Giving the digital asset industry the commonsense rules it needs to thrive isn't a Republican issue or a Democrat issue. It's an American competitiveness issue. Pass the Clarity Act.

DTCC LIQUIDITY COINS: PPL will see this,then talk crazy for views cause they’re a bunch of clout bozos. ORACLE has to clean it up.

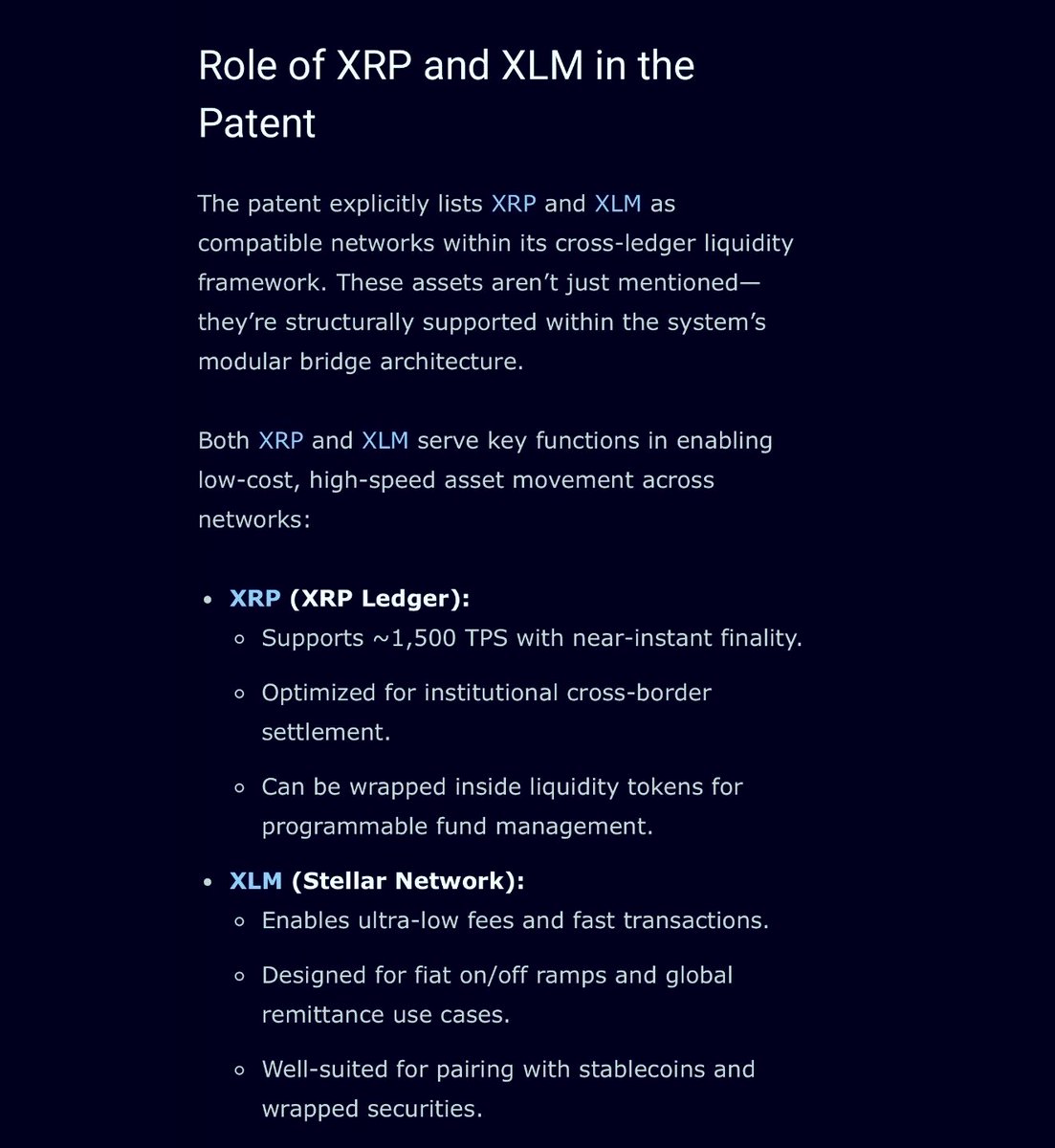

1. $XRP WILL BE INSTITUTIONALIZED CROSS BORDER SETTLEMENT

2. $XLM PAIRING STABLECOINS

YOU NEED BOTH. DIVERSIFY.

$XRP IS LITERALLY IN THE DTCC PATENT WITH XLM FOR MANAGING DIGITAL LIQUIDITY TOKENS IN A DLT PLATFORM.

SO THE RETARDS CAN STOP SAYING ITS OVER FOR XRP WHEN DTCC ALREADY HAD IT IN THE PATENT WITH XLM. THEY ARE BOTH THE ONLY TWO BODY MEMBERS OF THE NEW DLT STANDARD.

If you’re in crypto right now and your portfolio is red and your family thinks you’re crazy and your friends stopped asking about it, congratulations.

You just described the exact starting point of every person who actually made it

@blockchainchick agreed. can't think of anything more bearish than clear rules and regulations that will allow billions, even trillions, of dollars of institutional capital to flow into crypto.

The Senate Banking Committee is putting in the work as it moves the Clarity Act forward… incredible leadership!

Millions of Americans are already in this market. Ripple stands behind this bill because they deserve the same rules and protections as every other asset class. If the largest economy in the world is going to lead on crypto - and it must - this is the moment. Let's get it done!

Today, Mastercard, @OndoFinance, Kinexys by @JPMorgan, and @Ripple successfully completed a landmark transaction connecting a public blockchain with interbank settlement rails.

Together, we’re laying the groundwork for 24/7 global markets that never close.

BREAKING: A bill in California to authorize every state chartered bank and credit union to Custody Bitcoin and digital assets for their customers has passed unanimously out of committee.

LATEST: ⚡ The CLARITY Act’s stablecoin yield draft has reportedly been pushed to at least next week, with the current text still banning rewards on idle balances while allowing yield tied to transactions.

Wells Fargo is working with us as part of a global group of banks to design our blockchain‑based ledger for cross‑border payments.

Together, we are shaping the rails of the future to support interoperability across all forms of value – today and tomorrow.

👉 Learn more: https://t.co/kbxyTTw4Vg

Some years ago, I reviewed a confidential intergovernmental briefing circulated under NDA between several European states. The countries themselves were not named in the extract I saw, and they were not meant to be. What mattered was the operating assumption embedded in the document.

The conclusion was straightforward. End users would never be presented with raw infrastructure. Institutions would continue to front technology and trade solutions under their own names, their own balance sheets, and their own brands. Trust, in Europe especially, would remain institutional.

What sat beneath those branded solutions was the real focus. The document described settlement rails that would be standardized across borders, invisible to the customer, but interoperable at scale. The emphasis was on neutral infrastructure capable of real time value transfer once regulatory and identity frameworks were aligned.

Ripple and the XRP Ledger were referenced in that context. Not as a consumer facing product, but as underlying plumbing. The language was explicit that the winning technologies would never need to be marketed to the public. They would be embedded, abstracted, and eventually taken for granted.

That is how institutions think. They do not sell rails. They sell services. The rail only needs to work.

If this unfolds the way it was described, most people will one day use systems powered by XRP without ever knowing its name. And from an institutional perspective, that is exactly how it was designed to be.