@TCII_Blog There’s some point where the argument “we’ll keep a war chest of cash and be patient until opportunities arise” fails. I was on board when cash was $200B, but $380B is far beyond reasonable. Their three largest investments ever were in the $30B range (BNSF, Apple, PCP).

Two years later and the cash pile has nearly doubled to $380B.

I don’t care that’s it’s Berkshire Hathaway, hoarding $380B is bad stewardship and unacceptable.

$BRK.A $BRK.B

Berkshire is my largest holding but I am struggling to see the wisdom in holding $200B of cash and hoping that some massive acquisition or two comes along… is that clearly better than repurchasing shares with a little bit less price-sensitivity? $BRK

If you buy $STNE today, you’ll get a $2.53 special dividend on May 4 AND a business that could earn $2.25 of EPS in 2026 and $2.50 in 2027 based on management guidance.

Stock is under $15.

@andrewcoye@SteveWps Agreed, at this size I believe shareholders would much better off if they followed a “consistently repurchase at any price” strategy like Apple

@ValleyFallsRI I don’t know. I think another contributor is that they’ve opened a lot of new locations and year 2 sales at a new location are typically lower than the year 1 “honeymoon” period.

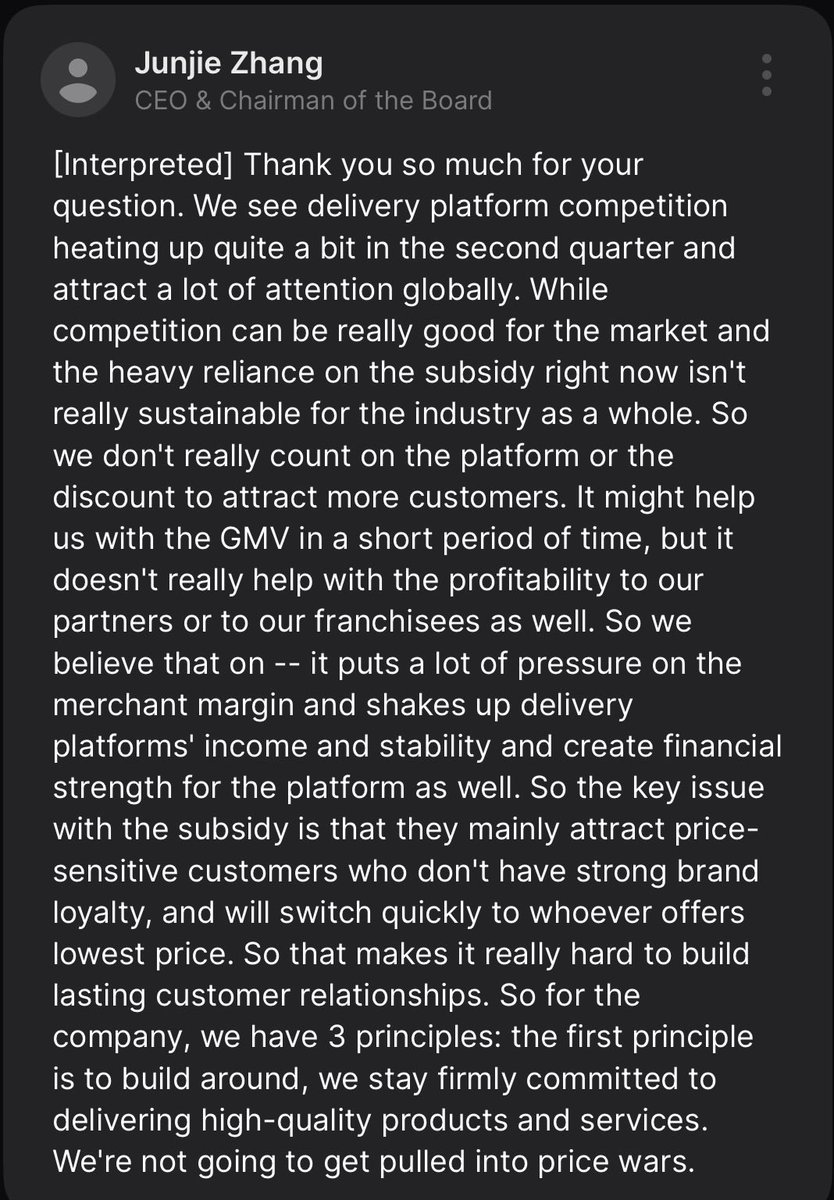

@ValleyFallsRI Terrible for sure, but partially because they’ve refused to participate in the delivery subsidy war. Is it possible that earnings are near a trough? If so, stock is trading at 3x EV / trough EBIT with more than half of today’s market cap in cash as downside protection.