LPs sometimes ask me who I think the best VC investors in crypto are.

I think about this a lot.

Ever since I started as a crypto VC, I have wanted to be the best. I’m deeply driven by competition, and investing is as pure of a competition as it gets. Only one person can win the deal, only one person can pick the winner of the cycle.

But when you honestly look at it and do the accounting, there are three people who have proven themselves the GOATs of crypto VC investing.

This is going to seem like glazing (it is) and probably not interesting to anyone who's not a crypto VC. But I am. So this is for all of us who make this our life’s work.

Here are my all-time top 3.

#3. @danrobinson (@paradigm)

There’s a legendary story about how Mike Speiser, Managing Partner at Sutter Hill Ventures, incubated Snowflake, which went on to become a $75B company. A VC adding that much value to a portfolio company is basically unheard of.

Dan Robinson is the Mike Speiser of crypto.

Again and again, Dan has been at the ground floor of generational companies in crypto. He was there from the very beginning of Uniswap, literally a co-author and foundational contributor to Uniswap V3, which became the backbone of on-chain spot trading. He was a critical contributor at the beginning of Flashbots, which birthed modern MEV auctions. And he was an early research contributor to Plasma, the predecessor of modern rollups, which led to him leading the seed round of Optimism.

Dan is a genuine polymath. He breaks the mold of a traditional VC. He started as a securities lawyer, then became a self-taught protocol architect and mathematician, and is now a self-taught investor. Perhaps the greatest investment that @matthuang ever made was hiring Dan. When we lose deals to Paradigm, so often it’s because people say: yeah you guys are great, but sorry, I have to work with Dan.

The scariest investors are people who can do more than just invest. Dan saw where it was all going, and he rolled up his sleeves and helped make it happen, multiple times. That’s what makes him one of the greatest to ever do it, and earns him his spot on the crypto Mt. Rushmore.

#2. @cdixon (@a16zcrypto)

Chris Dixon is the OG’s OG. He saw it before anyone. Before Chris, crypto VC was minor leagues.

He was the first mainstream VC to throw his hat in the ring and publicly bet his career on crypto. He was the first to adapt the language of VC to crypto and network investing. He was the first to socialize these concepts with Silicon Valley and its universe of institutional LPs. So many concepts we bandy about every day in our IC, we stole directly from Chris. It’s not an exaggeration to say I am walking along the train tracks that Chris set down originally for himself.

There are two most important deals that I attribute to Chris Dixon. The first, of course, is Coinbase. Chris led the Series B of Coinbase in 2013, at a time when the industry was still fledgling and none of this was obvious. That deal is the apotheosis of the Dixon-ism—"what the smartest people are doing on the weekends is what everyone else will be doing in 10 years." He had the foresight to do that deal, and then doubled down to go all-in on the industry. It was so much harder to do what we are now doing at the time when Chris first did it.

Second deal was Uniswap. Almost everyone who saw the Uniswap Series A passed on the deal ($100M FDV—Uniswap was still tiny back then). At the time we were having heated debates about whether AMMs were capital-efficient enough, whether they’d face too much adverse selection, whether they were too easily forkable. Paradigm passed (despite leading the seed round), we passed as well, and from what I’ve heard, everyone else at the a16z IC didn’t want to do the deal.

But Chris? Chris supposedly said: “A smart contract that can buy and sell anything? That sounds so cool. Who knows what will happen—let’s just do it.” And he was right. It was cool. All sorts of non-obvious things would happen because of what permissionless AMMs enabled. I learned a big lesson after passing on that Series A.

I disagree with the a16z worldview in many ways. But everyone in this industry owes Chris enormous credit. He has single-handedly done more than any other VC to put the industry onto the cultural footing it now has, has fought tooth and nail with his career to legitimize crypto in DC, and has earned us cultural recognition as a positive frontier technology. So much of the language we use about crypto was imbibed directly from Chris.

Crypto VC would not be where it is today were it not for Chris Dixon championing it as early as he did. For that, we owe him deep gratitude.

And that leads to the #1 VC of all time...

#1. @KyleSamani (@multicoin)

Kyle, Kyle, Kyle.

I give Kyle a lot of shit. He rubs a lot of people—including me—the wrong way. All the time.

But investing is like a sport. At the end of the day, you either put up points on the board, or you don’t.

And Kyle has put up the most points of anyone. The sheer scale of PnL he made from his Solana seed round investment, the amount of work he did for that deal, someone will write a book about it someday, and I’ll be grimacing the whole time while I read it.

You see, the best investors are contrarians. And Kyle is a true contrarian. To be a contrarian doesn’t mean that you write a hot take that gets a bunch of people to say "wow that was smart." If everyone wants to retweet you, by definition you’re not a contrarian. You’ll know you’re a true contrarian when you piss people off. When people think you’re an idiot. When they think you’re lighting your money on fire.

Kyle is one of the only true contrarians in crypto. I disagree with him about almost everything. But his original investment and subsequent conviction on holding Solana through the depths of the valley of darkness after the collapse of FTX, make him, bar none, the best VC investor in crypto history.

We always say that venture is a power law business. Kyle and his legendary Solana investment is precisely what we all mean by that. Sometimes it genuinely only takes one deal.

And that’s what makes Kyle the best crypto VC of all time.

So that’s my top 3.

---

LPs sometimes ask where I think I should go on this list.

As much as I think highly of myself—and boy do I think highly of myself—I don’t think I’m top 3. I’m top 10 for sure, and there’s an argument for top 5, but I’m not better than any of these three. I hope to be, someday, before I’m done. And if you break it out by seasons, there are seasons I’ve done better than each of them.

But in aggregate? These three are the best to ever do it.

It’s not helpful to Dragonfly for me to praise our competitors. But there’s a game bigger than the game. You see, this is a hard industry to be an investor in—most of the peers I’ve had along the way have not survived. Crypto is brutal.

As much as I compete with these guys every day, I have enormous respect for them. I've seen them evolve through almost a decade of ups and downs. We've all endured through the vicissitudes of crypto together to support our founders, to support this industry, and to help it stand shoulder-to-shoulder next to any other technology. As I was doing some end-of-year reflection, I thought it was worth acknowledging them in an industry that often doesn't give out much praise to VCs.

Each of these people have done a lot for me, whether they know it or not. I've learned so much from each of them. And I genuinely hope they are proud of what they’ve accomplished.

Dan Robinson saw it clearly.

Chris Dixon saw it first.

And Kyle Samani saw it through.

Hats off, gentlemen. Here’s to another vintage of competition. 🫡

im increasingly convinced that the best way to bet on a particular sector is simply to own the top 1 or 2 dominant players. the laggards may feel cheap and u tell urself they have much more room to grow, but they r often at a massive disadvantage in terms of economy of scale and network effects. good companies stay good and bad companies stay bad.

In Defense of Exponentials

I used to tell founders, the reaction you are going to get to your launch is not hate, it’s indifference. By default, nobody cares about your new chain.

I have to stop telling them that now. Monad just launched this week, and I’ve never seen so much hate about a blockchain that just launched. I’ve been investing into crypto professionally for 7+ years now. Before 2023, almost every chain I’ve ever seen that launched was mostly met with enthusiasm or indifference.

But now, new chains are born into a chorus of hate. The amount of haters I’ve seen for projects like Monad, Tempo, MegaETH—before they even hit mainnet—is a genuinely new phenomenon.

I’ve been trying to diagnose: why is this happening now, and what does it mean about the psychology of this market?

The Cure is Worse than the Disease

Forewarning: this is going to be the vaguest blockchain valuation post you ever read. I don’t have any fancy metrics or charts to sell you on. Instead, I’ll be arguing against the zeitgeist of Crypto Twitter, which for the last couple of years, I’ve been constantly on the opposite side of.

In 2024, I felt like what I was arguing against was financial nihilism. Financial nihilism is the belief that none of these assets matter, it’s all memes at the end of the day, and everything we’ve built is inherently worthless.

Thankfully, that’s no longer the vibe. We have broken out of that spell.

But the zeitgeist now is what I’d call financial cynicism: OK, maybe some of this stuff has value, maybe it’s not all memes, but it’s grossly overvalued and it’s only a matter of time before Wall Street finds that out. Not that all chains are worthless. But these things are all maybe worth 1/5th-1/10th of what they’re currently trading at (have you seen these PE ratios?), and so you’d better pray like hell Wall Street doesn’t call us on our bluff, because once they do it’s all getting wiped out.

You’ve got many bullish analysts now trying to conjure up optimistic L1 valuation models, inflating PE ratios, gross margins, DCFs, trying to fight against this mood.

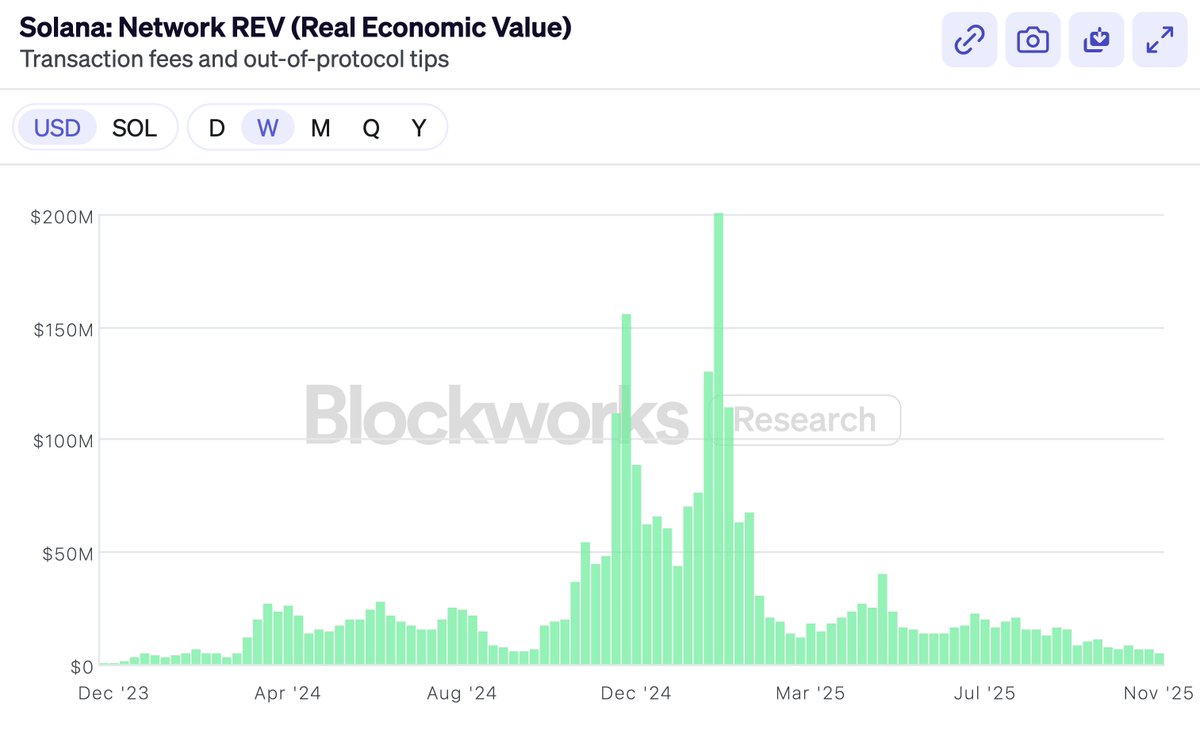

Late last year, Solana very proudly embraced REV as a metric that could finally justify their valuation. They proudly announced: we—and only we—are no longer bluffing to Wall Street!

And, of course, almost immediately after REV was embraced, it fell off a cliff (though $SOL, tellingly, did better than REV did).

Not that there’s anything wrong with REV. REV is a very clever metric. But the point of this post is not metric selection.

Then came the launch of Hyperliquid. A DEX that had real revenue and buybacks and PE multiples. And the chorus said—look, look I told you! Finally, for the first time ever, a token that has some real profits and a proper PE multiple. (Nevermind BNB, we don’t talk about that.) Hyperliquid will eat everything because obviously Ethereum and Solana don’t make any real money, we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these buyback-heavy tokens are all great. But the market always had the ability to invest into exchanges. You could always buy Coinbase, or BNB, or whatever. We own $HYPE, and I agree that it’s a fantastic product.

But that’s not why people were investing in ETH and SOL. The fact that L1s don't have exchange-like profit margins is not why people were buying them—if they wanted that, they could’ve bought Coinbase stock.

So if I’m not critiquing blockchain financial metrics, maybe you think this post is going to be chiding the sinfulness of the token-industrial complex.

Obviously, everyone has lost money on tokens in the last year, VCs included. Alts are down bad this year. And so the other half of the zeitgeist on CT is arguing about who's to blame. Who’s become greedy? Are the VCs greedy? Is Wintermute greedy? Is Binance greedy? Are the farmers greedy? Are the founders greedy?

The answer, of course, is the same as it’s ever been.

Everyone is greedy. Everyone. The VCs, Wintermute, the farmers, Binance, the KOLs, they're all greedy, and you are greedy too. But it doesn't matter. Because no functioning market has ever required anyone to act against their self-interest. If we're right about crypto, we can all be greedy and the investments will still work out. Trying to analyze a market that has gone down by figuring out “who’s greedy” is going to be about as fruitful as commissioning witch trials. I guarantee you, nobody just started being greedy in 2025.

So this, too, is not what I’m going to be writing about.

Many people want me to write a post about why $MON should be valued at X or $MEGA at Y. I’m not interested in writing this post, or advocating that you buy anything in particular. In fact, you probably shouldn’t buy any of them if you don’t already believe in them.

Will any new challenger chain win? Who knows. But if it has a material chance of winning, it's going to be priced on that basis. If Ethereum is worth $300B or Solana is worth $80B, a project that has a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow CT is scandalized by this, but it’s no different than Biotech. A drug that has less than a 10% chance of curing Alzheimer's is priced by the market as worth billions of dollars, even if 90% chance it won’t pass stage 3 trials and will go to 0. That's how the math works—and turns out, markets are pretty good at doing math. Binary outcomes are priced on probabilities, not on run rates or moral turpitude. It’s the “shut up and calculate” school of valuation.

I really don’t think that’s an interesting question to write about. “5% chance to win? No way, that’s clearly a 10% chance!” Markets, not articles, are the best way to assess that for any individual token.

So here’s what I am going to write about: CT doesn't seem to believe anymore that chains are valuable.

I don’t think this is because they don’t believe new chains can win market share. We just saw Solana dominate market share after emerging from the ashes less than 2 years ago. It’s not easy, but of course it’s possible.

It’s more that people have come to believe that even if a new chain wins, there’s no prize worth winning. If $ETH is just a meme, if it’ll never generate real revenue, then even if you win, you won’t be worth $300B. The contest is not worth winning, because these valuations are all bunk and it’ll all come crashing down before you go to claim your prize.

Being optimistic about chain valuations has become passé. Not that nobody is optimistic—obviously there must be optimists out there. For every seller there’s a buyer, and as much as CT cool kids love to drag L1s, people are comfortable buying SOL at $140, ETH at $3000.

But there’s a perception now that all the smartest people are over buying smart contract chains. Smart people know the jig is up. If not now, then soon. The only people buying here are suckers—Uber drivers, Tom Lee, and KOLs who say stuff like “trillions.” And maybe the US Treasury. But not the smart money.

This is bullshit. I don’t believe it, and you shouldn’t either.

So I felt like I had to write a smart person’s manifesto on why general purpose chains are valuable. This post is not about Monad or MegaETH. It’s really in defense of ETH and SOL. Because if you believe ETH and SOL are valuable, the rest is straight downstream.

Defending ETH and SOL valuations is generally not my job as a VC, but fuck it, if nobody else is willing to do it, then I’ll write it.

Feeling the Exponential

My partner Bo experienced the Chinese Internet boom first-hand as a VC. I’ve heard how “crypto is like the Internet” so many times now that it doesn’t even register for me anymore. But when I hear his stories, it always reminds me how costly it is to be wrong about these things.

A story he often tells is about when all the early e-commerce VCs (it was a small group back then) got together for coffee in the early 2000s. They debated: how big is the market for e-commerce going to be?

Is it going to be mostly electronics (maybe only techies will use PCs)? Could it ever work for women (perhaps they’re too tactile)? What about food (maybe impossible to manage perishables)? These were deeply important questions for early VCs to decide what to invest in and what prices to pay.

The answer, of course, was that literally every single one of them was devastatingly wrong. E-commerce would sell everything, and the target audience was the whole fucking world. But nobody at the time actually believed it. And even if they did, it would be too absurd to say out loud.

You just had to wait long enough for the exponential to show you. Even among the believers, very few thought e-commerce would become as big as it became. And those few who did, almost all of them became billionaires from just not selling. Every other VC—as Bo tells me, since he was one of them—sold too early.

It has become passé in crypto to believe in the exponential.

I believe in the crypto exponential. Because I’ve lived it.

When I started in crypto, nobody used this stuff. It was tiny and broken and awful. TVL on-chain was in the millions. We invested into the first generation of DeFi, MakerDAO, Compound, 1inch, back when they were science projects. I remember playing around on EtherDelta back when DEXes traded single digit millions a day, and that was considered to be a huge success. It was complete dogshit. Now we routinely trade in the tens of billions on-chain every day. I remember believing it was crazy that Tether hit a billion dollars in issuance and was being written up in the NYT as a ponzi scheme on the brink of shutdown. Now stablecoins are over $300B and regulated by the Federal Reserve.

I believe in the exponential because I’ve lived it. I’ve seen it over and over again.

But you might respond—well, stablecoin growth might be exponential, maybe DeFi volumes are exponential, but they don’t accrue to ETH or SOL. The value doesn’t get captured by the chains.

To which I answer: you still don’t believe in the exponential.

Because the exponential’s answer is always the same: it doesn’t matter. This stuff is going to be so much bigger than it is today. And when it’s absolutely enormous, you’ll make it up on scale.

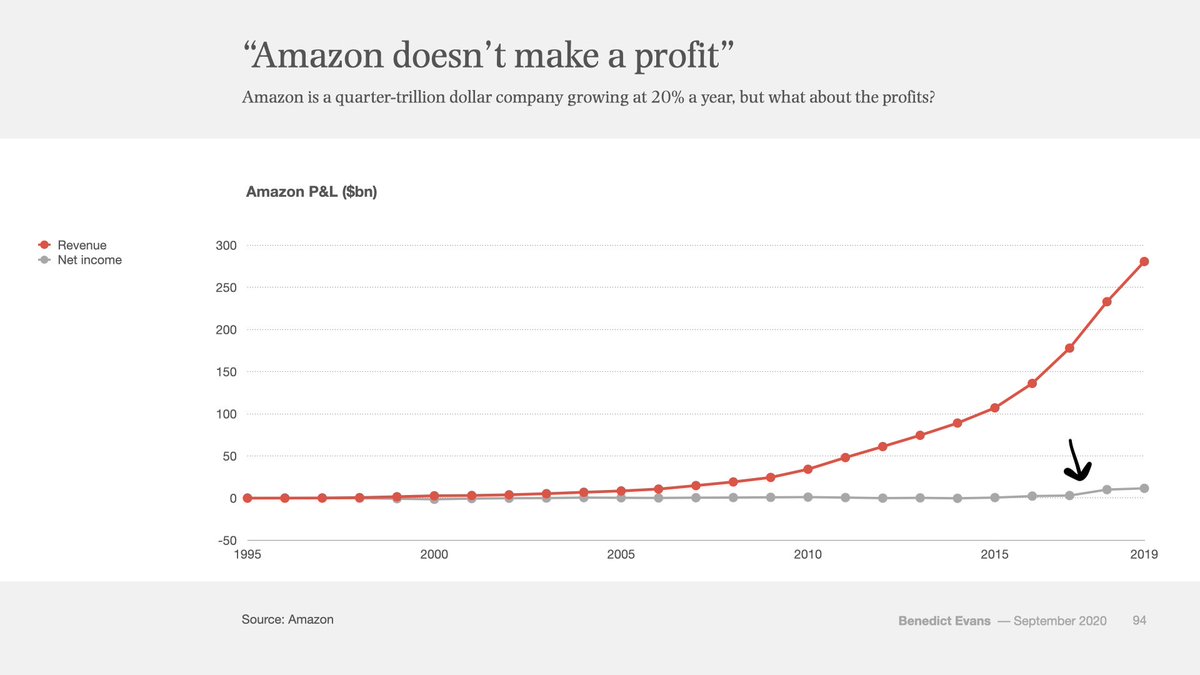

Study this chart.

This is Amazon’s P&L from 1995 to 2019. That’s 24 years. Red is revenue, gray is profit. You see that little blip on the end where the gray line goes up? That’s when, 22 years in, Amazon started actually making a profit.

Amazon was 22 years old when this little gray line of net income first peeled off of 0. Every single year before then, there were op eds and critics and short sellers claiming that Amazon was a ponzi scheme that would never make any money.

Ethereum just turned 10 years old. This is what the first 10 years of Amazon stock looked like:

10 years of chop. All along the way, Amazon was beset with doubters and non-believers. Is e-commerce a VC-subsidized charity? They’re selling underpriced cheap low-quality knick-knacks to bargain hunters, who cares? How are they ever going to make actual money, like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong regime. That’s the regime of linear growth. But e-commerce was not a linear trend, and so every single person for 22 years arguing about P/E ratios was devastatingly wrong. No matter what you paid, no matter when you bought, you were not bullish enough.

Because that’s what exponentials do. When it comes to truly exponential technologies, no matter how big you think it’s going to get, it just keeps getting even bigger.

This is the thing that Silicon Valley has always understood better than Wall Street. Silicon Valley was raised on exponentials, while Wall Street was raised on linearity. And over the last few years, crypto’s center of gravity has migrated from Silicon Valley to Wall Street. You can feel it.

Granted, crypto growth doesn’t look as smooth as e-commerce’s growth. It’s burstier, it goes in fits and starts. This is because crypto, being about money, is deeply tied to macro forces, and it also has more violent regulatory push and pull than e-commerce. Crypto strikes at the heart of the state—money—and so it’s more unnerving to governments than e-commerce ever was.

But the exponential is no less inevitable. It's a crude argument. But if crypto is exponential, then the crude argument is correct.

Zoom out.

Financial assets want to be free. They want to be open. They want to be interconnected. Crypto turns financial assets into file formats, makes it as easy to send a dollar or a stock as to send a PDF. Crypto makes it possible for everything to talk to everything. It makes it all 24/7, global, interconnected, and open.

That will win. Open always wins.

If there’s no other lesson I've learned from the Internet, it’s that. Incumbents will fight against it, governments will huff and puff, but eventually they will give up against the adoption, the generativeness, the sheer efficiency that this technology enables. It’s what the Internet did to every other industry. Blockchains are how that same trend will gobble up all of finance and money.

Yes—with enough time—all of it.

An old saying goes: people overestimate what can happen in two years, but they underestimate what can happen in ten.

If you believe in the exponential, if you zoom out enough, then it’s all still cheap. And it should humble you that every day, the holders outlast the sellers and naysayers. Big capital has a longer time horizon than CT swing traders might lead you to believe. Big capital has been trained through history not to fade big technologies. You know, the big gushy story that originally got you to buy $ETH or $SOL? Big capital believes that story and hasn't stopped.

So what exactly am I arguing?

I am arguing that applying P/E ratios to smart contract chains (the “revenue meta,” as it’s now called), is giving up on the exponential. It means you have consigned this industry to the regime of linear growth. It means you believe 30 million DAUs on-chain and <1% of M2 is it. Crypto is just one of the things in the world. A sideshow. It did not win. It was not inevitable.

More than anything, I’m arguing to be a believer. Not just a believer, but a long-term believer.

I’m arguing that this exponential will be bigger than anything else you’ve been a part of in your life. That this is your e-commerce. That you will look back when you’re old and tell your kids—I was there when it all happened. Not everyone believed it was possible, that whole societies could change, that all of money and finance would be transformed by programs running on decentralized computers that we collectively owned.

But it actually happened. It changed the world.

And you were a part of it.

Disclosure: These are my own views. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY among many other tokens. Dragonfly believes in the exponential. This is not investment advice, but is advice of another kind.