The current bull run is historic:

The S&P 500 is up +95% since the end of 2022, placing the current bull market within the strongest 10% at this stage of the cycle, in data going back to 1928.

By comparison, the top 25% of historical bull markets gained roughly +50% over the same period.

Meanwhile, the median bull market delivered just ~35% after 3.5 years.

The current bull run has remained within the strongest 10% of historical bull markets for 2 years, excluding the March-April 2025 correction.

Since the April 2025 low alone, the S&P 500 has surged +51%.

Market momentum is incredibly strong.

Gold has struggled big time during midterm summers. July, August, and September were each red months in 2022 and 2018. And $GLD hasn't seen a green July since 2006!

The biggest lesson of the AI era: never get comfortable.

On June 2nd, IBM, $IBM, was up +13% for the year and trading at its highest level on record.

Today, just 42 days later, $IBM fell -25% posting its biggest daily decline since 1968.

The stock is now down -35% in 42 days erasing over -$100 billion in market cap.

AI is rapidly transforming the global economy.

Adapt or be left behind.

The AI race between the US and China is intensifying:

Currently, 20 of the world’s 50 most used AI models come from China, according to Apollo, up 400% since 2025.

Over the same period, the number of US models in the group has fallen to 28 from 33.

Meanwhile, monthly token usage of Chinese models among the top 20 AI models surged +113% MoM, to 98 trillion tokens in June.

By comparison, US model token usage rose +43% MoM, to 53 trillion tokens last month.

As a result, token usage for Chinese models is now 85% higher than for US models, up from 24% in May.

China is challenging the US' lead in AI race.

@FinanceLancelot@andreijikh AI models themselves are becoming more commodity-like, but the products, data, distribution, and ecosystems built around them may still provide significant moats.

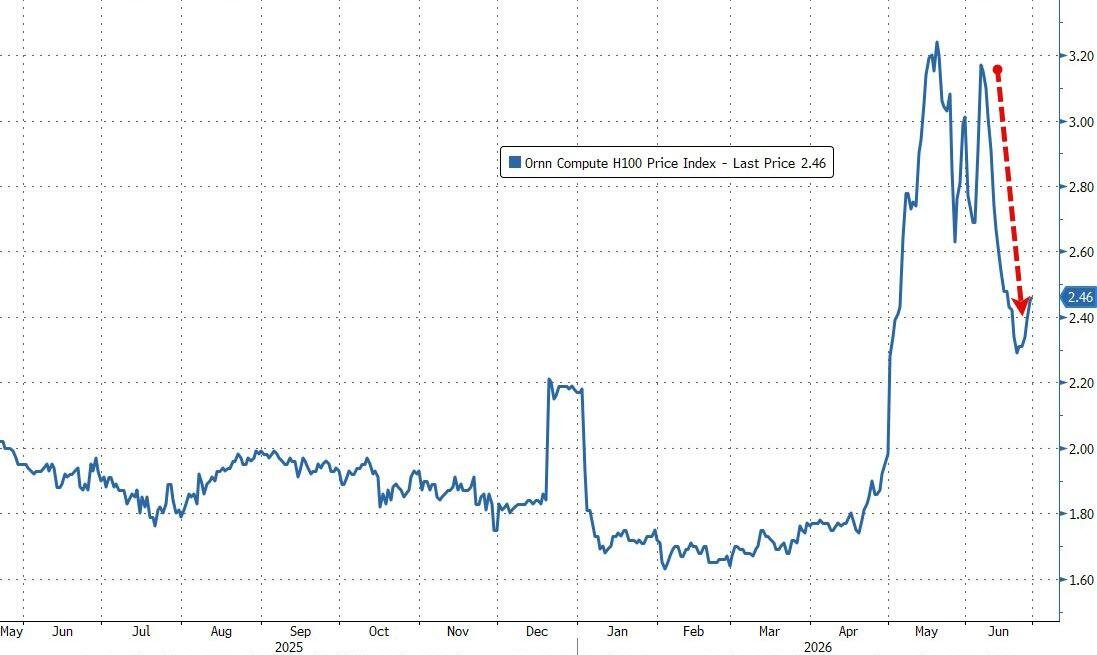

AI compute prices are completely collapsing. This is going to impact AI data center gross margins at the worst possible time.

Keep in mind, even at peak pricing all of these AI providers were extremely unprofitable.

The decline in private credit funding has forced them to switch from heavily subsidized subscription pricing to token based billing.

A desperate move, because corporations are now realizing LLMs are anywhere from 10-20x more expensive than they had been told.

Like subprime loans in 2008, the teaser rate just expired.

The rush for SpaceX, Anthropic and OpenAI to IPO is clearly because they see a double headwind of declining demand + declining gross margins.

Price discovery and return to normal is the hallmark of every bubble.

Did the AI bubble just pop?

BREAKING: OpenAI has proposed giving the Trump Administration a 5% stake in the company to "clear political obstacles," per FT.

Details include:

1. Sam Altman has argued that giving the public a financial stake in the company is the best way to share the upside of AI

2. OpenAI is reportedly in "early talks" for a public ownership deal as political pressure rises

3. The proposed arrangement would involve other US AI companies handing over a similar stake

4. Sam Altman is reportedly in active talks with the Trump Administration about the situation

The Trump Administration may soon have equity in US AI giants.

From the @FT:

“The price of gold fell below $4,000 a troy ounce on Tuesday as it headed for its worst quarterly performance in more than a decade, amid expectations of higher interest rates and dwindling enthusiasm among retail investors.”

(As to what's next, please see my prior post on gold.)

#economy #markets #gold

GOLD SET FOR WORST QUARTER SINCE 2013

Gold is on track for a 13% quarterly loss, its biggest decline in 13 years.

The selloff is driven by expectations of higher U.S. interest rates, with markets pricing in multiple Federal Reserve rate hikes this year.

Analysts say a stronger dollar, easing energy prices and higher-for-longer rates are likely to keep pressure on gold.

AI-related debt issuance is skyrocketing:

US corporate investment-grade gross debt issuance is projected to surge +25% YoY in 2026, to a record $2.25 trillion.

This would mark the 4th consecutive annual increase.

After accounting for maturing debt that is repaid, net new investment-grade debt issuance is projected to jump +57% YoY to a record $1 trillion.

Year-to-date, investment-grade gross issuance has already risen +20% YoY, to $796 billion.

The primary driver behind the surge is AI CapEx, with AI and AI-related debt issuance estimated to increase to at least $400 billion this year, according to Morgan Stanley.

The AI revolution is fueling a historic surge in corporate borrowing.

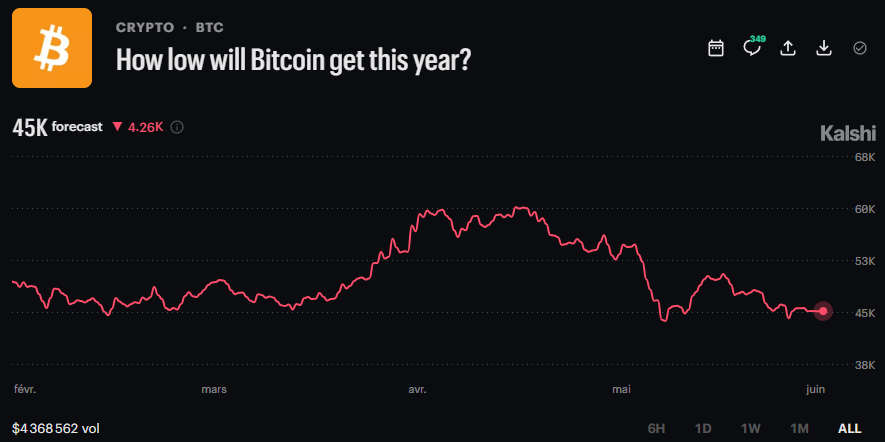

BITCOIN BEARS EYE $45K

Bitcoin remains under pressure as higher U.S. rate expectations weigh on risk assets and the dollar strengthens. Markets are also digesting Strategy's potential $1.25 billion Bitcoin sale and the EU's MiCA licensing deadline.

Meanwhile, Kalshi traders now forecast Bitcoin could fall to $45,000 this year, highlighting growing caution as the cryptocurrency trades near its recent lows.

https://t.co/mQDKbLDDIv

US households are "fighting" inflation with debt:

Total consumer credit surged +$25 billion in March, to a record $5.14 trillion.

This marks the largest monthly increase since March 2025.

Revolving credit, which includes credit cards, jumped +$10 billion, to $1.34 trillion, the highest since November 2024.

This was also the biggest monthly increase since February 2024.

Non-revolving credit, mainly auto and student loans, rose +$15 billion, to a record $3.80 trillion.

As a result, total consumer credit has now surged +$1.05 trillion since the 2020 pandemic.

US consumers' debt levels are skyrocketing.

No sector in history has ever been this large:

The Information Technology sector now accounts for a record 39% of the S&P 500's total market cap.

This percentage has more than doubled since the 2020 pandemic.

This figure is also now above the 2000 Dot-Com Bubble peak of ~33% and the ~31% peak reached by the Energy sector in the 1980s.

Including internet retailers and digital media platforms such as Amazon, $AMZN, and Netflix, $NFLX, tech now accounts for a record 50% of the S&P 500's market value.

By comparison, this same group accounted for just 29% of the index at the Dot-Com Bubble peak.

Tech is all that matters.

Retail investors appear to be rotating out of gold and Bitcoin into semiconductor stocks:

Since April, US gold and Bitcoin ETFs have posted -$12 billion in cumulative outflows.

Over the same period, US semiconductor ETFs have attracted +$20 billion in cumulative inflows.

This trend accelerated in mid-May, with outflows from gold and Bitcoin funds more than tripling.

At the same time, inflows into semiconductor ETFs have doubled.

Meanwhile, the largest US gold-backed ETF, $GLD, is down -13% since the start of April, while the largest Bitcoin ETF, $IBIT, is down -12%.

Over the same period, the semiconductor ETFs, $SOXX and $SMH, are up +81% and +60%, respectively.

Retail is driving markets like never before.