VC Investor | Founder & CEO @ 13ThrustVal Group - Global Private Equity Led Multi-Asset Mgmt & Capital Group | 3 Companies& Offices Across 7 Different Countries

13ThrustVal Economic Advancement Council is a high-level global council where global leaders, royal families, government policymakers, global titans, dynastic principals, economists, industry leaders, and powerful elites from around the world come together to contribute toward economic advancement, strengthen financial system transformation, and help enable growth opportunities across both private and public markets.

@myHQSpace It's great chance for any Founder to Sue MYHQ on their internal unethical Activities

They don't refund the amount snd marks in the app status refunded.

WakeUp Ruthless Founders to use it for Interest.

Sue for min $12 million

#founders#Founder#startupecosystem

@myHQSpace It's great chance for any Founder to Sue MYHQ on their internal unethical Activities

They don't refund the amount snd marks in the app status refunded.

WakeUp Ruthless Founders to use it for Interest.

Sue for min $12 million

#founders#Founder#startupecosystem

Most Expensive Wars in US History (inflation-adjusted)

⚔️ WW2 — $4.7 trillion

⚔️ WW1 — $582 billion

⚔️ Vietnam — $844 billion

⚔️ Korea — $341 billion

⚔️ Iraq War — $2.4 trillion

⚔️ Afghanistan — $2.3 trillion

⚔️ Gulf War (1991) — $116 billion

America has spent $14 trillion+ on wars since 1917.

That's more than the entire GDP of every country except the US and China. 💸

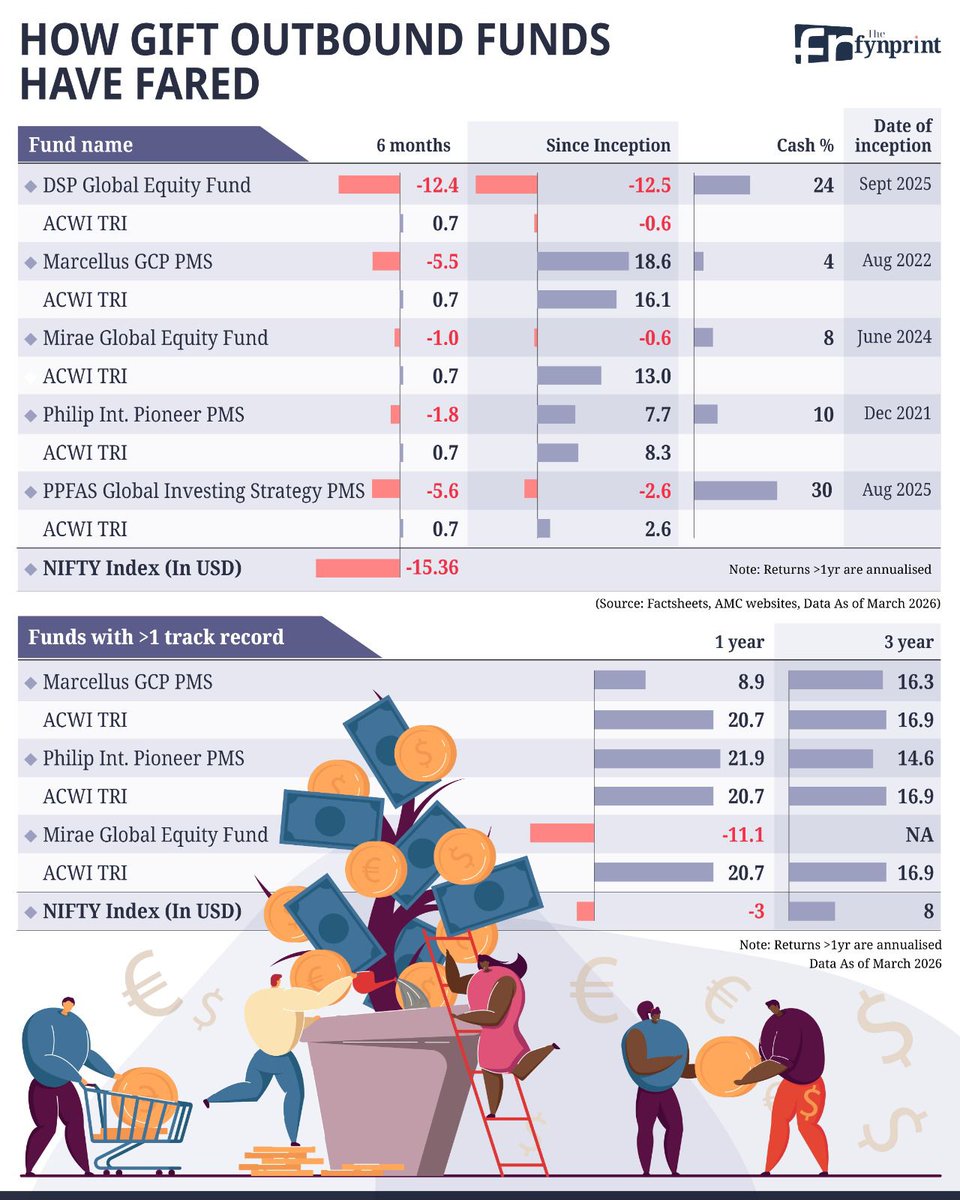

GIFT City's active global funds are off to a rough start — and the data is hard to ignore. 🧵

1/ Every single active fund in GIFT is negative over the last 6 months. DSP Global Equity: -12.4%. PPFAS PMS Global Strategy: -5.6%. Marcellus GCP: -5.5%. Meanwhile, ACWI TRI was +0.7%. That's not a small miss. That's a different direction entirely.

2/ The "Since Inception" picture isn't prettier. DSP is -12.5% since Sept 2025. PPFAS is -2.6% since Aug 2025. The only funds with positive since-inception returns (Marcellus at 18.6%, Philip Int. at 7.7%) have multi-year head starts — and even they lagged ACWI TRI over 1 year.

3/ On a 1-year basis, Marcellus returned 8.9% vs ACWI TRI's 20.7%. Philip Int. Pioneer returned 21.9% — one of the few bright spots. Mirae? -11.1% vs benchmark's +20.7%. Brutal.

4/ Now let's talk tax. GIFT funds are structured as Category III AIFs. They pay tax at the fund level — ~42% STCG & 14.95% LTCG vs slab rate or 12.5% for an individual.

5/ If you instead bought a UCITS ETF (say, an Ireland-domiciled S&P 500 or ACWI fund) directly via the LRS route, capital gains tax kicks in only when YOU sell — and at your applicable slab rate or 12.5% for long-term. The fund itself pays zero Indian tax.

6/ So with GIFT active funds you get: ❌ Active underperformance vs benchmark ❌ Possible cash drag ❌ Fund-level tax leakage you can't control

7/ With a direct UCITS ETF investment: ✅ Near-zero tracking error to the index ✅ No fund-level tax — you control timing ✅ Lower cost, higher transparency

8/ The case for passive international investing has never been clearer. If GIFT funds can't beat ACWI TRI in a falling market (when stock-picking supposedly shines), when exactly will they?

Story by @PosteAnil

https://t.co/rD6Qdy1KOh

"Warm intros lead to 13x higher chance of funding than cold emails"

Not exactly.

The 13x number comes from a UK study from 2017.

But there’s one important nuance.

Anyone can email a VC, but not everyone can get an intro. So intros aren’t just a sourcing function, they’re also a screening function.

Because of that, a lot of "bad" founders end up in the cold email pool, which naturally lowers the average success rate of cold emails as a channel.

But if you look at it for a given founder, the difference is likely much smaller than 13x!

Put another way: only the "best" founders get intros, so intros have a higher success rate not just because they’re a better channel, but because the average founder quality is higher.

Of course, intros do work better than cold emails.

Just not by 13x.

That number is mostly a statistical artifact.

NB: "Good" founders have traction + track record. Bad founders have none. No judgement here. We all start as "bad" founders, and some become "good". :)

Really cool!

"PLAID: Product-Level AI-Derived Indicators Databasefor International Trade" by Carsten Brockhaus, Julian Hinz, and Irene Iodice.

"We introduce PLAID (Product-Level AI-Derived Indicators Database), an open, versioned data-base of product-level indicators for international trade, generated by an ensemble of frontier large language models (LLMs). The current beta covers six indicators at the HS 6-digit level across all major HS revisions since 1992: (i) the Rauch classification of goods into organized-exchange, reference-priced, and differentiated products; (ii) UN Broad Economic Categories (capital, inter-mediate, consumption); (iii) economic perishability on a five-class scale; (iv) a hazardous-materials flag; (v) microchip/semiconductor content; and (vi) 3TG conflict-mineral content. We validate each indicator against established external benchmarks and demonstrate its empirical relevance through a targeted gravity application. PLAID is designed to grow: future releases will add indicators for technology intensity, R&D intensity, regulatory sensitivity, and other product attributes. All data and code are publicly available."

Working paper:

https://t.co/onHzeZ0sQN

Product-Level AI-Derived Indicators Database for International Trade:

https://t.co/44n5OasSj9

AI is entering an unexpected conversation around demographics.

Falling fertility and aging populations are already straining economic systems, and AI could either offset the impact through productivity gains or deepen inequalities if benefits are uneven.

The question is broader than technology. It is about whether AI can help sustain growth when the population no longer does.

https://t.co/aJWphv1nmQ

Private equity is entering a new era where value creation is shaped by two powerful forces: rising expectations around climate action and the accelerating impact of artificial intelligence. Find out more - sign up for our webinar series: https://t.co/K7nOTJeeXe #PrivateEquity

🇺🇸🇮🇷 THE DEADLINE NOBODY'S WATCHING: MAY 15 ⏰

Markets priced Friday as "conflict over." EUR IG rallied to 91bp — 1bp from "All Clear."

But there's a hard deadline in 26 days that changes everything 👇

The Timeline:

• Today: April 19 📅

• May 15: OECD crude hits **operational minimums**

• Oil shipping time: 20-45 days 🚢

Do the math.

Even if Hormuz FULLY reopens Monday, tankers leaving today won't reach Europe until mid-May.

**The inventory crisis is ALREADY baked in.** ⛽

What "Operational Minimums" Means:

This isn't "low inventories." This is where:

• Refineries shut capacity 🏭

• Strategic reserves tapped (again) 🛢️

• Rationing enters policy talks 🚨

• Price moves go NON-LINEAR 📈

And rebuilding takes MONTHS, not weeks.

The Blockade Problem:

Trump Friday: "Naval blockade remains in full force... until our transaction with Iran is 100% complete."

Translation:

• Shipping disruptions continue

• Insurance costs stay high 💸

• Transit times stretched

"Most points negotiated" ≠ signed. ✍️

The Market Disconnect:

Brent: Still $20 ABOVE pre-conflict ⚽

EUR IG: 91bp (pricing conflict resolved)

One is right. One is pricing hope.

The 2022 Playbook:

Feb 2022: EUR IG at 90bp

Feb 24: Russia invades

Weeks later: 160bp

Pattern: Markets priced stability until it broke. Then repriced VIOLENTLY.

This time we have a visible deadline (May 15) and quantifiable trigger. Yet EUR IG sits 1bp from "All Clear."

Even if signatures happen Monday, oil won't flow fast enough to avoid May 15 stress.

Inventory stress → policy response → economic impact → credit widening

The asymmetry can be brutal:

• Perfect deal: EUR IG tightens maybe -5bp to 86bp

• Drags past May 15: Looking at 130bp+ as emergency measures kick in

26 days. That's the window. ⏳

#EnergyMarkets #CreditMarkets #Iran

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Day twenty-five: Cloudflare $NET

Peak share price: $253.3 (Oct 31, 2025)

Share price today: $200.99 (-21%)

EV today: $70.2bn

ARR today: $2.46bn (+34% Y/y

NRR: 120%

EV/ARR: 28.5x

GAAP Operating Margin: 6.2%

EV/Run-rate GAAP EBIT: 453x

Headcount: 5,200 (+21% Y/y)

What Cloudflare does:

Cloudflare operates an edge network that it uses to provide an array of value-added connectivity, CDN, and security services to customers worldwide.

Its core business, application services, is built on upsells on top of its free CDN offering, which undercut the low-end of the paid CDN market and became an onramp to cross-selling higher value security services( WAF, DDoS mitigation, bot management, etc.

It then built and executed on an impressive second act, moving into enterprise access with a SASE business model that replaces corporate VPNs and firewalls with cloud native security.

Finally, Cloudflare uses the same infrastructure to run a developer platform, offering serverless compute (Wokers), object storage (R2), and more at the edge as a sort of distributed, developer-native alternative to traditional hyperscalers.

The company hasn't disclosed much on the relative sizes of these businesses, but its strength in enterprise customers and expanding net retention rate suggest that it is seeing significant success in the latter two businesses.

AI bear case:

This is less of an AI-specific bear case (those are hard to build), but Cloudflare's second-act businesses both face heavy competition from existing cybersecurity (Zscaler/Palo Alto) and hyperscaler (AWS, GCP, Azure) incumbents with substantially larger capex and go-to-market budgets.

On the AI side, perhaps most worrisome is the idea that provisioning of AI infrastructure might become the purview of the model vendors (OpenAI/Anthropic) who leverage their capabilities and the ubiquity of their APIs to ensure that inference compute happens on their backends, not Cloudflare's edge servers.

AI bull case:

The AI bull case for Cloudflare is pretty crisp (and arguably reflected in the multiple and metrics). Cloudflare occupies an increasingly strategic position between users and web content, and as agents proliferate, the types of security that Cloudflare specializes in (especially advanced bot detection) become increasingly critical.

Beyond that, there ARE AI workloads that likely belong at the edge, and in general enterprise security challenges will compound as agents come to the fore.

Finally, Cloudflare has done a surprisingly good job of maintaining its developer-first ethos (I use R2 for some of my projects!), giving it valuable exposure to the broader vibe-coding trend.

In short, Cloudflare has a history of executing well and beachfront real-estate from which to add value in an AI native world.

AI traction:

Cloudflare has seen a material acceleration in growth of late, with revenue growth increasing from 27% in Q1 to 34% Y/y in Q4, driven by increased net expansion, particularly with large customers.

The company doesn't disclose any AI-specific revenue (and indeed, is stingy on revenue breakouts for any segments), but it seems safe to assume that AI is showing up as a tailwind in the business one way or another. One of the most plausible candidates is heavy use of Cloudflare's Workers product by vibecoding customers (both developers and applications).

Strikingly, the company called out that the number of weekly agent-made requests on its platform doubled in the month of January alone (!!), highlighting the intensity of the usage tailwind.

Adjacent AI-native startup summary:

Though not fully AI native, @vercel is the most relevant competitor to the core CDN business (912 employees, +28% Y/y), and clearly executing well.

On the enterprise security side- ZScaler, Netskope and Palo Alto are the companies to watch, although all relatively mature. @Tailscale (315 employees, +68% Y/y) competes with Cloudflare's WARP and Tunnel products at the low end.

On the dev-tooling side, the competition is fierce, with @vercel showing up again along with a host of other inference platforms running from the low end to enterprise. It's hard to specify competitors given the breadth of Cloudflare's offering and the particular wedge it brings (a massive, highly optimized edge network).

Management Quotes:

"We blew away our previous record for new ACV in the quarter, with strong year-over-year and quarter-over-quarter acceleration. In Q4, new ACV book grew nearly 50% year-over-year, making it not only a record quarter in absolute ACV dollars but also the fastest growth rate we've delivered since 2021."

"A leading AI company expanded their relationship with Cloudflare, signing a 2-year $85 million pool of funds contract for our full platform, selecting Cloudflare as their single long-term infrastructure provider with 100% traffic allocation."

"A U.S. media company signed a 3-year $3.1 million contract for AI Crawl Control, along with application services and Workers. This customer was facing a massive increase in AI scraping, which was crushing their network and driving up infrastructure costs. They chose Cloudflare to gain visibility into which AI models are consuming their data, allowing them to protect and eventually monetize their unique content."

"That means we win when AI applications are built on Cloudflare Workers, but we also win just from the increased usage of all of our products and agentic Internet drives."

"It's not a coincidence that most so-called vibe coding platforms are either built on Cloudflare Workers or have us as their preferred deployment target. We exited 2025 with more than 4.5 million human developers active on our platform. It's a lot more if we count their agents."

Commentary:

No comment on Cloudflare would be complete without reference to the company's sky-high valuation multiple. At 28.5x sales only Palantir is higher, and the next highest in SaaS in CrowdStrike at 19.7x with another cliff down to Palo Alto at 12.7x. This is a very, very expensive stock and while the metrics are truly impressive (and more importantly, trending the right direction) it's strike that they aren't yet standout on an absolute basis (other companies have similar/higher growth rates and similar net retention, yet trade at a massive discount). The market clearly believes that Cloudflare is a secular AI winner- and yes, it does have good reason to believe so.

The biggest challenge to writing about Cloudflare's AI tailwinds more specifically is the inscrutability of the business given the range of business lines and market segments served. The company's investor day on June 9th will hopefully provide some helpful context.

What seems true is that AI is a meaningful tailwind for Cloudflare's business, although there is no one hero SKU to point to and analyze. Still, taking the sky high, top-in-all-of-SaaS multiple aside, it is hard to argue against a well-oiled machine with a stellar management team that occupies beachfront AI real estate. It will be interesting to see if/how the story evolves into something more legible (and quantifiable) for investors over time.

The best of GitHub Constellation India

- AI agents for developers

- What's new in GitHub Copilot

- The future of software development

👉 Watch the highlights on YouTube

Let’s see how this ages.

“Private Credit Is Not a Financial Crisis in the Making”

The article acknowledges the risks, but claims the losses will be more easily absorbed.

“.. The problem raising concerns today is that private credit lenders are willing to extend enormous amounts of money — a billion dollars is not unheard of — much more quickly than a bank would.

And they are levered up themselves, often borrowing half the money they lend out from banks.

To make things worse, the notes in private credit deals are highly illiquid and closely held, which means there’s precious little price discovery in the market, and it’s extremely hard to mark to market, know how much the loans are worth, or be able to discern systemic risks before they become a crisis.

The cherry on top: Borrowers in this market are primarily much maligned private equity companies, who are notorious, fairly or not, for overleveraging their portfolio companies, taking out enormous dividends and then leaving them for dead.

From a distance, they’re not all that different from the financial innovators who blew up the world in 2008…”

https://t.co/8EZ8Ghl6xm

🛢️The Crude Oil Industry: Every Company, Every Segment, Every Dollar at Stake.

subscribe to my newsletter, link in my bio , for deeper analysis and research on the best stock in this industry... some of them are already there