1/ Mass adoption for NFTs may be far closer than you think.

I spent 3 months studying abroad in Paris, researching Product NFTs, digital luxury, and attending @nft_paris

Here's my thesis on Luxury in Web3 - or when watches become NFTs

[TLDR in Thread]

https://t.co/rmJ7FB63ve

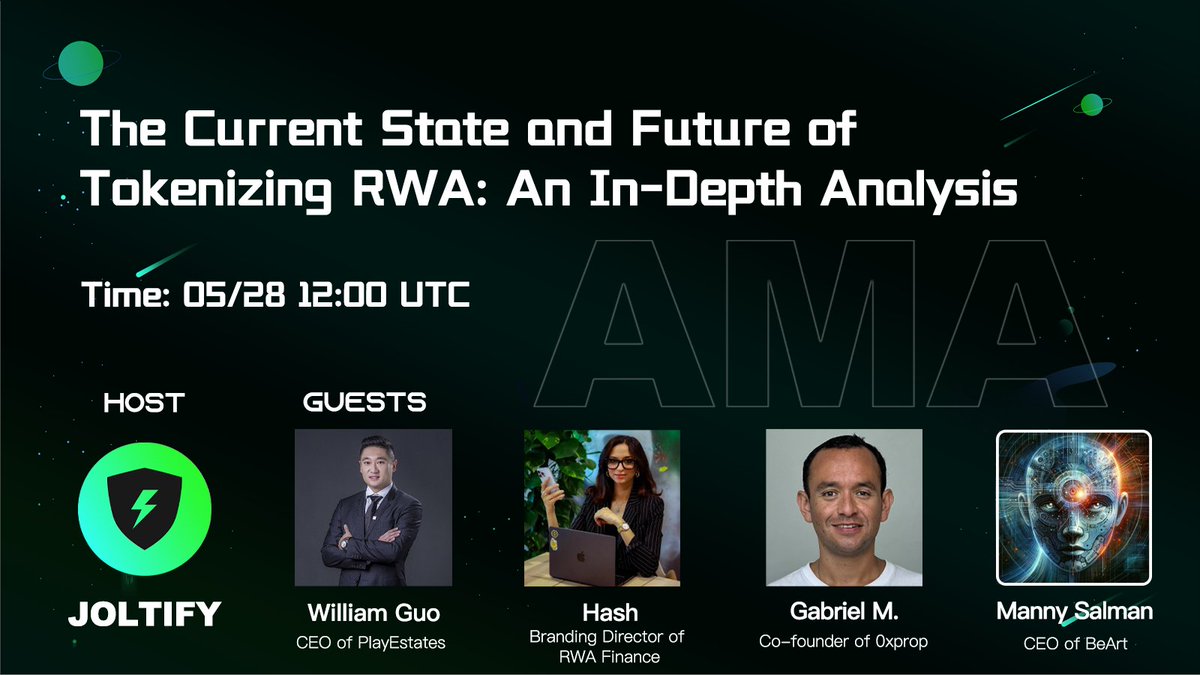

Reminder for upcoming AMA session

We’re excited to announce our upcoming AMA on a highly relevant and transformative topic: The Current State and Future of Tokenizing Real-World Assets (RWA): An In-Depth Analysis.

📅 Date & Time: May 28, 12:00 UTC

📍Platform: Twitter Space

Whether you’re a seasoned professional in the digital assets space, an investor looking to understand new opportunities, or just a curious learner, this AMA is for you.

Meet Our Panelists:

👤 George – Co-founder of @joltify_finance

👤 William Guo – CEO of @PlayEstates

👤 Hash – Branding Director of @RWA_Finance_

👤 Gabriel M – Co-founder of @0x_prop

👤 Manny Salman – CEO of @BeArt_RWA

See you there!

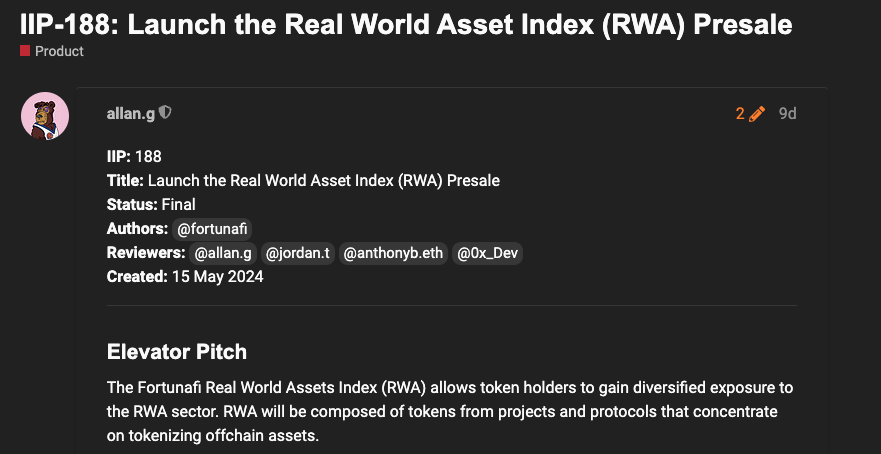

We're excited about this proposal to bring CFG to an onchain RWA index on @indexcoop!

Read the full proposal from @_Fortunafi here: https://t.co/gwaXv7Ji4i

Tomorrow: Join @AIMA_org and our General Counsel @JusNode to discuss navigating legal structures for blockchain finance and tokenization.

On the agenda:

• Legal structures available for compliant blockchain investment transactions

• Types of Tokenized Fund Offerings

• Recent and future developments in the blockchain finance legal landscape

Also on the panel:

• @kkirkbos | Chief Legal Officer @CBOE

• Trish O'Donnell | Partner @reedsmithllp

• Casandra Carpenter | Shareholder @Polsinelli

Moderated by James Delaney of AIMA!

Register for the webinar below ⬇️

https://t.co/yWs9oi4koZ

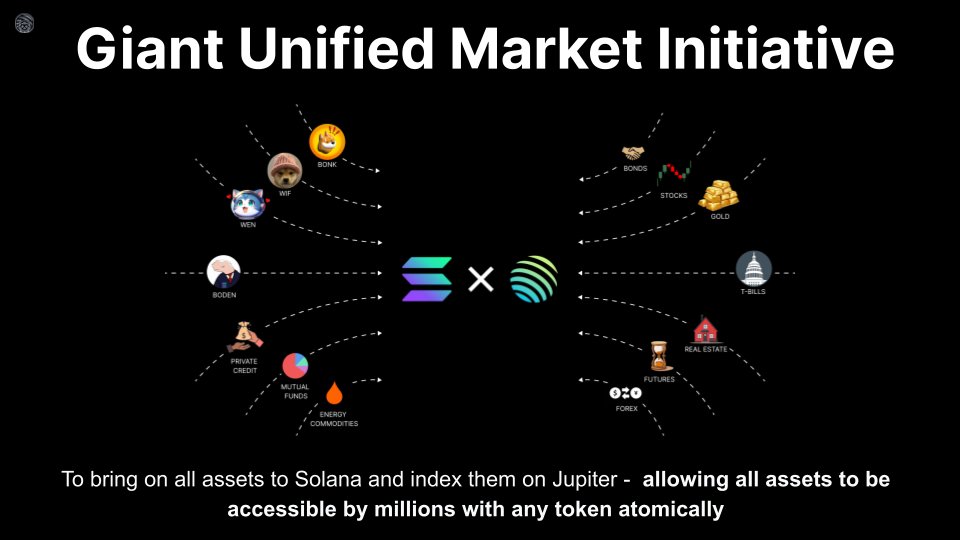

1/ Today, we’re kicking off the Giant Unified Market initiative - our key effort to bring all assets into a single atomic market, accessible by everyone in the world with a fraction of a cent.

Only on Solana, powered by Jupiter, enabled by the best partners in crypto.

1/ a perp-first real world asset listing strategy will front-run tokenization with a better primitive and make tokenization on most assets effectively obsolete

a thread:

If you're interested in tokenized assets, it's good practice to understand real-world financial products!

In this article, we summarize the Centrifuge Credit Group's asset primers on U.S. Treasuries, U.S. Corporate Bonds, and Asset-Backed Securities ↓

https://t.co/PpY3TeSHIu

The institutional adoption of crypto and DeFi is rapidly gaining momentum, and with it an increasing demand for on-chain credit. Clearpool’s launch of Credit Vaults on Avalanche signals a paradigm shift in on-chain RWAs.

Learn about @ClearpoolFin's Credit Vaults with CEO & Founder @JKronbichler, on the recording of last week’s Money Moves Spaces: https://t.co/UqwTgQiIqe

Yesterday I published an update on real-world assets (RWAs) for @MessariCrypto pro subscribers, as the TVL in RWA protocols has grown from about $2 billion at the start of 2023 to around $7-8 billion currently. Not all RWAs are created equal, and markets appear to recognize these differences.

RWAs can be categorized in two primary ways. First, does the tokenized product yield returns for the end user? Yield-bearing RWAs now represent over 80% of the RWA TVL, highlighting the market's preference for assets that generate returns. This trend is likely driven by low demand for tokenized alternative assets; instead, markets are primarily interested in accessing offchain yield opportunities.

The second categorization concerns whether the end user holds a debt or equity position. This can generally be determined by whether the end users are subject to the price fluctuations of the underlying assets generating the yield. For instance, if the users are not exposed to such fluctuations, as seen with yield-bearing stable coins pegged to the dollar, then they are almost certainly in a debt position. Conversely, if the user's position can fluctuate based on the AUM of the protocol, then it's an equity position.

Markets also show a preference for debt positions over equity positions within yield-bearing assets, with debt positions holding a 70% market share. Notably, there is a correlation between TVL and yield, with Ethena having the highest TVL and yield among these protocols. This is likely because these protocols primarily denominate their debt in USD, presenting an alternative to traditional stable coins. Thus, the generated yield needs to adequately compensate users for both the risk associated with the product and the lower liquidity of their dollar position.

TLDR: Users are seeking exposure to offchain interest rates without any price exposure to underlying offchain assets.

🚨 Announcing the Stablecoins Dashboard 🚨

Today we're launching the most comprehensive view into crypto's biggest real world use case. Check out the most notable institutional and asset-backed stablecoins 🧵👇

The real innovation of crypto isn't tokenization -- it's assetization.

Assets have been always expensive to create.

They either need to be physical goods, or have complex ownership, accounting, and payment structures to make them trustworthy and useful.

Crypto makes the costs of creating an asset go to zero.

Ownership, transfers, accounting, payments are all built into the platform.

It means you can create an asset like bitcoin which rises to challenge conventional monetary theory.

It means anyone can create a memecoin which captures a cultural moment and forms communities at internet speed.

The arc of technology shows us that when the cost of something goes to zero, it unlocks a long tail of new possibilities that forces us to rethink everything that came before.

I'm more excited than ever to see what kind of weird assets we create next.