Honest opinions on difference between working buyside vs sellside in finance, from personal experience having worked in both

1/ Both are sales jobs. The sellside mandate is very clear. You have clients who you provide a service for, whether that is M&A advice or capital raising. On the buyside, the job description says investing, which is true, but just as much of it is sales. As a junior hedge fund analyst, you are selling your ideas to PMs and ICs. As you get more senior at a PE firm, your job shifts towards raising capital, having conversations with LPs and convincing companies to sell their business to you. The top people in finance are all incredible salespeople.

2/ The quality of work matters much more on the buyside. A lot of sellside banking work is focused on quantity and volume of materials. Hundreds of useless pages in pitch decks and CIMs, weekly materials that your client never opens, and ideas that will never happen. Buyside work is much heavier on quality vs just volume. The projection models are more thoughtful. The IC memos are better thought out with realistic scenarios, and not just banking CIMs where every chart goes to the right without any explanation. The analysis you put together has to consider a lot of factors, including macro conditions, industry tailwinds, etc. Analysis in banking is boiler plate with clear templates for everything. Hedge fund and PE analysis can be a lot more situation-specific, which requires you to dive into the business and actually understand it

3/ Sellside teaches you numbers, buyside teaches you business models. During my banking years, I learned to get very comfortable with accounting. Putting together analysis quickly, figuring out drivers for a model, and being able to articulate the takeaway cleanly are your core banking analyst lessons. The main thing missing is focus on business and revenue models. On the buyside, this shifts. Numbers and accounting are boiler plate skills because the markets are already efficient and know how to do it. The core skill is more about deciphering the business model, competitive moat, and products. The numbers are still important, but I would argue that almost all of the alpha in the market today comes from qualitative analysis of companies

We’ve automated every single thing we can @every with AI agents.

And yet there’s way more human work to do than ever. We’ve gone from 4 -> 30 human employees since GPT-3.

I wrote a report on the structural reasons: how AI makes expert competence cheap, why that drives up demand for experts, and why the dynamic only intensifies as we approach AGI.

After Automation: https://t.co/Lb7SUCduAg

The incredible daily routine of Paul Tudor Jones:

2:30 AM Wake up, work for 30 minutes

3:00–3:45 Watch the London open, analytical work

3:45 Back to sleep

6:15 Wake up, repeat

6:15 Wake up

6:15–7:00 Work

7:00–7:45 Workout, 45 minutes of hard cardio

8:00 At the screens for the market open

8:00–10:00 AM Screens, no meetings

10:00–12:00 Meetings

12:00 Lunch

1:00 Meeting

3:00–4:00 Hour before the close: map out the next day

4:00 Market close

4:00–5:00 Hour after the close: think about Tokyo and Hong Kong, map out tomorrow

5:00–6:00 PM Walk with wife

6:00–7:00 PM Work

7:00 Eat and watch the news

8:00–9:30 Netflix / mindless entertainment

9:30–10:15 Work

10:15 Bed

2:30 Wake up, repeat

He's had the same routine for over 40 years.

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy:

"We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%.

If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years.

Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.

In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country.

And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008.

The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows.

So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now.

Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."

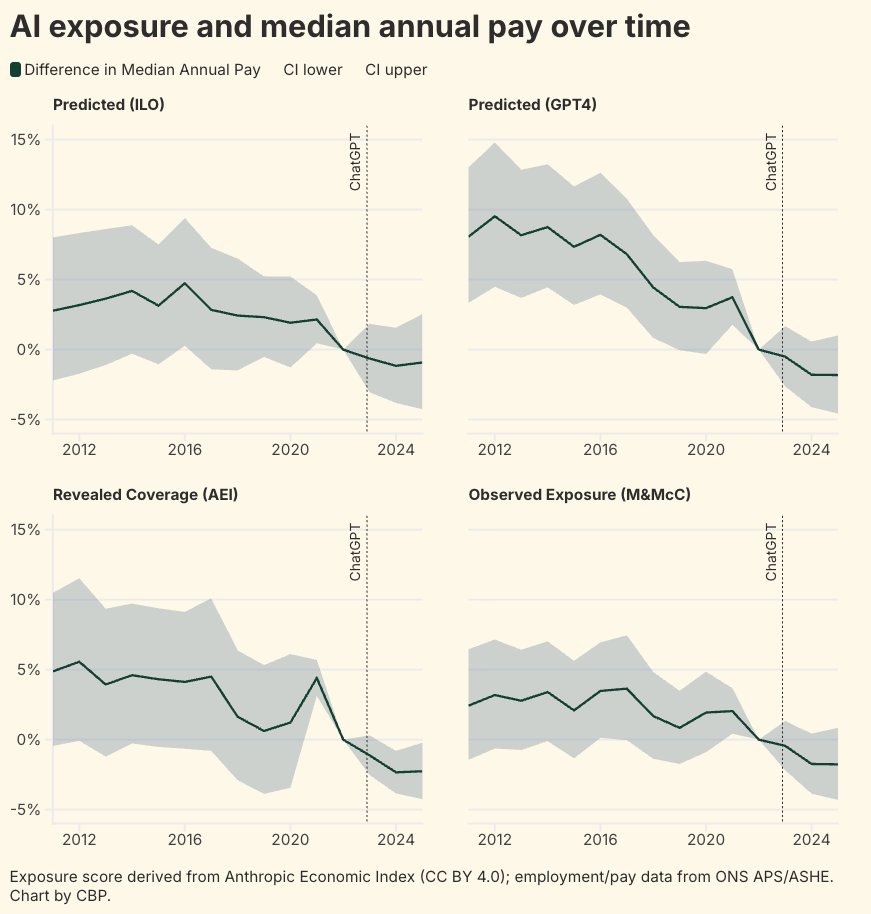

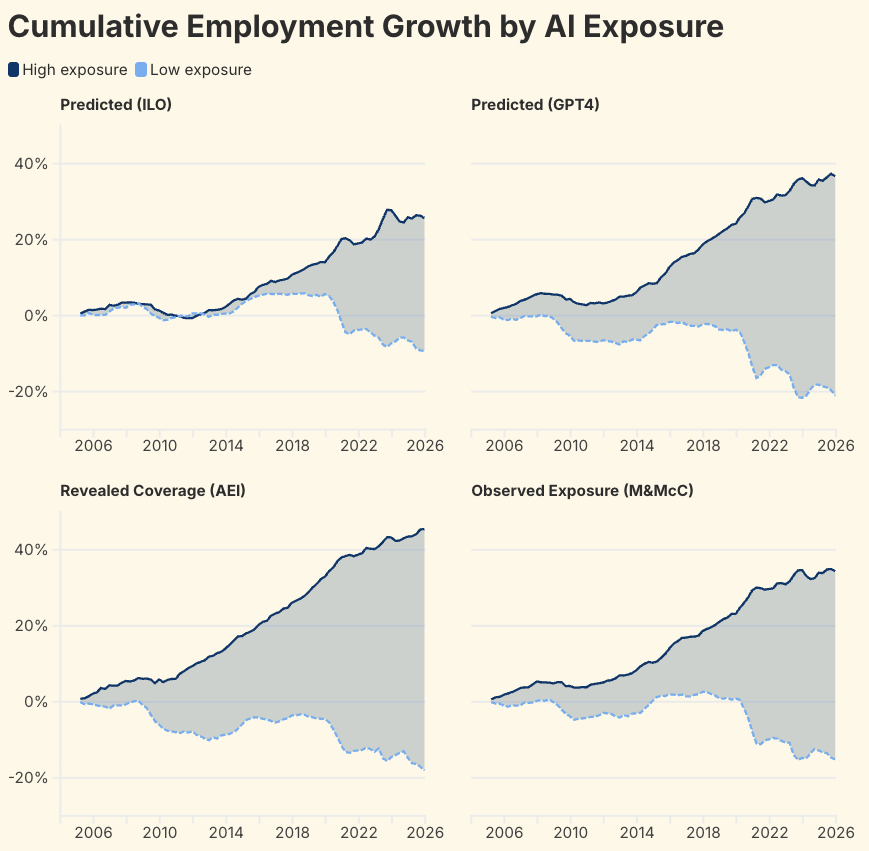

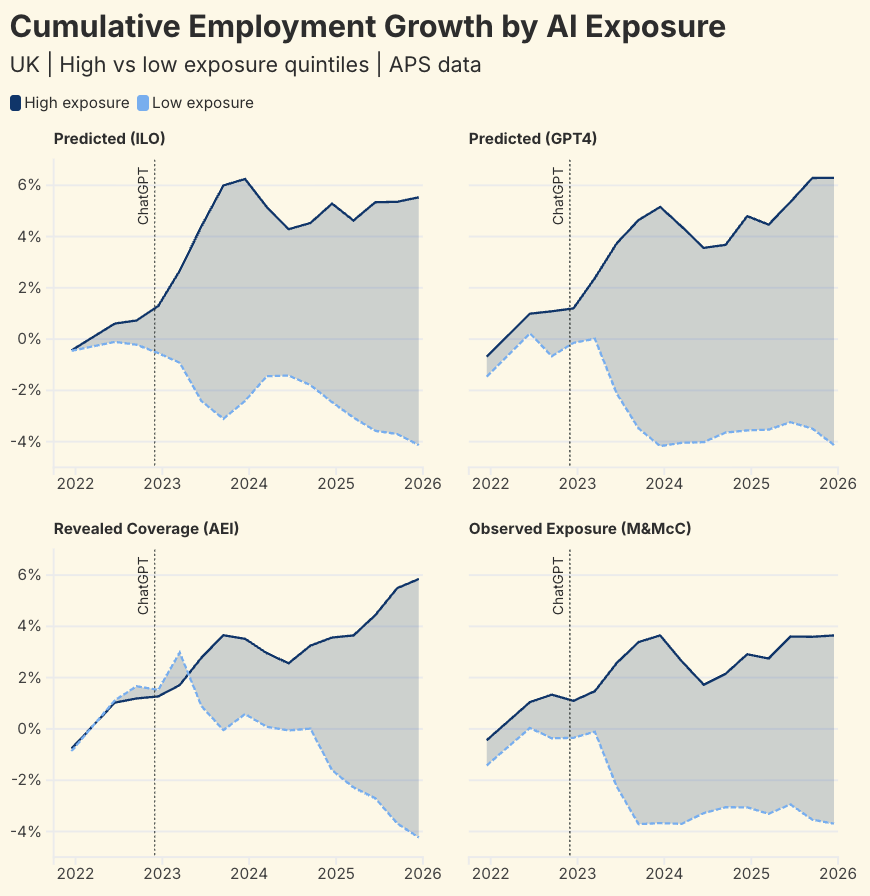

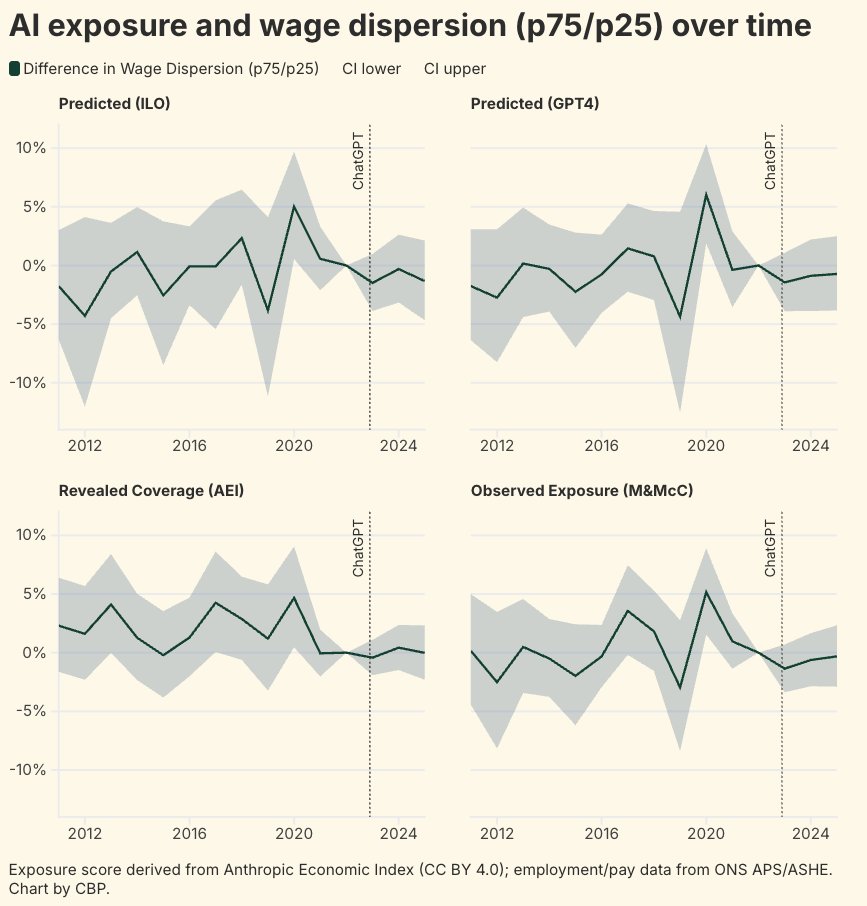

Is AI killing jobs?

New data shows that, more than three years after the release of ChatGPT, there is no evidence for a significant impact of AI on overall employment in the UK.

In our new report, we break down the labour force into different occupations and use four measures of AI exposure to determine how likely they are to be affected by the technology.

Surprisingly, occupations with higher exposure to AI have grown faster than least-exposed ones, not slower. This holds across all four measures, and across two different data sources.

The wage picture is different. Pay in AI-exposed occupations has lagged the rest of the labour market since 2019.

But that gap opened three years before ChatGPT, which makes AI an unlikely candidate for the observed wage compression.

This flattening of the wage structure is visible across the within-occupation distribution and strongest at the top quartile, which is consistent with labour market dynamics that predate generative AI.

True greatness in history isn’t always measured by how hard you beat your enemy on the battlefield - it's more about your values and how you treat those who are vulnerable.

His army was beaten.

His men were demoralized.

Then the enemy general's dog was found on the battlefield.

What Washington did next showed why he was exceptional:

🧵1/5

AI won't kill fundamental investing because more information doesn't kill alpha. We have decades of priors here (Excel, Bloomberg, alt data...all democratized analysis & information gathering, and didn't kill alpha). As measured by factor volatility, stocks are less efficient and more alpha-rich than ever (and empirically, the ability of multi-eight figure market neutral multi-managers to consistently grind out 10-15% returns in an idio-maximized way proves this point...15 years ago a $10bn hedge fund was considered to be impossibly large).

Innovations in investment process have shifted alpha pools, for sure, and systematic investors have arbitraged many old, reliable fundamental alpha pools. But as the players at the poker table have shifted, the constraints of those new players have created new alpha pools. Long duration fundamental investing has been gutted, and definitionally competing against a group of non-fundamental (quants, factor/thematic investors, indexers) and duration-constrained (multi's) investors should be a huge competitive advantage, long term (however frustrating in the near term). To wit, a 9-month thesis where I "look through" the next two prints is now considered a long-term thesis.

Rigorous investment process serves investment judgment, but the real alpha generation fits a power-law distribution and there is some ineffable "nose for money" that the great investors have, that cannot be trained necessarily. Investing is a very hard game, that cannot be distilled to a reinforcement learning sandbox (by the time it is, the regime will have shifted and new drivers move stocks). AI has no sense of materiality, no true discernment, and the lack of context of N of 1 situations (if you haven't noticed, we are living in an N of 1 world!). There is a irreducible element of humanness that is critical to success in fundamental investing, and that won't change.

What does this all mean? In my opinion, there is no better time to be starting a careers as an investor. My first year on the desk, I spent a lot of time doing grunt work: updating Nielsen files, updating models for my PM, creating same store sales master files, building question lists for CEO meetings, etc. This is grunt work. I can automate this all now, and get more quickly to the deep, value added parts of learning the investment process.

Will AI drive alpha? This is a debate people are having, which I find sort of silly. When used correctly, by the right investor, of course it will. Ask any great investor if they had another 4 hours of research time per day whether the quality of their research would improve? That's kind of a dumb question...of course it will. Compressing the mechanical part of your job to focus more on the artisanal part of the job is Step 1, and with agentic systems accelerating fast is now in the strike zone of possibility. This is before we start to layer in a broader monitoring net and use cases to go deeper and build more rigor, finding signals in unstructured data that were missed before, as well as turning your investment genius into a co-pilot pattern recognition system.

The future is very bright for fundamental investing, in my opinion.

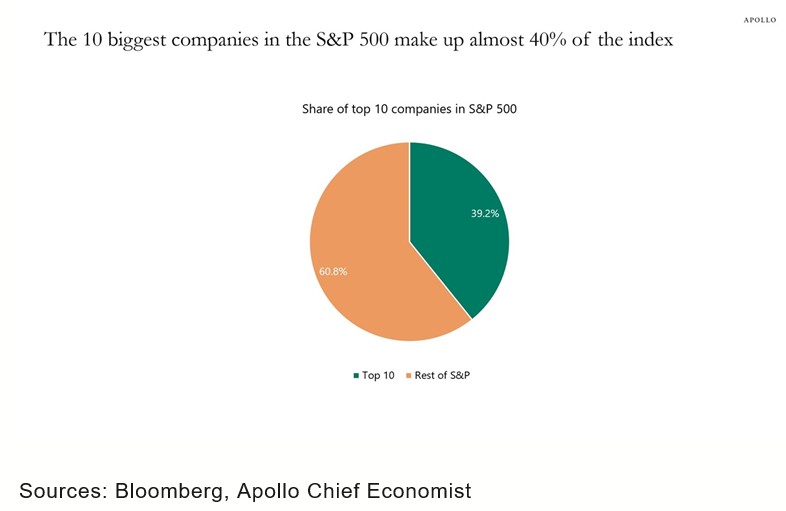

Apollo's Torsten Slok:

"The 10 biggest companies in the S&P 500 make up almost 40% of the index, and if Anthropic, OpenAI and SpaceX are added later this year, the concentration could approach 50%, see chart below. The bottom line is that the S&P 500 basically doesn’t offer much diversification anymore."

#economy #markets #investors #investing

Researchers trained a humanoid robot to play tennis using only 5 hours of motion capture data

The robot can now sustain multi-shot rallies with human players, hitting balls traveling >15 m/s with a ~90% success rate

AlphaGo for every sport is coming

Ten years ago, AlphaGo’s legendary match in Seoul heralded the start of the modern era in AI. Its famous ‘Move 37’ signaled to us that AI techniques were ready to tackle real-world problems in areas like science - and ideas inspired by these methods are critical to building AGI

Today I was asked: what’s the best golf course in New England?

As you guys know, I don’t like talking “best.” But I’ll give you my favorite:

The Myopia Hunt Club, a half-hour north of Boston, is an ancient charmer by Herbert Leeds that hosted 4 early U.S. Opens in much the same form as it exists today.

There are so many great clubs and courses in New England - Eastward Ho, Ekwanok, Essex County, Kittansett, Brookline, Newport, Old Sandwich, Boston Golf, Yale, Fairfield and many more brilliant gems come to mind - but if I had one round to play anywhere I want on a crisp September day, I’m making my way to Myopia.

GPT-5.4 just solved a 20 year math problem, and now the mathematician is "working on a completely new level"

AI is not here to replace us, but to accelerate us 🚀

https://t.co/MXkKzxRJ5d

It finally happened-my personal move 37 or more. I am deeply impressed. The solution is very nice, clean, and feels almost human. While testing new models in the last few weeks, I felt this coming, but it's an eerie feeling to see an algorithm solve a task one has curated for about 20 years. But at least I have gained a tool that understands my idea on par with the top experts in the field. And I am now working on a completely new level. My singularity has just happened… and there is life on the other side, off to infinity!

Fun to do this with my friend @tseides

Minimal discussion of AI; much more of a focus on investing.

Background, philosophy, process, etc.

https://t.co/f8X30Hd4RY

So good by @GavinSBaker

In Michael Jordan’s second to last year with the Chicago Bulls, Jerry Krause, GM of the Bulls said, “Listen players don’t win championships, organizations do. It isn’t just Jordan or Pippen. It’s how we scout, draft, train, it’s our system." Well… after Michael Jordan left they never won another championship.

The thing allocators struggle with is it feels safe and good to say there is a process and its repeatable. Yes, it is important to have a process that is repeatable that works for you, but any process that is repeatable that generates significant alpha will be quickly arbed away in a competitive world.

So where does repeatable outperformance come from? I would submit that any investment organization no matter how big, there are somewhere between 2-10 people where if you took those people out, and that organization would have the exact same process, the results would be dramatically different.

https://t.co/YEfcvZQmKN

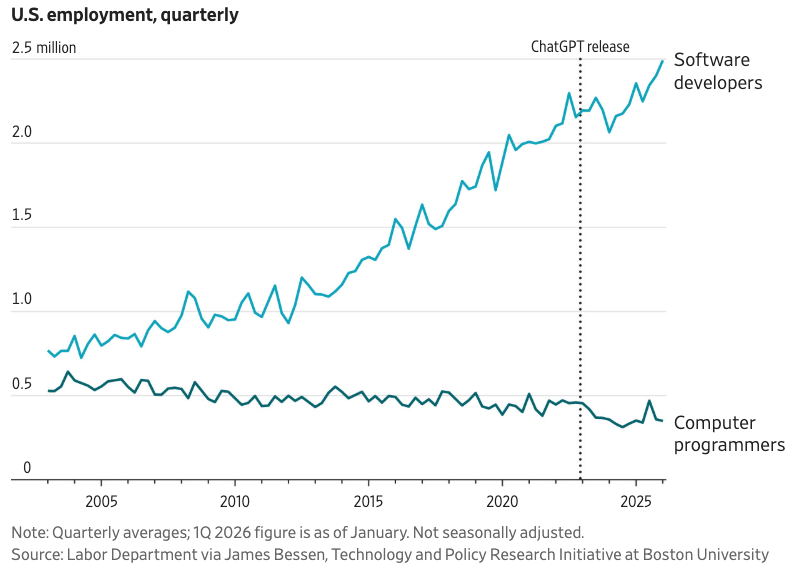

This column counters doomers who say AI could raise unemployment broadly. First, rarely has any technology directly destroyed more jobs than it creates, and I don't see it now. This chart (H/T @JamesBessen) surprised me: software employment still rising /1 https://t.co/mMN9VaPDJP