SK HYNIX CEO: NEXT YEAR IS EXPECTED TO BE THE WORST YEAR IN THE INDUSTRY’S HISTORY FROM A SUPPLY PERSPECTIVE — RTRS

SK HYNIX CEO: DESPITE AGGRESSIVE CAPACITY EXPANSION, MEMORY DEMAND WILL CONTINUE TO EXCEED THE COMPANY’S PRODUCTION CAPACITY OVER THE NEXT DECADE — RTRS

'custom HBM' (cHBM) and why advanced AI Memory is no longer cyclical:

"An HBM carrying a customer’s circuitry is that customer’s dedicated part and cannot be sold elsewhere, and from the customer’s side, memory with its own circuitry embedded cannot easily be swapped for another supplier’s product. The commodity premise that anyone’s part is interchangeable as long as the spec matches no longer holds from cHBM onward"

Guys... with the recent LTAs from the Memory Majors, with HBM being customized, with Physical AI and its giant Memory requirements coming..... don't you think $MU $SKHY deserve a re-rating ?? 💪

Memory is the new GPU story, to the best of my assessment, which makes it outright hilarious that we price these names at 7–8x forward P/E. In my view, those multiples need to be 2–3x higher.

Prediction: Nvidia Nemotron's market share will 5-10x from now until end of this year.

Open source AI is having a real moment. Nemotron is best set up to capture it, especially inside large enterprises. It won't show up cleanly on OpenRouter stats or similar leaderboards, because the install will live within on-prem environments.

This is not because Nemotron is the "smartest" model per se. Many other open/close models are "smarter". But it is the most open!

Weights are open. So are pre and post-training data, plus how the model is built. Only other model that is as open is the K2 models from @mbzuai, an academic institution. (See @ArtificialAnlys openness index, an increasingly important chart.)

None of the open source Chinese labs open up beyond just the weights. Many do write great papers to share methodology and innovation. None share the datasets that go into pre/post training.

This data transparency part is becoming increasingly important for large companies, who want to verify the models they deploy are not trained on data that could present security vulnerabilities, then post-train them further with its own data and IP.

Only Nemotron fits the bill. It also has all the hyperscalers plus Palantir as partners to make deploying, post-training, plus continuous improvement on-prem in perpetuity manageable. This is huge undertaking!

Creative structures are needed to get GPUs in the hands of startups + other companies that aren't Meta, OpenAI, Anthropic, SpaceXAI, Microsoft, Amazon, Google

AI Debt Financing will be over $7T of debt outstanding by 2029 driven by needs of neoclouds, DC builders, + hyperscalers

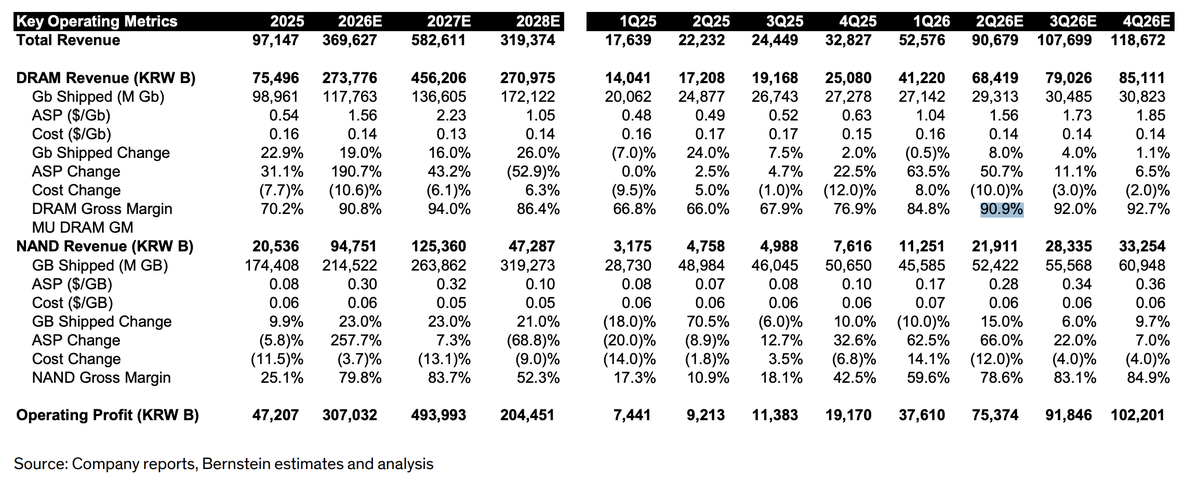

its often a lot easier to impute what the market is assuming instead of forecasting. humans are much better at tasks like this. so, for $MU:

F2027: consensus

F2028: slightly below

F2029-terminal: well below

stock price: current price

returns on cash: meager

SK Hynix confirming the the increasing performance need on data flows. Where data lives, how fast it moves, how often it gets reused. Company strategy focussed on selling the whole memory hierarchy… HBM4 on chip, AI server level DRAM in the system, massive QLC storage underneath. Make sure to READ the SK hynix part attached.

Memory stopped being a component a while ago. It became the architecture. And It will increase more and more as co-design will grow. And the numbers they cite say the same: HB +92% this year, server DRAM +60%, eSSD +130%. the best positioned company long term is not selling a part anymore, it is designing the whole stack.

In the strategy part of the research we also reviewed their whole long term strategy and what important strategy choices they have to make in my eyes.

You can read the full thinking on how we came to this conclusion in the upcoming research. For now check the post in the comments for further understanding.

$MU $000660.KS $005930.KS $SNDK

UBS raises its DRAM and NAND price forecasts

DRAM prices are now expected to rise 32% QoQ in Q3 and 18% QoQ in Q4.

NAND prices are expected to rise 30% QoQ in Q3 and 12% QoQ in Q4.