Deep Dive is out my terminally online friends. A nice weekend read to bring you upto speed on everything Prediction Markets.

I talk - a lot in here. Bear with me!!

The aim is for anyone reading to choose the topics of their interest and then explore that topic further

1. Why do we need onchain prediction markets?

2. How are modern prediction markets designed?

3. The absolute dominance of @Polymarket and @Kalshi

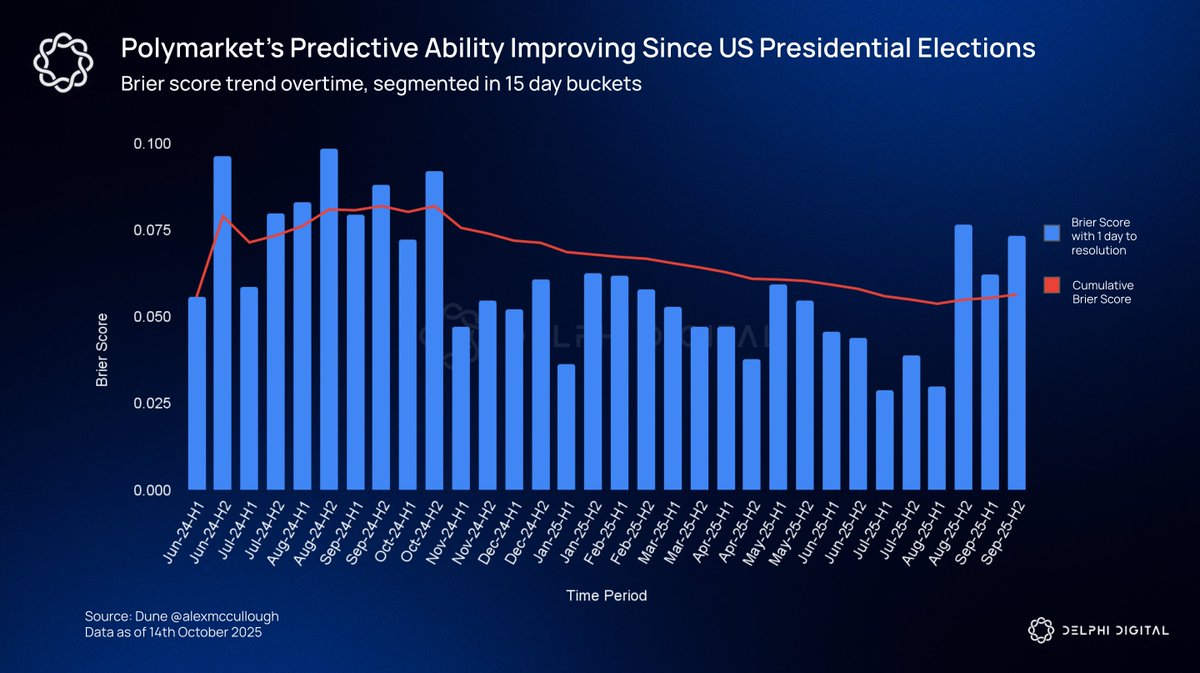

4. The Predictive Power of Prediction Markets

5. Five Unsolved Problems plaguing the category

6. Some recommendations for solving these problems (And the startups already doing so)

7. Prediction Market Adjacent Apps that are at a critical juncture

8. How to value the market opportunity here

9. Real risks that are not discussed by the permabulls

10. My expectations from a Polymarket token

DMs always open if you're building something cool in the prediction markets space. I want to try and test as many new products as possible

Prediction markets have become Web3's mainstream breakthrough.

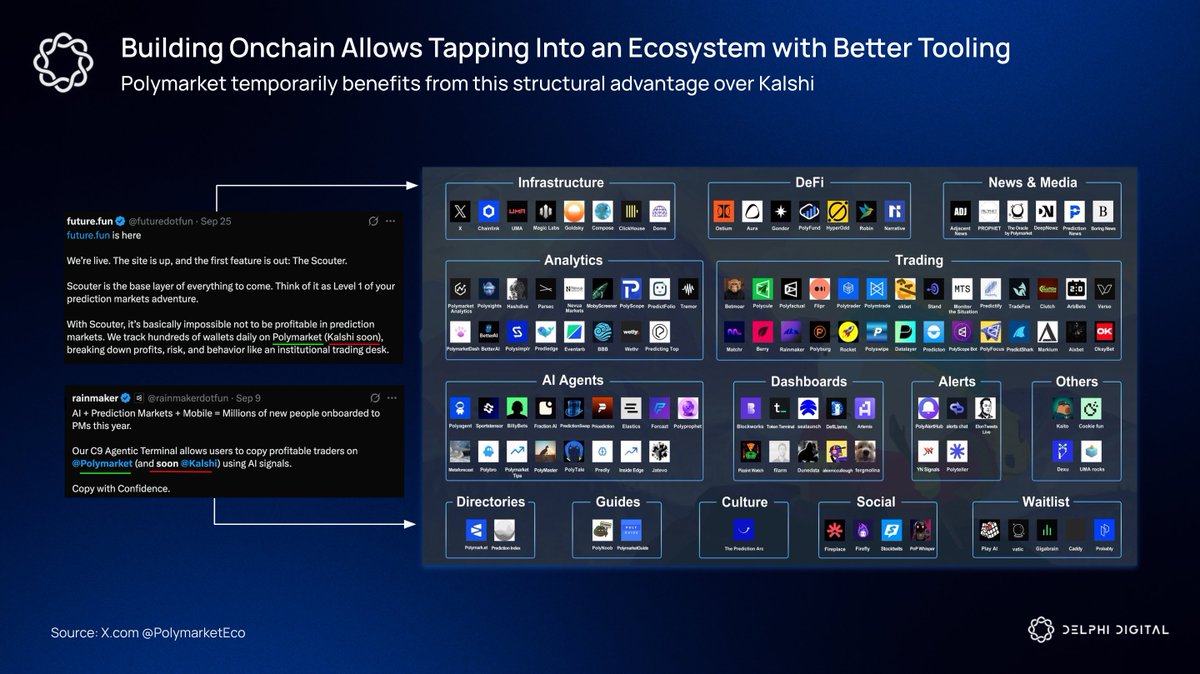

The next frontier is Prediction Market Terminals.

Professional traders need data density and execution speed more than discovery. This creates a big opportunity for professional trading terminals, mirroring the memecoin rush.

These terminals integrate multiple platforms like Polymarket and Kalshi and justify charging fees by offering a suite of key features:

Market Aggregation & Order Routing: A single interface to view odds across all major platforms and route trades to the venue with the best price and lowest fees (@tradefoxai, @fliprbot, @StandDOTtrade).

Real-Time News & Data Integration: A live feed of news, social media sentiment, and economic data integrated directly alongside the relevant markets and their impact on a trader's open positions (@VersoTrading, @betmoardotfun, @fireplacegg).

Onchain Intelligence: Tools for tracking the flow of smart money, identifying large wallet movements, and analyzing the positions of top traders (@hash_dive, @poly_data, @polyburg).

AI Assisted Market and Opportunity Discovery: Utilizing AI to augment and improve a trader's decision making process (@polyfactual, @polymtrade, @Polysights) or utilizing agents to help users passively participate in prediction markets (@polytraderAI, @rainmakerdotfun).

Advanced Risk Management and Order Types: Tools that allow users to model complex scenarios and utilize order types such as TWAPs and trailing stop losses for professional traders.

Third Party Leverage: Offering leverage on selective high volume markets with their custom liquidation engines.

These terminals serve the power users driving the most volume in prediction markets.

Our new report "State of Token Markets" is live!

Most tokens spend their lifetime below launch price.

Across 540+ tokens launched since 2020, the average token spent 70% of its life below launch.

Tokens launched at inflated FDVs with minimal float, which handed the initial pop to insiders and farmers. The typical token underperformed BTC by 7% per unlock. By the tenth unlock that underperformance had compounded to -47%.

Now the model is shifting. Hyperliquid routes 97% of protocol fees into HYPE buybacks. Uniswap voted in December to burn $600M of supply and flip its fee switch, with the burn sized to match the fees holders would have received since 2018.

But buybacks alone aren't enough. Jupiter ran a similar program but had $3.78 in unlocks for every $1 bought back. Hyperliquid has been the outlier since no insider supply was fighting the bid. Buybacks only matter when supply discipline matches them.

Revenue alone doesn't guarantee market cap growth. Pump runs one of the largest onchain buyback programs but that hasn’t translated into durable token performance.

A revenue-weighted portfolio of the top 10 protocols by revenue returned 30% since January 2025 while BTC was down 17%.

The market is now paying for real cash flow.

“HIP-4 is Polymarket on Hyperliquid, therefore Hyperliquid takes all of Polymarkets volume”

^ i think the above is often the way in which people describe and think about HIP4. While the outcome contract largely functions the same, I think the above statement wildly underestimates the retail friendliness of Polymarket. I believe that asset underlying outcome markets can see meaningful growth and be the spark to lead meaningful vault growth on Hyperliquid, but it is misguided to assume HIP4 takes meaningful marketshare in the next 12 months from Polymarket/Kalshi when it comes to sports, political, and culture markets.

HIP-4 introduces a new contract type that lets users trade discrete event outcomes alongside spot and perps on Hyperliquid. For tradfi readers, these outcome markets essentially function as binary options. My base case is that HIP-4 is incremental, and over time, one of the key pieces to meaningful vault growth as an asset manager's core trading instruments, spot, perps, and binary options, can be used at their discretion.

The market for short-dated, bounded payoffs is real, and the economics at modest market capture are meaningful in absolute terms but don't move the bottom line until we see large marketshare capture or growth.

This is not a HIP-3-style zero-to-one moment for new deployer entrants; the existing HIP-3 winners and dominant frontends are best positioned to absorb the surface area. With HIP-4 introducing a new way speculators can express a bet, I expect vaults to see significant growth over the next 12-24 months along with steady treasury yield from USDC (AQAv2) as there are now less reasons to move capital off Hyperliquid.

The cleanest investable expression remains HYPE itself, with a handful of entrants carving out a niche share in exotic markets (politics, sports).

Our new report "How Far Can Saylor Stretch It" is now live!

STRC has become the center of Strategy’s BTC accumulation model.

The question now is whether each new raise can still add BTC per share after accounting for the common issuance needed to service the preferred stack.

Strategy’s earlier BTC purchases were powered by a wide equity premium. MSTR traded far above the value of its BTC holdings which made new share issuance accretive.

At ~1.24x EV-based mNAV, that math is weaker. Common issuance sits close to the breakeven line and no longer gives Strategy the same clean path to BTC/share growth.

Convertibles were useful because buyers accepted low coupons for MSTR volatility. They also left behind $8.2B of principal and a repayment schedule that starts to matter in September 2027.

STRC now carries more of the load. It gives Strategy access to yield buyers underwriting an 11.5% annual dividend paid monthly, rather than MSTR equity upside. The proceeds can keep flowing into BTC without adding another convert maturity.

The tradeoff is the recurring claim STRC creates. Each raise adds Bitcoin today and another dividend obligation tomorrow. If BTC rises and MSTR’s premium holds, the structure can absorb that cost. If BTC chops sideways, the obligation stack grows while common issuance becomes less efficient.

The stress case is whether STRC-funded BTC purchases can keep outrunning the common issuance needed to service the preferred stack. Strategy’s $2.25B dollar reserve can handle the ~$1B September 2027 put. This buys time but the larger 2028 wall still needs an answer.

The next boundary is the $28.3B STRC authorization cap. Before the cap, STRC can keep adding BTC and offsetting dividend-related dilution.

Without an extension to STRC issuance capacity, reaching the cap means the BTC-buying offset can slow or stop while the dividend obligation remains.

ZEC holders are the funniest lol

They'll be the loudest to announce they have "private" money

Yes the point of private money is to let eveyone and their mom know that you have assets in a private SOV

@coinbase was out here preaching “Just Coin It” and tokenize everything except token holder rights.

Acquihired the

1. https://t.co/IEV6uAmKey team ($TNSR holders got absolutely nada) 2. Iron Fish core devs ($IRON holders left bagholding the protocol)

Maybe they haven't been acting for the industry's best interests for a while - few people want to call them out

BREAKING: Nvidia and PulteGroup are partnering with startup Span to install mini data centers on the walls of new homes

Each unit packs 16 Nvidia Blackwell GPUs, 4 AMD EPYC CPUs, and 3TB of RAM - and taps unused home electrical capacity to run AI inference workloads

@JupiterExchange really needs to get their perps product in competitive shape or they're going to lose the sector that drives the majority of their protocol revenue