“A great business at a fair price is superior to a fair business at a great price… The investment game always involves considering both quality and price, and the trick is to get more quality than you pay for in price. It’s just that simple." - Charlie Munger

@ByteTree Quality is an investment research service which does exactly that.

#Quality #Investing

https://t.co/yx5VRE0Ow3

Alphabet is about to do the largest equity sale in history.

Bigger than SpaceX's IPO.

Bigger than Petrobras in 2010.

Nearly 3x Aramco's 2019 IPO.

$80 billion, in a single equity raise.

The previous record holders were both oil companies at the peak of their cycles.

🇧🇷Petrobras in 2010: $65 billion to drill the pre salt ultra deepwater fields off Brazil the biggest oil discovery in decades. The market couldn't get enough.

🇸🇦Aramco in 2019: $25 billion to monetise the world's largest oil reserve. The most profitable company on earth going public. Still the largest IPO ever at the time.

Both were energy. Both were oil. Both represented the dominant capital deployment thesis of their era.

Now Alphabet an AI company, is about to raise more than both combined.

Not to drill. Not to pump. To build compute.

The capital cycle has rotated completely.

2010s: the world's largest equity raises funded oil megaprojects deepwater, pre-salt, sovereign oil reserves.

2026: the world's largest equity raises fund AI infrastructure data centers, GPUs, power.

Do not miss my latest analysis on oil prices����

Super interesting piece on Claude Code and disruption threat.

"This pattern is familiar. We replaced shovels with excavators, and then we built skyscrapers. We replaced manual arithmetic with calculators, and accountants did not vanish; they did more interesting work, if you can believe it. Each time a tool made a job easier, we didn’t run out of things to do. We found bigger things to do."

https://t.co/41TyQVuATe

A former SK Hynix strategy director with 34 years in memory:

"They may order in advance, maybe a year, because the cycle time normally takes one year. But even though they ordered, they may delay the actual adoption. Even though the equipment installation is done, they may delay the input of wafers. There are many ways that they can delay to see the market situation."

Animal spirits are in play once more.

In 1999, Pets .com was one of the most famous bubble stocks, commanding a huge market cap with little to show for it in business terms. It went public at $11 a share in early 2000, near the peak of the dotcom bubble, with backing from Amazon and Merrill Lynch, and went bankrupt a year later. Today, a different bubble is forming.

https://t.co/6vai9U0oPq

Why did Intuit $INTU command such a huge premium over Sage $SGE?

Faster cash flow growth since 2008 (INTU in blue).

Interestingly, it's not just US buyback culture - SGE has bought back a greater portion since 2011.

Looks like the main error was giving it such a huge premium in 2021 - a time of so many poor decisions.

For investors now, it's key to be aware of anchoring bias, and not get sucked into thinking that anything from that period is a valid benchmark.

An important chart.

China’s economic growth vs shareholder returns over the last 20yrs shows how important net issuance is.

If negative, shareholders benefit. If positive, bad luck.

#SpaceX

FT: "Goldman Sachs analysts are predicting total US equity supply of $1.175t in 2026, consisting of $225b of IPOs, $450b of other corporate stock sales, and another $500b gradually dribbling out from corporate executives and early investors in the IPOs...This has understandably led to fears that the market could suffer severe indigestion. Even one of these big IPOs could be enough to cause a mild case, but the combination could prove painful. That big IPO years tend to presage big downturns has exacerbated those concerns."

As I dissected in my February report on "Price Discovery" (https://t.co/kEx5Z4BJH7), relative market resilience since the GFC has been in part predicated on passive investing reducing equity supply against persistent demand. Less AUM in the hands of active managers means fewer shares traded based on price moves. Meanwhile, passive flows have stayed constantly positive. This has reduced the elasticity of stocks. To quote an Economist recap of one study into this:

"The paper, by Xavier Gabaix of Harvard University and Ralph Koijen of the University of Chicago, sets out their 'inelastic-markets hypothesis.' This contradicts the textbook argument that money flowing into stocks should barely raise prices, since if it did, demand would fall and return prices close to their starting level. In fact, the paper’s authors find that stock market demand is not 'elastic' in this way. It is inelastic, and does not fall much as share prices rise. As a result, an investor who buys $1-worth of stocks using fresh cash (or the proceeds from selling other assets such as bonds) pushes up aggregate market value by $3-8…Most important, funds that maintain fixed allocations can push up prices. Suppose you exchange cash for new units in a fund promising to keep 80% of its assets in shares. The number of shares in existence does not change, but demand for them has risen. The fund can buy shares from another type of investor, but in practice flows between investor groups are low. (This also implies inelasticity, since if demand were elastic, groups with different beliefs, about future earnings, say, would act differently, boosting trading.) The only way to put the cash to work, if all similar funds are to also meet their mandates, is to buy fewer shares at a higher price."

Which, of course, begs the question: what will a flood of new supply mean if demand doesn't spike to meet it. Difficult question to answer given we've not seen an IPO wave of this scale at a time when passive vehicles control this much AUM. I'll be digging in for answers in the days and weeks to come. But as I warned in the report: "The benefits of inelasticity on the upside could do the equal and opposite on the downside."

Learn more about Sage Road Research here: https://t.co/Wgwz2xnvR6. Interested in subscribing? Message me.

FT link: https://t.co/0mb9o48ZWR

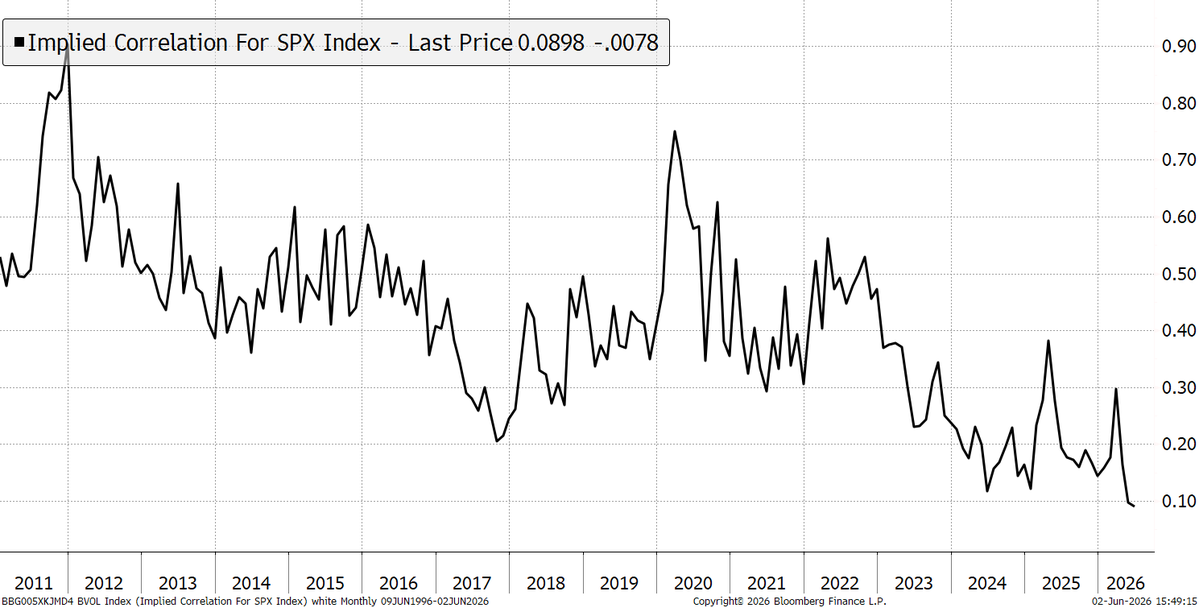

Who can recall the days of RORO. Risk-ON, Risk-OFF when asset prices rose and fell together. Today, we have the exact opposite, as implied correlation falls into single digits.

With the world's largest stocks switching from buybacks to equity issuance, and the world's most famous private companies (SpaceX, OpenAI, Anthropic) all lining up blockbuster IPOs...

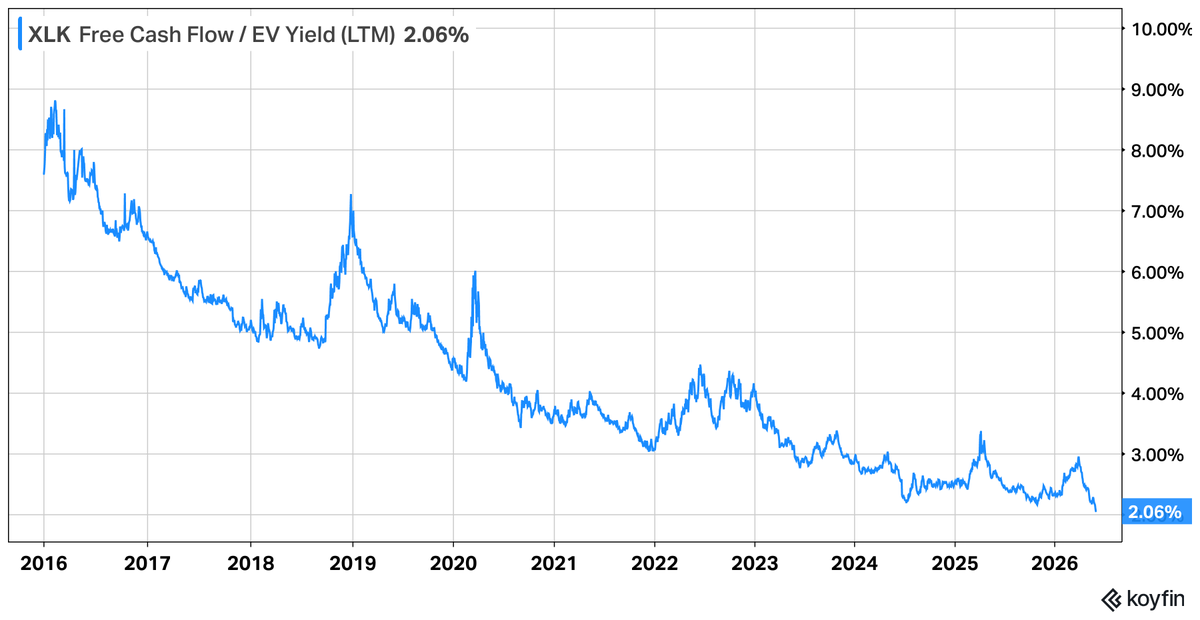

We follow last week's look at the impact on the indices by measuring the growing bubble in semiconductor stocks, and studying where opportunities might be appearing instead: the antibubble.

Clients can see our latest change to the portfolios.

#Bubble #Investing

https://t.co/QPlZzTd9VV

@SteadyCompound Like this a lot. Should apply a very high bar to turnaround situations.

Clear-eyed management and access to capital are non-negotiable.