We still pay on the web like it is the early 2000s. Repeat subscriptions for the news. Large, one-time payments for movies, games and tickets.

It is time to grow beyond payments from your grandma's era. x402 is changing how micropayments on the web work.

Our latest is an exploration of how it works, its impact on ads and what may happen to software pricing. Read below.

Social media monetised attention; the next step is to financialise it.

@TrendleFi lets you trade social trends, and @azuroprotocol brings liquidity to them. Together, it is the recipe to financialise attention.

Our latest on where prediction markets are headed. 👇

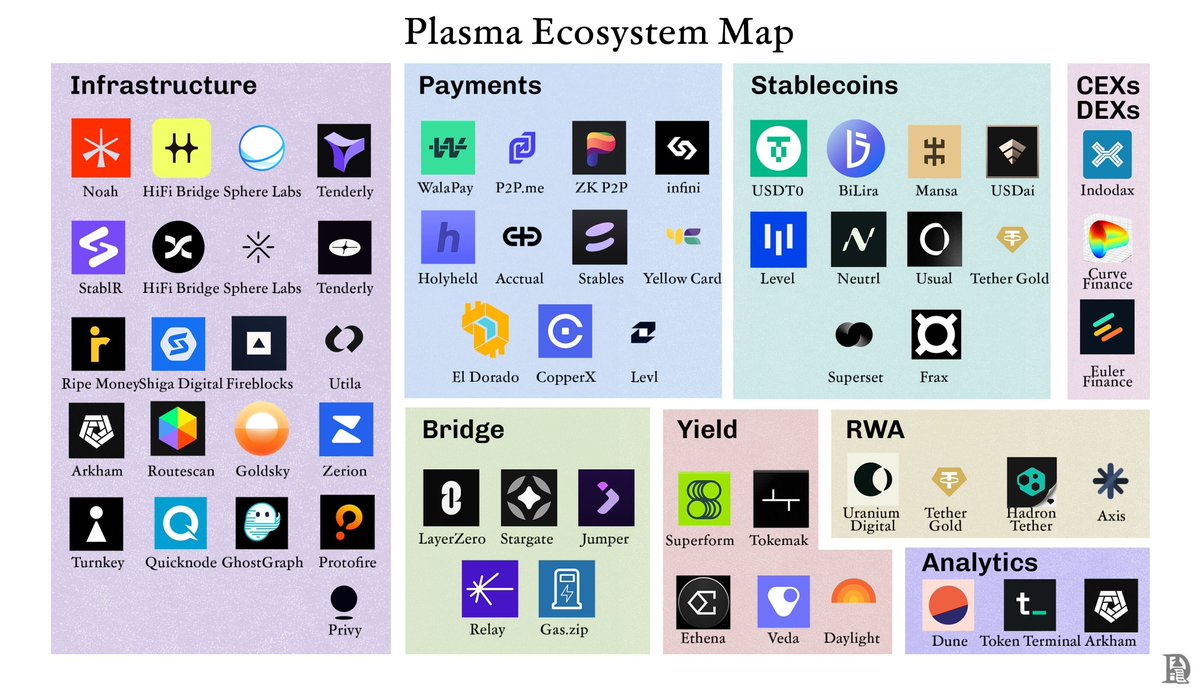

It took shipping containers to help scale commerce.

It will take standardising building blocks to make stablecoins relevant around the world.

Our latest, written with @PlasmaFDN explores how they are creating the gmail moment for money.

Read: https://t.co/YsCJKAel8C

Every app will be a bank and crypto will lead this shift.

In the past decades, banks were run by men in suits in marble lobbies. The banks of the future will run on blockchain rails and be operated by developers that find distribution.

Enabling financial applications in the past meant collaborating with a bank that had licenses. In the US, it could mean owning 50+ transmitter licenses and building rails for compliance. All of this excludes APIs that may have been updated a decade earlier.

Even giants like Google learned the hard way when they tried embedding a wallet into Gmail. Two years of regulatory back-and-forth later, they still couldn’t convince authorities why money should move where the emails move, and the idea got shelved.

That’s why most non-fintech apps don’t even try to add payments, as the regulatory and technical overhead kills it. VCs understand this struggle. Since 2021, the total money flowing to fintech startups has halved.

But the GENIUS Act just changed the calculus. It allows apps and crypto protocols to hold tokenized dollars (stablecoins) for users without needing a traditional bank partner.

Compliance still exists, but it’s scoped for digital assets, and all the core banking functions can be built directly on-chain inside smart contracts.

When custody, compliance, and settlement become code, any product with users can embed money:

- A game that doubles as a savings account.

- A marketplace where sellers earn yield between payouts.

- A social app that lets you tip in dollars instantly, globally.

The shift is irreversible: finance is unbundling into code, and every platform that touches people’s lives will be capable of holding their money.

For a deeper understanding of how banks control money and why crypto will lead the way in making everything a bank, read the full story in our latest publication (link below).

The age of mature aggregators are here and @JupiterExchange is leading the charge. But how?

Our latest tries to explain why the exchange has focused excessively on M&As, expanding product suites & new market primitives to own the end user.

https://t.co/7kt50Xpzzx

Hyperliquid brought CEX liquidity and speed to DeFi. But the magic stopped at perps.

HyperEVM cracks @HyperliquidX's order‑book wide open. Any contract can tap that depth:

- Prime Brokerages

- Perp‑aware lending vaults

- Option AMMs

- MEV resistant auctions

- Structured products

- Delta neutral hedging

- Onchain market makers

I broke down the infra that makes it possible ↓

Everyone talks about disrupting payments with stables.

But insurance is the real cash cow pulling in more than all other banking services put together.

Fintechs have captured less than 1% of this space. Will that change?

The Coming Boom in Crypto Options

Robinhood went all-in on crypto this month, unveiling an @Arbitrum-based L2, rolling out tokenised US equities for anyone with a wallet, and teasing synthetic pre-IPO shares of @OpenAI. However, the first crypto derivative it shipped was perpetuals capped at 3x leverage, not options, which made @RobinhoodApp famous.

This single product choice captures a decade of evolutionary divergence between crypto markets and traditional finance. Traditional markets operate under CFTC constraints that require future rollovers and create operational friction. U.S. regulations cap stock margin leverage at roughly 2x and ban anything resembling "20x perpetuals". Options became the only way for investors with $500 to turn a 1% move in Apple into a 10%+ gain.

This led to explosive growth in the US options market. Nearly half of this activity comes from retail traders punting short-dated options expiring on the same day or by the end of the week. Robinhood built its business around providing quick, easy and free access to options and monetising it via Citadel through a model that’s called payment for order flow.

The Trading Gap

Crypto's unregulated environment, dealing purely in digital assets without physical delivery, created space for innovation. It all began with @Bitmex’s perpetual futures. These futures are unique in that, much like the name suggests, there is no “delivery” date. They are perpetual; you can open a position going up to 100x leverage on any token.

Options are more complex. Investors need to manage multiple variables simultaneously: strike selection, underlying price, time decay, implied volatility, and delta hedging. Most crypto traders evolved directly from spot trading to perpetuals, completely bypassing the options learning curve.

CEXes like @Binance and @Bybit_Official leaned into perpetuals to capture retail demand for leverage. Last month, perp venues cleared roughly US$3.7 trillion in notional value. All crypto options combined cleared just US$100 billion, less than 5% of perp volume.

@DeribitOfficial, the biggest crypto options CEX alone handles 85% of this option flow, highlighting how thin and centralised the market is.

Moving options on-chain looked easy on paper. A smart contract can track strikes and expiries, escrow collateral and settle payouts without middlemen. Yet, after five years of experiments, Option DEXes combined still capture less than 1% of option volume. Compare this to Perp DEXes, which process around 10% of futures volume.

Evolution of On-Chain Options

Options require a counterparty who is willing to take on asymmetric risk. If you bought a BTC call for $100K last year, and the price moved to $115K, the counterparty, known as the option writer, has to pay this $15k out.

They charge a premium based on how likely it is that you might make money, which they calculate using the Black Scholes formula. Higher volatility in the underlying token translates into higher option premia because writers need more compensation for wilder price paths.

1. The first phase of protocols led by @Opyn_ democratised writing by letting anyone lock collateral and underwrite options as ERC-20s and earn premiums. This let users trade options in a peer-to-peer fashion, but gas fees for minting these options burnt more than the premiums. Writers also had to lock the full notional value until expiry, so capital sat idle for months.

2. Builders next pooled collateral in AMM vaults, inspired by Uniswap’s design. @HegicOptions let traders buy an option with a single click while a pricing curve handled the math. The convenience worked, but the vault mispriced puts; one sharp ETH crash in September 2020 wiped out a year of LP yield and reminded everyone that automated pricing without hedging is dangerous.

3. Lyra (now @Derivexyz) tried to solve that by teaching the vault to hedge net exposure on perpetuals. Hedging cut drawdowns in half, yet the design relied on @synthetix’s DEX liquidity. When the Terra–Luna panic emptied those pools, hedges failed to fill, and option spreads ballooned, making trading impossible.

4. Projects like @RibbonFinance tried underwriting calls as a way to provide yield. Depositors sent ETH to an option vault that auctioned calls expiring in a week. During the bull market, these premiums looked amazing, but when ETH slid, the income no longer covered losses and users were stuck with their positions until expiry.

5. Finally, Solana and Optimism teams such as @PsyOptions, @DriftProtocol,@Aevoxyz and Derive tried to recreate Deribit’s order book, matching trades off-chain and settling on-chain. They onboarded market makers who could prove tight spreads. But makers still had to post fresh collateral for every leg because the smart contracts couldn’t recognise that a short call hedged with spot carries little net risk. Liquidity dried up whenever those makers logged off.

Why Options Struggle

A market-maker selling a $120K BTC call and delta-hedging with spot BTC has near-zero net risk. Deribit recognises that and charges a margin on the combined net exposure. Most on-chain designs tokenise each option in isolation, severing the risk link. Every hedge ties up fresh collateral, so market makers' quotes get wider.

While Derive has partially addressed this by adding perpetuals to enable cross-margin within their clearinghouse, spreads remain significantly wider than Deribit's; often 2-5 times fatter for large positions.

Contrast that with @HyperliquidX, the DEX that now clears about 6% of all perp volumes and matches CEX spreads. Hyperliquid’s secret isn’t novel math; it is plumbing. A single global liquidity pool called HLP sits on the other side of every trade. Traders see one order book, one funding rate, no strike grids and no expiries. The cognitive load is near zero, and the UX is smooth. Longs and shorts take opposite sides of the trade. When net exposure gets lopsided, the protocol’s risk engine hedges on external venues or throttles leverage.

Onboarding new markets is equally painless. Seed a pool, list the asset, and trading can begin without cajoling market makers.

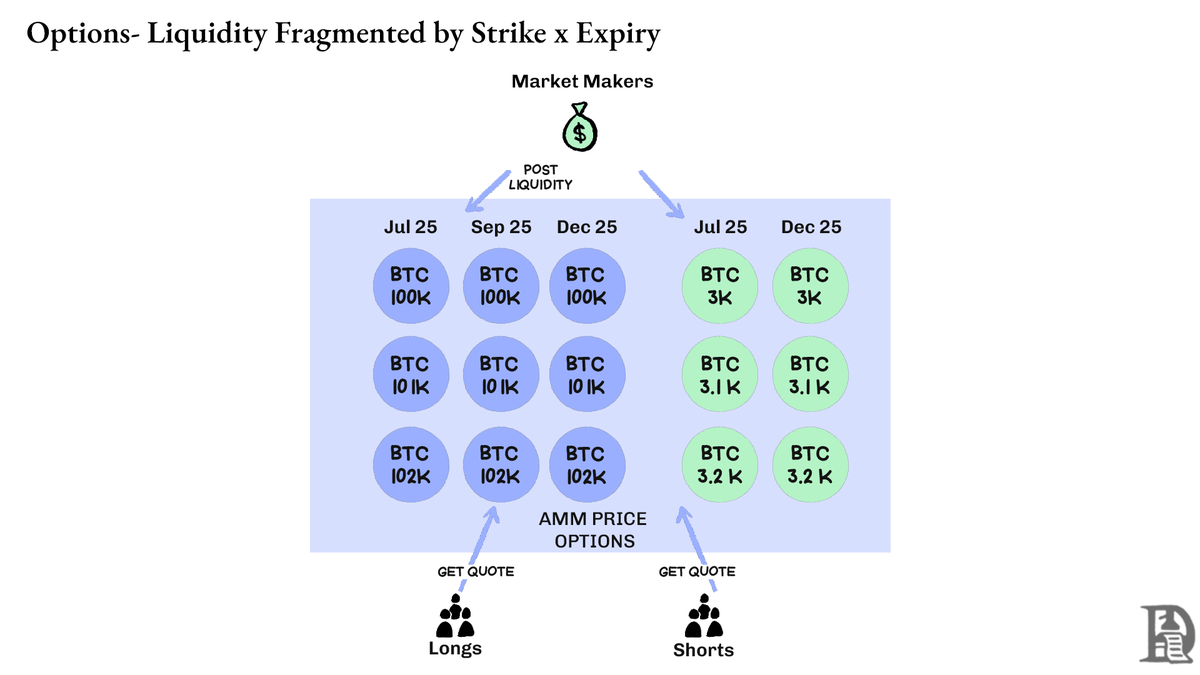

Options, by contrast, splinter liquidity across thousands of micro-assets. Each strike-expiry combination creates its own market with distinct characteristics, dividing available capital and making it nearly impossible to achieve the depth that sophisticated traders require.

Writers’ capital sits frozen until settlement, spreads stay wide, and the seamless UX that powers perps never materialises. This is at the heart of why on-chain options have not taken off.

The Missing Piece

Ironically, the infrastructure that powers Hyperliquid could be exactly what on-chain options have missed. We've written about Hyperliquid's approach to shared infrastructure, creating the positive-sum dynamics that DeFi has long promised but rarely delivered. Every new application strengthens the entire ecosystem rather than competing for scarce liquidity.

We believe that options will finally come on-chain through this infrastructure-first approach. While previous attempts focused on mathematical sophistication or clever tokenomics, HyperEVM solves the fundamental plumbing problem: unified collateral management, atomic execution, deep liquidity and instant liquidation.

There are a few core aspects to changing market dynamics that we see:

1. In the post-FTX crash of 2022, there were fewer market makers in the market engaging with new primitives and taking on risk. Today, that has changed. Participants from traditional avenues have returned to crypto.

2. There are more battle-tested networks that can take on the needs of higher transaction throughput.

3. The market is more open to some of the logic and liquidity not being entirely on-chain.

Options have the Lindy effect and volatility, but are hard for the average individual to understand. We believe there will be a class of consumer apps that focus on bridging this gap, helped along by LLMs that can check premiums and suggest the most attractive strike in plain English.

Tokens will do to assets what the internet did to information. The floodgates are open.

Everything will be a token and much like with the attention economy, there will be a power law for how liquidity concentrates in the new internet.

You can’t make this up:

On May 23rd, President Trump threatened Apple, $AAPL, and Samsung with a 25% tariff on phones not made in the USA.

This was the first Trump tariff in 2025 to target individual companies.

Today, exactly 24 days later, the Trump Organization announced “Trump Mobile.”

“Trump Mobile” will be using phones made in the USA.

Truly incredible.

$CRCL is now trading at $133, 4.5x up since its IPO 10 days ago.

I wrote about how @circle is well positioned in the stablecoin space but even I didn't guess they would be eating this good.

Who are some folks building options products --

team working internally on a story around the evolution of options and impact of derivs market on token volatility

Happy to chat .

May be cooking something on the side too. Idk tho.

Stablecoins are money on crack cocaine.

But what is the financial engineering that goes behind these instruments? And what does it hint about the future?

Our latest story seeks answers to these questions alongside breaking down the GENIUS act.

Much like a 20 year old figuring out life - the US government tends to run out of money occasionally. It issues bonds to bridge the deficit. Credit cards, but for nation states.

A quarter of this debt is normally soaked up by foreign buyers such as Japan, China and the petrodollar bloc. These countries export goods to the US and earn dollars. Converting them into the local currency in the forex markets would spike exchange rates and make exports more expensive, gutting competitiveness. So these countries reinvest the dollars into US debt. It’s a neat vendor-financing loop that financed America’s rise.

But that loop is currently faltering. Tariffs, credit downgrades and geopolitical tensions are scaring buyers. If there’s no demand for fresh debt, the US Treasury will have to offer higher yields. Interest rates would go up, and the debt spiral would worsen. Washington needs a new buyer.

The GENIUS Act turns stablecoin issuers into the new mega-bid. Every “qualified” stablecoin must park an equivalent amount of USD issued into Treasuries and other high-quality liquid assets. Stables must also provide real-time FATF-compliant attestations and the ability to sanction addresses.

Washington gets an always-on, transparent currency, while global freelancers get the option to save in Dollars with just their Gmail login.

Stablecoins started as a way to escape from crypto’s volatility and save in a fiat backed currency. Now they have become the cheapest cross-border FX rail. In Argentina, Brazil, and pretty much anywhere the local currency depreciates, stables are the easiest way to store value without touching a U.S. bank. And we see how this translates to volume. As of writing, Stablecoins have begun doing more in transaction volume than Visa.

Regulation gives the sector institutional legitimacy. If stables capture even 5% of global dollar balances by 2030, that’s a market cap of $1.5 Tn. That will make them the largest holder of US Treasuries, ensuring a fresh base for federal debt. Without it, the US will be forced to offer higher yields on their debt and service ever-growing interest payments.

Our thinking is that stablecoins are the next frontier for fintech. They are the fastest rails for founders to build, deploy & onboard a global scale banking experience. They are also one of the few instances where crypto becomes relevant to the average individual - without elements of speculation involved.

If you are a founder building atop these new money primitives - read our latest to explore the past, present & future of how money moves on-chain. Link below.

Want to show token balances in your DeFi app? There's no Ethereum endpoint for that. Need user transaction history? Doesn't exist. Crypto apps rebuild the same data infrastructure from scratch. @mewwts takes us through how @Dune is fixing it.

Chapters —

00:00 The Evolution of Dune and On-Chain Data

08:00 User-Generated Content and Community Engagement

14:03 Dune's New Product Suite

17:48 The Future of On-Chain Data and Infrastructure Challenges

21:13 Navigating Solana's Data Challenges

24:10 The Evolution of On-Chain and Off-Chain Data

26:33 Understanding Data Strategies in Crypto Applications

29:59 The Future of AI in Data Analytics

33:12 Reflections on the Crypto Landscape

34:31 How Dune Thinks About Acquisitions

39:12 Future Directions for Dune's Product Development