Ultra long-term investor tweeting about stocks and investment philosophies that may benefit you. Subscribe to my Patreon for real-time investment disclosures.

Whirlpool's debt load has led to underinvestment and competitive loss for its core appliances, suspension of dividend, and adoption of lobbying for tariffs as strategy.

Remember this as you encounter article after article grumbling about size of Berkshire Hathaway's war chest.

What gets me is when certain investors pout over the $380+ billion cash position and ... buy a stock with tens of billions in debt instead.

They forget that owning Berkshire consists of owning assets that, by definition, are so great they create the extreme surplus.

I’ve been working and investing in financial markets since the 90s and in every full cycle I’ve seen, Berkshire Hathaway (and Buffett) are ridiculed during the most extreme end stage of each cycle, then celebrated for their discipline and focus when they buy at generational lows while everyone else is either bankrupt or getting bailouts.

This time is no different. 👇🏼

During the Berkshire meeting, Greg Abel was directly comparing Burlington Northern Santa Fe's railroad operations to specific other large railroads. This was a very common corporate management way of communicating decades ago. Now, you almost never see it. The best competitors tend to be those who embrace rather than obfuscate objective measurements.

Coca-Cola $KO up quite a bit on strong earnings. This lifts up the value of all those dividends reinvested over the years. If the current price holds, Coca-Cola will have been a 10% annual compounder over the past 15 years.

There are three stocks I am currently buying (one stock has been growing earnings at a 62% annual rate). To become a subscriber and access, click here: https://t.co/yN6qIFbsbO

John Deere $DE has paid out over $40,000 in dividends over the past 30 years for every $10,000 invested. This also came with $600,000 in capital appreciation. Don't let those "only 1%" starting dividend yields fool you.

Price of Berkshire Hathaway stock $BRK.B during March 4th buyback, conducted at (in management's opinion) conservatively estimated intrinsic value: $487-$490.

Price of Berkshire Hathaway stock now: $468.

Very odd if speculative reporting is true that *all* of Todd Combs' picks at Berkshire Hathaway $BRK.B are being discarded by Greg Abel. Sure, get rid of SiriusXM $SIRI, but no need to discard Amazon $AMZN when you have $370+ billion in cash. Seems a bit personal (not rational).

Last May, when Berkshire $BRK.B hit $539, many shareholders remarked that the price was a bit high. Now that the stock is down 11% with another year of enormous profits under its belt, many shareholders are noting the price is reasonable. By far, most rational shareholder base.

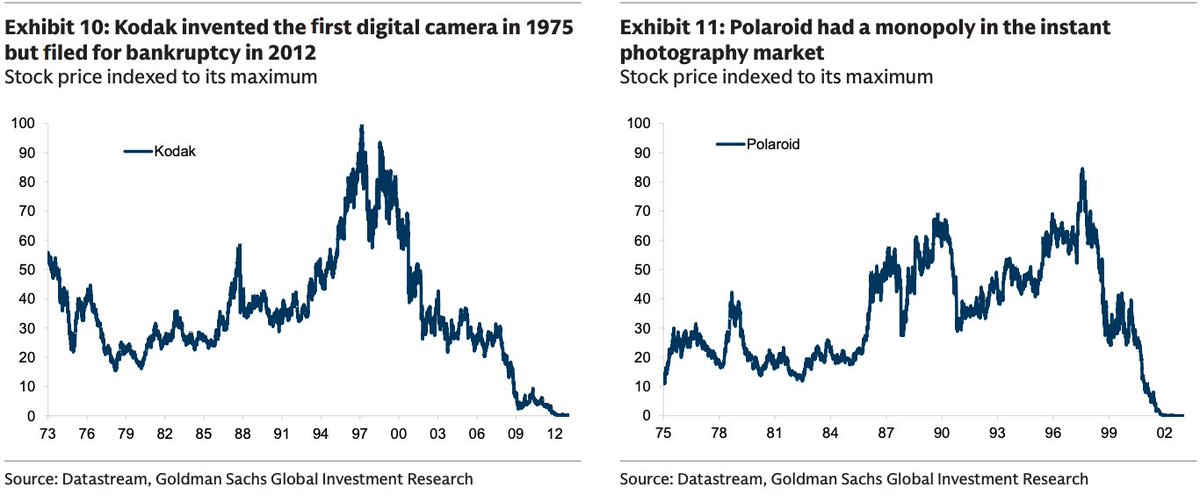

My optimistic opinion on this: Only 19 of the largest 500 companies in 1975 have gone bankrupt since then. And even 1975 Kodak shareholders got shares of Eastman Chemical $EMN spun off in 1993, such that $10k in 1975 Kodak would be worth $125k today in Eastman Chemical shares and $0 in Kodak, i.e. even the bankrupt case contains 12.5x returns for shareholders.

Some people need to be taught to buy 30 dividend growth stocks to hold forever, pool the dividends for the first three months to pay to Uncle Sam as a front-loaded estimated tax payment, and then set the dividends from April - December to be payable to their checking account so they can be constantly hit with ~10 dividend checks per month that grow annually faster than inflation. Owning is a better way to live than gambling.

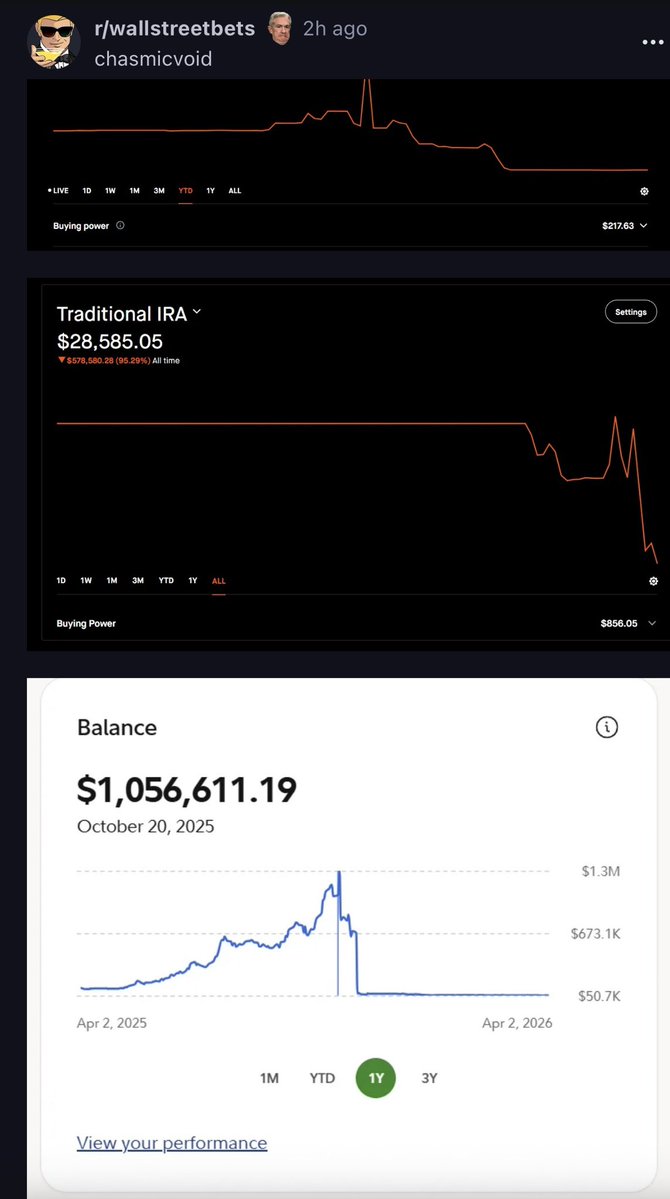

The most viral story on $RDDT right now:

-> Guy started with $300,000

-> Gets lucky with individual names at April 2025 bottom

-> Runs it up to $3,000,000 and claims they had financial freedom

-> Proceeds to do 0DTE options on $SPY

-> Turned $3M -> $50k.

Usually I give a lesson learned type story but this is just stupid?

Legit stop touching 0dte options.

Even if they full ported it into Jim Cramer’s favorite stock $MRVL, probably would have been $6M in 2-3 years.

The best lesson of generational wealth is looking at Nancy Pelosi.

If you do options, look at how their on $AVGO to $NVDA keep compounding over time.

Not one day windows.

For those that initiated a position in Coca-Cola $KO in 1994 right after Berkshire Hathaway finished buying the stock, today's dividend marks $3,000 in cumulative dividends collected for every $1,000 invested. The dividend growth marches on.

The credit rating agencies made a mistake stripping Berkshire Hathaway $BRK.B of its AAA rating in 2009-2010, and it has been an ongoing error of misplaced pride that they have not restored Berkshire to AAA status at any point on the company's road to $370+ billion in cash.

There is one stock in particular (among several) that I am purchasing now at today's compelling valuation. To access and subscribe to my latest post on what I am buying now, click here: https://t.co/1biJg5JDhE

Disappointed to see the Berkshire Hathaway $BRK.B meeting Q&A has been reduced to two sessions of slightly more than an hour. I hope to be wrong, but I sense a new era of sparse insight from management.

I think Buffett and Munger, and now Abel, have regarded true actionable information and knowledge as proprietary and something to be confidential. Which is why the most insightful responses from Buffett and Munger tended to be non-Berkshire specific "good financial life and informed citizen economically" type commentary, which I do not think Abel wants to provide. Abel regards the general financial educator role as outside his scope.