Réagir à chaud sur 2CRSi serait précipité

Avant de me prononcer, j'attends trois choses :

>la communication du CEO à 15h00

>la reprise de cotation

>une éventuelle réaction de l'AMF

Le rapport est solide et redoutablement bien timé comme d'habitude avec ces fonds short seller

La fenêtre pour répondre est très serrée, le CEO s'exprime à 15h00 à Vivatech

Si j'étais lui je n'irai pas hormis si j'avais déjà bossé ma réponse auparavant

$JBL (Bloomberg) -- Jabil boosted its core earnings per share guidance for the full year; the guidance beat the average analyst estimate.

YEAR FORECAST

Sees core EPS $12.70, saw $12.25, estimate $12.38 (Bloomberg Consensus)

Sees net revenue $35 billion, saw $34 billion, estimate $34.24 billion

FOURTH QUARTER FORECAST

Sees core EPS $3.80 to $4.20, estimate $3.72

Sees net revenue $9.2 billion to $10.0 billion, estimate $8.96 billion

Sees core operating profit $589 million to $649 million, estimate $565.7 million

THIRD QUARTER RESULTS

Core EPS $3.16, estimate $3.10

Net revenue $8.75 billion, estimate $8.64 billion

Core operating profit $504 million, estimate $489.7 million

COMMENTARY AND CONTEXT

Sees 4q26 Net Revenue $9.2 Billion to $10.0 Billion

AI infrastructure demand remains extremely strong, and full-year AI-related revenue outlook is now meaningfully higher

Continued to see better-than-expected performance in areas of the portfolio that had previously been under pressure, particularly in Automotive and Connected Living

Another major tailwind for ex-China rare earths stocks, and some nice spikes in the pre-market for $MP $USAR $CRML etc.

#MKA lists its upstream subsidiary, $MKAR, on NASDAQ shortly (I believe it'll be before end July) at a valuation of 77.5p per share equivalent. At 43.5p, Mkango is currently trading at a 44% discount to that listing price.

Even following a +78% move required to bring MKA in line with the MKAR listing price, MKA's magnet recycling / remanufacturing business will still be valued at zero.

Very shortly, I believe we will be hearing from HyProMag USA about securing financing for its first plant in Texas, commencement of construction, and possibly details on a proposed NASDAQ listing (vis SPAC merger).

That second NASDAQ listing could add a further >77.5p per share as as a liquid asset to MKA's balance sheet.

The age of AI, robotics and the budding space industry will drive a monumental step change in demand for NdFeB magnets - regardless of geopolitical developments (which, to reiterate, are presently adding significant further tailwinds for ex-China NdFeB suppliers).

Low-cost recycling / remanufacturing of these magnets on a global scale will be a requisite for fueling those aforementioned hyper-growth industries.

Step forward, HyProMag.

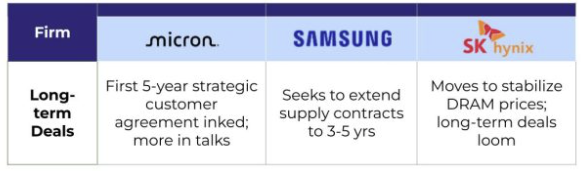

🚨 $MU $DRAM $SNDK Important Reminder

Huge inflection point for the memory industry.

Micron signed its first ever 5 year Strategic Customer Agreement. Not one year. Five. Samsung and SK Hynix are following suit, pursuing 3 to 5 year contracts with major tech firms.

For decades, memory has been defined by cycles. That is ending.

Multi year commitments bring predictable revenue, operational stability, and structural dampening of the boom bust cycles that have kept PE multiples compressed for 30 years.

One year deals gave Wall Street an excuse to call memory cyclical. Five year deals remove that excuse.

As revenue visibility extends, PEG ratios move toward 1.0 and PE expansion follows. The market has not priced this in yet.

The real breakout has not even happened.

OIL SLUMP COULD FUEL STOCK RALLY

JPMorgan’s Karen Ward says falling oil prices could become a “huge tailwind” for equities. A potential U.S.-Iran deal may boost global supply, push oil toward $70, ease inflation, and support rate cuts. She expects renewed market rotation, with Europe among the most attractive regions as investors remain overly pessimistic.

The AI bottleneck rotated one layer closer to the GPU over the past month.

aibottlenecks book: +9.70%

S&P 500: +0.31%

Alpha: +9.39pp

12 of 15 baskets green

Memory Supercycle +32.7%

Custom Silicon +24.0%

Networking/Retimers +25.2%

Power & Grid, Cooling, and Construction & MEP all lagged or went red.

The market is paying for compute density right now it seems, whatever sits on or immediately next to the accelerator.

Proof inside a single basket:

- Samsung Electro-Mechanics (009150.KS) +97.9% (package substrates + high-end MLCCs for AI servers)

- Photronics ($PLAB) –38.9% (photomasks)

Same HBM/Packaging thesis, in the same timeframe, but with a 137pp spread.

One name captures the immediate substrate and component surge from the AI server ramp. The other got hit by design release delays, precisely because memory is tight and fabs are maxed out. The constraint itself created the short term friction for the photomask layer.

This is what layer specific selection alpha looks like.

The outer layers (power queues, liquid cooling retrofits, data center MEP) have longer clocks and different frictions: grid interconnection lead times measured in years, labor and permitting bottlenecks, thermal density walls that air cooling can’t solve.

They will become binding, they just aren’t the marginal bid this month.

Right now the tape is rewarding the parts of the stack that can actually deliver more tokens per watt and more accelerators per rack in 2026/2027.

Breadth was solid (71 names up), and drawdown contained. The gap between layers always closess, it just doesn’t close on a 1 month horizon.

🇺🇸🇨🇭🇫🇷 The party is over, and now it's time to get down to business. Trump landed in Geneva a short time ago for this week's G7 summit.

Trump took off shortly after last night's UFC Freedom 250 event. Now he heads to Évian-les-Bains, France, where the event will be hosted at an Alpine retreat.

Today, he is expected to meet with French President Macron before addressing major issues later in the week, including the Iran-Israel conflict, the Russia-Ukraine war, and other matters.

Writer: Jamie

Why demand is growing so fast:

More compute + more data → better AI.

Better AI → more usage.

More usage → more data and compute demand.

Repeat.

AI is the first technology that creates demand for itself.

Just as a recap, these were all my core European longs:

1. $SIVE

2. $LPK

3. $SOI

4. $RPI

5. $IQE

6. $ALRIB

7. $XFAB

Sivers: As you know by now, core laser chokepoint over next generation photonics, from 1.6T pluggables to CPO.

Embedded in many hyperscaler suppliers from Jabil to Ayar. Should go brrr 2027 but markets are forward looking, so ramps + qualifications should get priced in now.

LPK Laser - Glass core substrate "monopoly" with LIDE.

"More than 80% of major global players have selected our equipment for process validation, learning and scaling to mass production"

Soitec - Silicon photonics SoI substrate pure monopoly while coming out of legacy drag segments.

Raspberry Pi - Was my fun idea around Raspberry Pis being used for AI hardware deployments.

Previously this thing was mainly educational or hobby boards, but now used for edge/local AI. Just thought revenue increase would be extremely material and it played out well.

IQE - Critical epiwafer player for your Western photonics like Macom, Tower, Lumentum, and others.

Was kinda going under, but thought their latent capacity relative to Landmark was undervalued.

Also given how important it was, I thought that your downstream players + Govs wouldn't let it go under, so it was more of a moonshot idea earlier in the year.

Lot more derisked now, very important.

Riber - Kinda monopoly in the MBE space, exposure to Quantum / quantum dot + silicon photonics.

Found out from OSINT help from a friend latentvalue that Microsoft Quantum was buying their machines, so this was direct hyperscaler validation + kinda de-risked at current MCs.

XFab - SiC foundry backed by EU/US CHIPS Act with power semi upside. (152% Y/Y growth for their sic vertical).

Main growth was their silicon photonics foundry past 2027 that's getting evaled by nvidia. And that they're leading Europe's value chain efforts in photonics, kinda like an early tower semi.

We'll see how this plays out, thought power semi exposure + low P/B would derisk the company until they scale their photbunchonics efforts.

From my own personal thoughts:

Out of the maybe $SOI has already been re-rated the most? But I'm holding anyway.

$LPK and $ALRIB I think are still undervalued despite their monopolies.

$RPI is just kinda seeing how things go at this point, would be hilarious if they ended up like a mini nvidia for low end edge ai.

$IQE probably has a long way to go given new tower long term agreement, alongside macom. And if they convert latent capacity, I still think it has a chance of rerating like landmark.

$XFAB idk if im missing something or are markets missing something. you have nvidia as a direct eval of their silicon photonics foundry, and it's trading below replacement P/B. i think im right though.

$SIVE I see has the highest upside out of all of them given laser company ability to vertically integrate, acquire companies downstream to make their lasers more valuable, etc. Just like coherent/lumentum.

There's like 1-2 more random ones that aren't really material, but just in general.

These are the ones I've liked the most.

$IQE x $TSEM just announced a multi-year InP epiwafer supply agreement.

IQE is the non-Chinese InP epiwafer source Tower needed. That’s a geopolitical moat that is ever so crucial in this political complex tape.

200Gb/s pluggables today. 400Gb/lane modulators + optical circuit switches next. IQE is being designed into the full optical roadmap for AI data centers.

Shat makes this so interesting – IQE sued Tower in 2022 for IP theft. Today Tower grants IQE a royalty-free porous silicon patent license as part of the deal.

Former adversary becomes anchor customer, if you can’t beat them? Join them. That only happens when your product is irreplaceable.

$LITE $MTSI were already IQE optical anchors. Add $TSEM and now you have three Tier-1 foundry relationships in the AI photonics stack.

When the market hands us lemons, we make lemonade. I position myself after the drop at 45 and 32. Now I can rip the benefits.

I’m long $IQE

Best FinX communities

- Finnish Tungsten Mafia

Absolute vibemaxxers. Stage 4 Asthma from chronic metal investing. Probably investing directly from their job at the coal mine. If you were ever in danger, 100 naked drunk men will turn up to your house to defend your honour. Brothers for life.

- Korean Leverage Degens

Severe mental illness. Their entire index moves like a 40k market cap shitcoin. Their only 2 options are Bill Hwang or homelessness. No fear of failure, as you can always max another credit card out. Beautiful people with a deep love for winner hard and losing even harder.

- Frenchies Cult of Paris

Their discord is the closest thing to a hedge fund. There is like 400 french adderal + coke addicts doing dd simultaneously on 10000 different stocks at all times. Won't invest in anything that doesn't have a scent of Jean Paul Gaultier on it.

- Crypto Asylum Seekers

Watching them navigate a playing field where they can't rug you to zero is amazing to watch. 24-7 meme fest to cope with how downbad they've been for the last 6 months. No idea how to invest in an equity that actual has value, so they use Fibonacci TA on NVDA and Broadcom.

Je posterai désormais les résumés de chacun de nos lives

Ces derniers sont traité par un LLM et peuvent avoir des "Coquilles".

J'ai la chance d'être entouré d'intervenants d'une qualité rare, et de pouvoir restituer à la communauté l'ensemble des "recherches" que nous menons ensemble sur notre communauté

Merci pour la force que vous nous donnez. Je suis profondément touché par les messages que je reçois autour de ces exercices loin d'être simples car souvent préparé hativement

Dernièrement, ces derniers temps, je suis particulièrement fier des investisseurs qui ont su garder le cap sur leurs propres convictions malgrès les remous et le bruit

Onward

Nous sortons d’une séquence haussière d’une ampleur rare, née d’une rupture : l’IA

D’abord les LLM, la couche logicielle qui a été le récit.

Puis la rotation vers le hardware, le buildout, la plomberie physique de la révolution. Les méga-caps, Nvidia, Google, Amazon, sont devenues trop lourdes pour offrir de l’asymétrie dans ce toujours plus.

Le marché est allé chercher les beta, puis les goulots d’étranglement.

Et là, une mécanique de marché s’est enclenchée.

Float réduit, MCAP modeste, les fonds ne peuvent pas se positionner sans faire bouger le prix. Le retail, lui, le peut.

Résultat une verticalité brutale, alimentée par sa propre réflexivité.

Sur le fond, la thèse tient. La microélectronique est peut-être la condensation de travail humain la plus dense de l’histoire.

Jamais autant d’heures accumulées des décennies de lithographie, des milliers de doctorats, une chaîne d’approvisionnement étalée sur trois continents n’avaient été comprimées dans quelques centimètres carrés de silicium.

Et jamais autant de la production textuelle de l’humanité n’avait été comprimée dans un seul objet logiciel que dans un LLM.

C’est ce qui rend le domaine illisible pour la plupart. il est trop technique pour le narratif, il est trop technique pour les retail, et le narratif arrive toujours avant la compréhension.

D’où la loi d’Amara, « nous surestimons une technologie à court terme, et la sous-estimons à long terme »

À court terme, on price le récit, l’euphorie et récemment on l’a pricé très vie.

À long terme, on price la diffusion, la valeur réelle.

Entre les deux s’installe le grand écart où vivent, successivement, l’euphorie, la déception, les boites qui réussirons, celles qui ont été mise en avant pour les mauvaises raisons.

Beaucoup ont pris le trade en route. En marche, ils ont bricolé une thèse ou pire, emprunté celle d’un autre. C’est là que tout sonne faux.

Une conviction n’est pas une opinion que l’on adopte, c’est une structure que l’on bâtit. Et seule celle que vous avez bâtie vous-même survit à un drawdown de 40 %.

On ne tient pas une position sur la conviction d’un autre.

Au premier trou d’air, la thèse empruntée s’évapore, parce qu’elle n’a jamais été vôtre.

Construisez vos horizons.

Étayez vos thèses. Développez VOS convictions, non par orgueil, mais parce que c’est la seule chose qui tient quand le prix, lui, ne tient plus.

Mais n’oubliez jamais non plus que personne ne part du même point de départ, avec les mêmes avantages ou les mêmes contraintes.

Comparer votre parcours à celui des autres n’a donc que peu de sens.

Le plus important, c’est de construire votre propre histoire.

La France est un pays de frondeurs, d’ingénieurs, de chercheurs et d’industriels capables de se réinventer quand l’ambition est claire.

Sur les semi-conducteurs et le quantique, il n’est pas trop tard. Mais il faut éviter l’erreur classique de vouloir tout faire, partout, avec trop peu de moyens

La France doit choisir les maillons où elle peut devenir indispensable.

Quelques points qui pourraient être intéressants :

1. Une fiscalité beaucoup plus attractive pour les pépites industrielles

Crédit d’impôt, amortissements accélérés, incitations au réinvestissement en R&D, stock-options plus compétitives, PEA encore plus avantageux pour orienter l’épargne vers nos champions technologiques.

Bonus : Un fond de retraite souverain avec avec un panier axé sur nos pépites (Spoiler : infaisable).

Il faut permettre aux jeunes entreprises hardware de grandir en France, de lever en France, de produire en France, sans être contraintes de partir chercher ailleurs le capital patient dont elles ont besoin.

2. Des parcours qualifiants beaucoup plus rapides

Les semi-conducteurs, ce ne sont pas seulement des ingénieurs. Ce sont aussi des techniciens de salle blanche, opérateurs, spécialistes packaging, test, métrologie, maintenance, process, qualité.

Il faut des formations courtes, exigeantes, professionnalisantes, directement connectées aux fabs, aux laboratoires, aux sous-traitants et aux équipementiers.

Pas dans cinq ans, il nous le faut au plus vite.

3. Des investissements massifs sur des niches critiques

>La Corée est devenue incontournable en mémoire avec Samsung et SK Hynix qui ont récemment poussé l'indice coréen très haut.

>Taïwan en fonderie avec TSMC.

>Les Pays-Bas en lithographie avec ASML.

La France doit choisir ses propres goulots d’étranglement : matériaux, électronique de puissance, photonique, packaging avancé, équipements, logiciels EDA, contrôle qualité, supply chain critique.

Et ces entreprises existent déjà. 2CRSI, KALRAY , SOITEC, STMi, RIBER pour ne citer que elles.

Je pense qu’Il faut arrêter de penser uniquement en enveloppes budgétaires

Le vrai sujet, c’est la concentration des moyens, la vitesse d’exécution et la construction d’un avantage industriel défendable sur 10-20-30 ans, comme on a su faire sur le nucléaire. Mieux vaut dominer 3 maillons critiques que subventionner 30 projets moyens.

La France sait faire, nos ingénieurs sont parmis les meilleurs au monde. Maintenant, il faut choisir, accélérer et protéger nos champions.

Notre pays est incroyable mais rendons le indispensable