$EWY closed -14%.

The amount of anxiety global investors are going to have building up all weekend is going to be astronomical. Asian markets are going to puke hard Sunday night, and it will flow through to the US.

$EWY on track for worst day since the margin calls at the start of the Iran War. Except now leverage is higher.

For $SPY I'll be watching for a Monday morning gap down capitulation, but given the amount of leverage in the market and fear that will kick in, I wouldn't rule out a continued slide into Tues either.

$EWY on track for worst day since the margin calls at the start of the Iran War. Except now leverage is higher.

For $SPY I'll be watching for a Monday morning gap down capitulation, but given the amount of leverage in the market and fear that will kick in, I wouldn't rule out a continued slide into Tues either.

This cycle I believed the memory trade had a loose expiration date of summer 2026 due to concerns over the supply coming online 2027-28.

Right on cue we have the classic Chinese supply narrative emerging, concerns over decelerating and possibly contracting pricing 18mo out, and this disconnected idea that locking in supply/demand via LTCs is bullish despite them removing upside optionality.

Incremental rate of change of memory pricing decelerates in 2027, and the probability of funds rotating out at this point is high, even if only to take the significant profits that have been generated the past year.

Memory trades usually end sooner than you think, but this time, there’s an unprecedented amount of embedded leverage from global retail investors.

Certainly feels like we’re at the point where every bear is extinct, leverage is high, and doubters capitulated in, so who will be the incremental buyers to offset funds taking profits on massively outsized memory positions?

Just something to consider, especially as the semis trade sets up for consolidation again.

"BNP Paribas analyst Karl Ackerman expects the average selling prices (ASPs) of DRAM and NAND — which surged on AI demand — to peak in mid-2026, much earlier than his original forecast of mid-2027, before turning into quarter-over-quarter declines starting early next year. He argues that this is driven by aggressive capacity expansion from Chinese memory makers such as CXMT and YMTC, combined with reduced memory consumption from other industries due to soaring prices, including a 14% decline in global smartphone shipments this year. He also noted that growing concerns over future oversupply and margin deterioration within the next one to two years are beginning to weigh on the sector in advance."

I’m trying to remember the name of this analyst.

Two weeks ago the dominant $MSFT narrative was "funds selling because of no AI" (incorrect). Now the headlines are MSFT rallying into the build conf based on efforts in AI... wacky inflatable tube man market is undefeated.

The stock has been totally bombed out and positioning will now play catch up as the market shifts towards the actual underlying story of AI, Azure, and margin gains from Maia 200.

I expect MSFT to continue rallying, but will likely exit the July calls by EOW.

$MSFT is a compelling opportunity and calls remain cheap. Watched it since March, then thought I missed it after Ackman's tweet on May OpEx, but it's still doing a bunch of nothing.

The copilot business is compounding at a triple digit rate , and their distribution channels are some of the best in enterprise AI.

The Maia chip should be helping drive margin expansion from Azure services at the same time growth is accelerating.

On top of that we have reports that Anthropic is in talks to be the first external customer to use Maia 200- really, it's to expand compute access, but the headline will validate the Maia story.

My view has been very similar to Ackman's; here's his thesis: https://t.co/ULWKicbYrd

$MSFT is a compelling opportunity and calls remain cheap. Watched it since March, then thought I missed it after Ackman's tweet on May OpEx, but it's still doing a bunch of nothing.

The copilot business is compounding at a triple digit rate , and their distribution channels are some of the best in enterprise AI.

The Maia chip should be helping drive margin expansion from Azure services at the same time growth is accelerating.

On top of that we have reports that Anthropic is in talks to be the first external customer to use Maia 200- really, it's to expand compute access, but the headline will validate the Maia story.

My view has been very similar to Ackman's; here's his thesis: https://t.co/ULWKicbYrd

As two of the largest forces in equity markets -- growing index ownership and increasing amounts of capital controlled by extremely short-term-oriented, leveraged, volatility-intolerant investors -- converge, we have found occasional opportunities to acquire some of the most dominant long-term compounding franchises at attractive valuations.

For example, we acquired Alphabet $GOOG when the stock declined substantially on the release of ChatGPT in late 2022, Amazon $AMZN in the weeks following Liberation Day, and $META more recently on the market's response to the company's unexpectedly large cap ex guidance and expenditures.

In our 13F which we will file later today, we will disclose a new position in Microsoft, a company we have followed for many years now offered at a highly compelling valuation. While $PSUS will not be filing a 13F tomorrow, it has also recently made $MFST a core holding.

Microsoft operates two of the most valuable franchises in enterprise technology, which account for approximately 70% of the company's overall profits: M365 and Azure.

M365, the company's productivity suite, is the dominant operating platform for knowledge work, with over 450 million workers using Word, Excel, PowerPoint, Outlook, and Teams on a daily basis.

Azure is the world's second-largest hyperscaler cloud platform and, like AWS in our Amazon investment, is a direct beneficiary of the multi-decade migration of enterprise IT workloads to the cloud, which is now further accelerated by surging demand for AI inference workloads.

Both M365 and Azure are underpinned by Microsoft's unparalleled enterprise distribution and the security, compliance, and identity infrastructure it has built and refined over decades.

Beyond these core franchises, Microsoft also owns a portfolio of other leading businesses, including LinkedIn (the world's largest professional network with 1.3 billion members), its gaming platform (Xbox and Activision Blizzard), and search and news advertising (Bing and the Edge browser).

We began building our position in MSFT in February following a meaningful share price decline after the company reported its fiscal Q2 2026 results. We were able to establish our position at a valuation of 21 times forward earnings, broadly in line with the market multiple and well below Microsoft's trading average over the last few years.

Notably, MSFT's headline multiple does not reflect the value of Microsoft's approximately 27% economic interest in OpenAI, which would represent approximately $200 billion, or 7% of Microsoft's market capitalization, at OpenAI's most recent funding round valuation.

We believe Microsoft's recent share price decline has been principally driven by investor concerns around two key issues: i) the competitive positioning of M365 against increasingly capable AI lab offerings (notably Anthropic's Claude Cowork), and ii) the durability of Azure's growth, especially in light of Microsoft's evolving relationship with OpenAI.

In our view, investors underestimate the resilience of the M365 franchise given its deeply embedded role across enterprises and highly attractive price-value proposition. Unlike point software solutions, which may be vulnerable to disintermediation by better-performing AI alternatives, M365 is tightly integrated into the daily workflow of nearly every large enterprise and is supported by Microsoft's identity, security, compliance, and data governance infrastructure, which would be nearly impossible to replicate.

Attractive bundle economics further reinforce Microsoft's advantage, with monthly average revenue per user on the M365 suite at approximately $20, less than half of what customers would pay to purchase the underlying applications individually from different vendors.

Moreover, we are encouraged to see Microsoft prioritizing its R&D efforts and investment in Copilot, its own AI agent embedded across M365, with direct involvement from CEO Satya Nadella. We believe these efforts will translate into improved product velocity and greater customer adoption over time.

Alongside Copilot's rollout, the company has also begun shifting its pricing model from pure per-seat licensing to a hybrid model of seats plus metered consumption, which helps expand the company’s revenue opportunity as AI agents drive incremental usage that a seat-only structure would not capture. These initiatives should help sustain M365’s strong underlying growth momentum, which was already evident in the business unit’s 15% revenue growth (in constant currency) last quarter.

We believe concerns regarding Azure's growth trajectory are similarly misplaced, particularly in light of the franchise's exceptional recent performance. Azure revenue grew 39% in constant currency last quarter, with company guiding to modest acceleration through the second half of the year.

We view Microsoft's recent decision to restructure its OpenAI partnership not as a concession but as part of a deliberate pivot toward a more open, multi-model architecture that better serves enterprise customers, who increasingly seek optionality across model providers.

Microsoft recently disclosed that over 10,000 enterprise customers have used more than one model on Azure Foundry, the company’s modular AI model marketplace. This model-agnostic approach also strengthens Copilot, which can auto-route queries across multiple models to deliver the optimal output for a given task.

To support Azure's rapid growth amid persistent supply constraints, Microsoft has raised its calendar year 2026 capex budget to approximately $190 billion. Consistent with what we have observed at hyperscaler peers Amazon and Google, we view this spend as growth capex that should drive future revenue generation. This is particularly true for Microsoft, given that roughly two-thirds of its capex budget is allocated to server and networking equipment that correlates directly with near-term revenue.

Like our purchases of $GOOG, $AMZN, and $META, we believe that $MSFT offers analogous and compelling long-term value at today's valuation.

$SONY has been setting up and I started accumulating the last week. Call IVs are dirt cheap.

Business/roadmap updates should be coming in the next few weeks (annual cadence) and I expect more on the recent MOU on a 2nd JV with TSMC for CMOS sensors that'll power physical AI. This will be the key to their re-rating, which I suspect is imminent.

SONY pays a meaningful amount of expenses in USD, so a strengthening JPY- which seems likely to materialize in the next few months- will be a tailwind for margins. They also just blasted out of ~1bil (USD) in charge offs into strength as core businesses outperformed. These are non-cash write downs. Ex write offs, the recent report would have been a sizable beat.

SONY trades around ~17x fwd

Hundreds of billions of stock buyback/dividends INCOMING for $NVDA I'm serious.

I just got off a video call interview with Nvidia CFO Colette Kress after the earnings call. (Yes, Substacks get this kind of access now. Sorry, mainstream media.)

When I asked her whether the 50% FCF shareholder return plan after strategic pre-payments/investments is a permanent policy (not just this year), she said yes.

I then followed up by saying with some growth factored in that math points to hundreds of billions in stock buybacks and dividends soon, do you agree with that?

She nodded her head emphatically. "Yes! Yes. Yes. Do the math going forward, when will we meet a trillion dollars returned to shareholders? That's what we're pretty much saying. It's on the horizon.”

Gavin Baker: "I've been optimistic that the fundamental shortage of wafers, which is really controlled by Taiwan Semi, will prevent a bubble."

"If Taiwan Semi did what Jensen wanted, Nvidia could sell $2 trillion of GPUs in 2026 or 2027.

But there is a limit where consumers would consume so much that you'd probably be in an overbuild.

And you are starting to see companies go to Intel and Samsung.

A lot of this may come down to the degree to which Taiwan Semi can maintain a lead over Intel and Samsung and the pace at which they expand capacity.

If I were to watch one thing to understand whether there's a bubble, it's Taiwan Semi's capacity decisions.

There's a Goldilocks zone where they expand enough to make it hard for Intel or Samsung to emerge as a second source, but they also keep the fundamental constraint on wafers that helps us avoid a bubble."

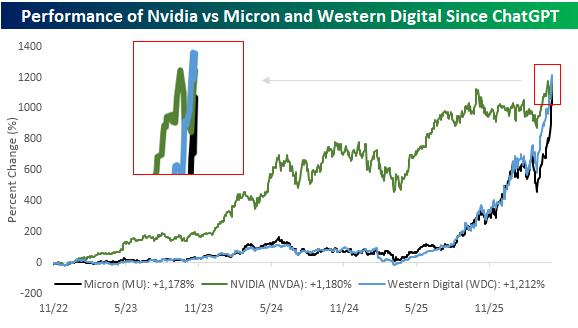

Feels like only yesterday WDC/SNDK was left for dead at ~$15bil mkt cap (pre-spin) as the market refused to accept the structural shortage story outlined by WDC in June '24.

Big blowoff top vibes this week with the daily gap ups and the picture perfect finish of a squeeze into the weekend. Pros deployed into EOQ, which means the semis basket just made their whole year while positioning and valuations are getting stretched. Stay frosty.

Stay frosty for this part. Market tends to "test" new Fed Chairs with -10% drawdowns in their first year on the job, and I would bet if Warsh gets the FOMC to vote in a way that reduces rates but increases BS runoff, there is a non-zero chance the bond market could have a scare due to fear over impact of tighter borrowing.

First 2 meetings would be:

1. June 16-17: My *guess* is this would be status quo unless conditions meaningfully changed)

2. July 28-29: I'd expect a little more of the Warsh policy to surface. Could kick off a challenging period

Honestly, that leaves Sept 15-16 as the third meeting, and if we do get volatility in July-Aug period, by the Sept meeting we should have enough of the inflationary pressures starting to roll over that Sept could be a great month for equities.

Shocking news.

As a non-expert in fin plumbing, I never understood why we didn't 1st accel the BS runoff instead of aggressively hiking. Would've avoided dual impact of money market income driving inflation & reducing supply-increasing investment.

Warsh's views seem similar.

The admin keeps pushing this "hawkish" narrative to soothe bond mkt. It's nonsense.

Literally a 0% chance that Trump, with full control of the nomination, selected a hawk who will pressure credit.

Rate cuts + BS runoff = high spread =/= high rates

https://t.co/tsZdjbqJ2H

I've spent a significant amt of time w/claude vibe coding tools and programs for myself. There's ZERO chance SMB will have time or risk tol to vibe code critical infra. Startups are most at risk vs embedded platforms.

We probably see some mega squeezes on earnings this quarter.

the stock market is funny because the largest global supply chain shock since a deadly worldwide pandemic is worth -0.2% but a single blog post speculating about a new technology can stone cold stunner SaaS companies -50%.

Full disclosure, I got aggressive on the ORCL dip on Mon, trimmed it yday, and cut a lot more today. OpenAI closing on $110bil in new funds is positive, BUT the announced partnership w/AWS to supply 2GW (vs ORCL's stalled 4.5GW) specifically for frontier (i.e. enterprise agents) is a big negative imv, as AWS will now be leading the charge in the most important growth area for LLMs.

Fundamentally changes a good portion of my immediate term bull case, so I sent funds to cash to await better setups and a more constructive market environment (which may begin next week).

Ive been watching $ORCL to pick my spot since Dec, and took it today.

The stock has been disconnected from the reality of its >$500bil and growing RPOs, and given the total sector capitulation of the last few weeks, it’s likely finally flushed.

I expect >50% from here in 2026.

"After watching Anthropic's Enterprise Agents briefing event, we have even greater

conviction that model providers are unlikely to displace software incumbents and

are instead positioning themselves and their agents to be an orchestration layer on

top of existing and incumbent systems" - Deutsche Bank

The year is 2028. $NVDA has been trading in a sub-penny bid-ask spread of 193.598-193.599 since December 2027. It is now trading at lower than market multiple despite a 40% CAGR. Surely this is the year it breaks out.