$SOFI... -8%, let's see how it trades b/c this was a crazy good Q. Obviously I'm p*ssed, but at the same time, the bears do this sh*t...

Let's go through the Q.

Rev + 43%, Net Inc + 134% EBITDA + 62%

BV of $8.44, TBV of $7.21

Really? Are we really trading this down to 2x BV in line with $JPM, but growing Net Inc like 12x faster?

And before we try to front like that's not relevant, realize this: Every other bank (except maybe $BK) is making that high teens/20s growth this quarter and growing net income only 5-25% of $SOFI via Investment banking. $SOFI's doing it with just straight boring commercial banking growth.

Oh... and in the Q&A... in case there is ANY confusion $SOFI's goosing the growth numbers, the EBITDA growth (which matters more than net income b/c $SOFI is still an early stage company and also implies net income is also clean), that's net of marketing expense. That's not even how other folks present the number, btw...

That's why when folks pretend $SOFi doesn't disrupt banking, I'm like... in what world is that true? Look at these numbers. What is it you think is happening here in these financial statements?

How good was it?

BTW... the bears want to pretend that something is going on with Credit Quality and so equity is understated in some way (aka ROE), but are you F-in kidding me.

Clearly, with TBV up 63%, that net income is most def hitting Retained Earnings (aka how you get TBV up that much). In other words, that's BS, right.. we can agree that's how you read that, right?

Let's talk about Book Value

Oh, and BTW, BV is one of the metrics that more traditional folks like me will look at. AND MOST DEF will tell you if the capital raise was worth it. You basically raised $3b in Equity capital through secondaries ($1.5 July 25, $1.5 Dec 25). And at this point, not even a year later, you have $4.2b more in Book Value (so $4.2-$3b, $1.2b addition Equity Capital).

What's that mean? Plenty of Capital to continue to fuel growth. By plenty, I mean $1.2B more in addition to the $3b capital raise.

Strong Despite the Macro

Yup. that's straight cash, kids. And realize that "in theory," this isn't yet a truly good market for $SOFI. A "Good Market" would be the world calming down and rates declining at a chill place, with the whole curve shifting downward vs this weird twisty steepening we're getting. That would drive a macro refi boom in Mortgages, HELOCs, etc. And this would substantially change the balance sheet.

Crazy Strong Loan Growth

But then let's look at the mortgage growth (image below). A few comments for the newbies learning to infer this. You have Mortgage growth up 137% with average balance down 11%. What's that mean? It means unlike every other bank which had flat to single digit mortgage growth, $SOFI made loans, aka took share. AND ALSO, these ARE NOT risky loans.

If anything, given the size difference from previous year, this book is less risky. AND also, the volume (aka count of customers) of 137% is likely higher.

And they talked about the demand for loans despite the weirdness in the long end of the yield curve being strong. And that matters b/c if you can finally get this stupid yield curve shifting downwards vs just steepening, the low-hanging fruit of HELOCs is just refinancing the student loan book. Call it what it is. Those are high-credit-rating older GenZ's, younger millennials who have been out of university now for a while and likely are home buyers.

What about the Tech Platform?

Ya'll know I differ from everyone else b/c I could give a farthing (insert other F word) about the tech platform. The nature of tech-heavy FinTechs always involves a ton of CapEx, depressed earnings because of it, and, quite frankly, in the coming macro environment, you can likely buy a smaller Fintech at a discount from some broke start-up that's going belly up due to lack of clients and earnings.

So yeah, TBH, I'm not sure why ya'll care so much when the internal use of that platform grew EBITDA 64%. But whatev's.

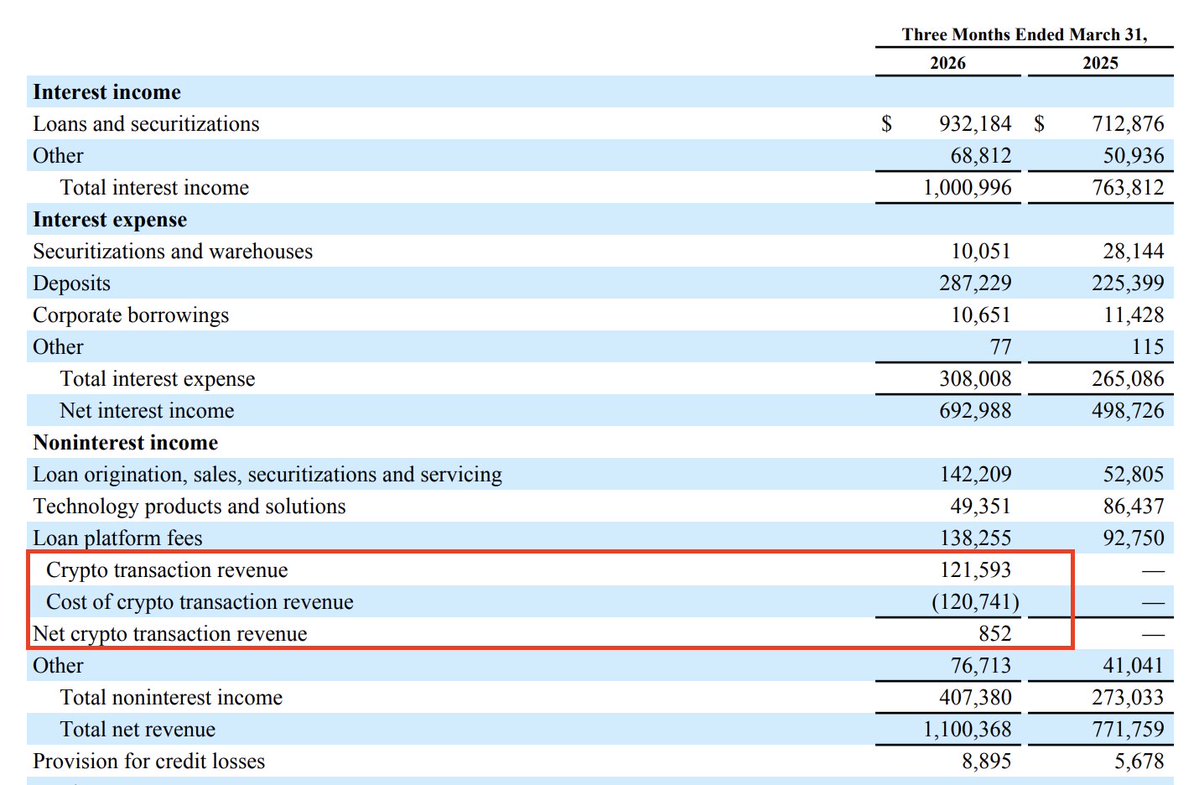

What about Crypto

I do want to show the Crypto biz. Notice. It takes a lot of cash right now. That might change in the future. We shall see. That's yet another reason why I think you fortify Book Value with the additional $4.2 b of capital.

And here I differ from others, too. I think $SOFI's most wild card value is this stablecoin biz, not because of payments or because a bunch of crypto bro's want to pound their chest like a bunch of apes on the end of America, but because the most PROFITABLE THING stable coin allows for is an off-ramp.

And it occurs to me that a bunch of you will nod your head but have NO IDEA what I mean. So let's talk about it.

Let's say you're some dude from UAE who's got a ton of crypto assets (not that far-fetched). You wanna buy a bunch of real assets (real estate) in the US. You gotta figure out for yourself... how do I get my crypto into USD so I can buy real assets on the cheap in the US? That's what stablecoin is really for. Not the nonsense $5 toothpaste you bought from Walmart.

Right now, at $124mm that's on the small side for an off-ramp, given the size of money I'm thinking is possible. But it doesn't have to be.

And we know Mr. Noto had zero dollars last year, and this year he's got $124mm now.

And guess what lovelies... that's why it's such an interesting biz, esp in the context of offering it across to other banks. Whether most of it is with $SOFi and it helps grow the asset management biz or it facilites money coming into the US, I care. It's part of why even if I didn't own one share (which obvious I'm long) I would STILL watch $SOFI.

Other

1) NIM is down barely. Why Barely? B/c funding mix is more or less compensating for it. And you can do that for 2 reasons:

a) Your debt isn't warehouse financed anymore. Even with their higher-than-market bank accounts, those deposits are still a cheaper form of funding.

b) B/c you were offering so much more than everyone else on deposits last year, your funding cost is still is lower yoy despite that you are offering less to folks who have deposits at $SOFI.

2) Financial Services Segment growing 41%. Cool, but even that crazy number is less significant than everything else I mentioned. Plus b/c hte yield curve is all over the place yoy, it cosmetically looks like lower margins.

3) Credit Quality is just fine/slightly better NCO's. Even though you have higher Provision for Credit Losses, you also have massive loans that were originated. Overall, though you have lower NCO's. That implies that once we finally do get lower rates, $SOFI can still release reserves just like everybody else. (aka more liquidity if we shift to a good market.

Conclusion

There is nothing more thankless than being a $SOFI investor, and quite frankly, I wish you would do a 4pm EST call so I could go get a drink right now. Instead, I gotta watch how the day traders beat up my poor stock all morning, fully caffeinated.

No change to my views. Happy Wednesday. If you actually made it this far in my post, drop me a comment... maybe some kind words as I cry in my coffee about how mean the bears & day traders are....

This 1992 lecture at MIT from Steve Jobs will teach you more about product and sales than most 2 year MBA programs

Crazy just how ahead of his time this man truly was

So you are saying $NIO is turning the profit corner exactly at the same spot in time, where $TSLA historically did - and might follow their trajectory?

Too funny, I had to borrow the chart of the NIO shorts for this one, as it now works against them.

📣SoFi keeps breaking records! In Q3, we delivered record adjusted net revenue driven by all-time highs in new members, new products, and fee-based revenue.

For more details, visit: https://t.co/qZYKyHe4SC