Program Merit Review Awards.

The Ballard Power Systems-supported project successfully demonstrated its megawatt-scale fuel cell platform at Microsoft’s Cheyenne, Wyoming, data center. The 1.5MW fuel cell and battery microgrid solution showed increased resiliency and lower carbon intensity, providing applicability beyond standby, over a simulated 48-hour outage.

I've filled an equal position in both the $4C @$0.90 and $5C @$0.60 for August expiration

I believe $ONDS is poised to win the FIFA World Cup contract. $Sentry's’ passive RF technology enables operators to detect, identify, track and neutralize drones without GPS or kinetic engagement. When combined with Iron Drone’s autonomous interception system, Ondas win.

Ondas reported record Q1 2026 results with $50.1 million in revenue, raised its 2026 revenue target to at least $390 million, and expanded pro forma backlog to $457 million.

The quarter reflected accelerating demand across counter-UAS, ISR, and autonomous systems markets while advancing Ondas’ global operating platform and AI-enabled multi-domain ISR strategy. $ONDS

https://t.co/q635nUZDdF

It’s still pretty incredible $HIMS is down 44% even after:

1. $NVO de-risking + partnership

2. Multiple global acquisitions expanding DTC distribution network

3. Peptide arc, with Huberman saying HIMS was set to soar under these conditions

4. Entering a friendlier macro climate.

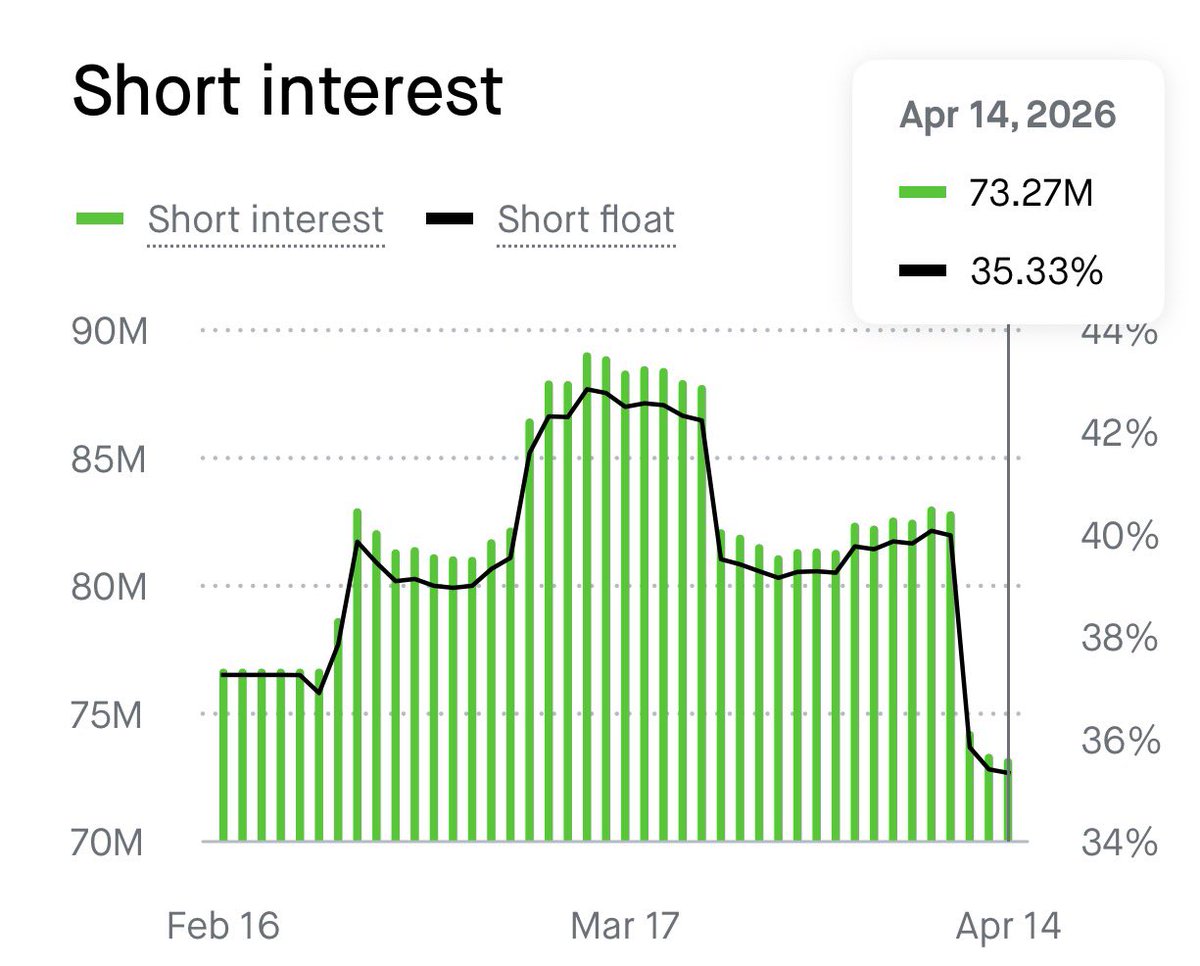

5. Short interest reaching unsustainable 36%+

The good news is: short interest can only be so much of the float… So it’s inherent buying pressure to cover over time, which does limit downside if fundamentals improves.

This announcement is the most bullish catalyst for $HIMS revenue re-acceleration to date.

This is amid:

- 30%+ of the float sold short

- new $NVO partnership/lawsuit dropped

- new global acquisitions

- recovering macro climate.

The share price is still $25, down from $70 last year.

Short sellers are likely in trouble:

$HIMS can capture market share at the ~70%-80% gross margins typical of their compounded products for the holy grail of the "Grey Market" TAM for peptides.

- EG. Healing: BPC-157 and Thymosin beta-4

- Hair & Skin: GHK-Cu

- Weight Loss & Muscle: MOTS-c and Ibutamoren

And now they're probably the world's largest independent DTC distribution network to date from their new acquisitions...

So just running a peptide protocol subscription between $150 to $300, for 200k subscribers is $360M+ in high-margin ARR.

As just one example, but now they have a worldwide net of customers.

They burned through capex last year to acquire peptide manufacturing facilities too... so now that's turned into a massive cash-cow business.

I said $HIMS would need fundamental changes in order to force shorts to cover, and this is probably that signal as seen with market data.

And $HIMS is turning into a fundamentally sound company after regulatory de-risking.