This article is extremely bullish for Sivers. $SIVE 👀

The entire AI optics stack ultimately depends on one unavoidable reality: silicon can process light, but it cannot efficiently generate it. That makes high-performance InP laser sources a critical bottleneck for 1.6T optics, CPO and Optical I/O.

With its DFB laser arrays, partnerships with GlobalFoundries $GFS, Jabil $JBL, O-Net and WIN Semiconductors, Sivers is not merely exposed to the AI optics boom it is targeting one of the most essential and hardest-to-scale components in the entire value chain.

AI compute cannot scale without optical connectivity. Optical connectivity cannot scale without reliable light sources. And Sivers is building those light sources.

Why did I even get interested in $IQE?

When the entire market went absolutely crazy over $AXTI - I was swallowing the bitter pill of being late to that specific party.

But since I hate losing, I immediately started asking myself: what is next?

I always try to look one step ahead.

That is exactly how I managed to get early into names like $IQE or $LPKF and others before the masses caught on.

But back to $IQE - why this specific company?

The global frenzy and massive demand for optical lasers are just getting started.

The market quickly realized that Indium Phosphide (InP) - the core substrate material - does not just fall from the sky.

Hence, the massive explosive run on $AXTI.

But a raw InP wafer by itself is practically useless for high-performance photonics.

You have to actually do something with it before it can become a functioning laser.

Epitaxy.

Epitaxy is the atomic-scale deposition of crystal layers onto that substrate.

Only a handful of companies globally possess the highly specialized MOCVD and MBE machinery required for this advanced process.

One company listed on the London Stock Exchange owns a significantly larger fleet of these reactors than almost anyone else, giving them a massive structural scale advantage.

Say hello to $IQE.

Look at the pure-play competition for epi-wafers. Landmark Optoelectronics possesses far fewer machines, yet because it sits on a different exchange (Taiwan), it historically traded at multiples that make IQE look like an absolute deep-value steal.

And if you want proof of their technological moat:

IQE was just confirmed as the second largest patent filer in the entire UK for semiconductor devices.

This isn't a speculative small-cap; it’s an IP powerhouse.

Now, to be completely fair, IQE had a dark cloud hanging over it.

The cyclical semiconductor downturn cut their 2025 revenue to £97m, and because chip fabs have massive fixed costs, underutilization completely crushed their near-term margins.

Worse, geopolitical tensions flared as China introduced strict export controls on critical raw materials like Gallium and Antimony.

If you check most standard financial screeners today, that ugly debt and supply-chain risk warning still pop up.

But the market is looking backward.

First, IQE completely neutralized the China risk by successfully recycling 100% of their Gallium Arsenide and Indium Phosphide wafer waste directly back into ultra-pure raw materials for their production lines.

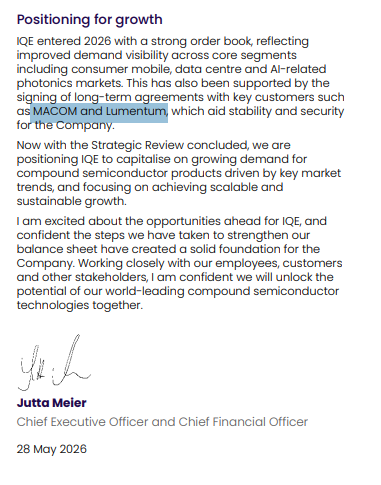

Second, on May 28, 2026 - the ultimate balance sheet reset happened.

IQE officially completed a transformational £81 million strategic recapitalization package.

MACOM Technology Solutions ($MTSI) stepped up to anchor the deal - injecting £30m in direct equity and £15m in new convertible notes to secure a ~15% strategic stake.

Existing institutional notes were swapped into equity, and the old HSBC bank debt was entirely wiped out.

The balance sheet is clean. The financial risk is gone.

So, who is MACOM and why does this partnership matter?

MACOM is a heavyweight in high-performance semiconductor products for Data Centers, Aerospace, and Defense.

They design the brains - the optical components and ICs that power next-generation networks.

By deeply aligning with IQE, MACOM secures a stable Western supply chain for advanced epi-wafers.

For IQE, it guarantees immediate structural volume demand to fill those empty reactors and unlock massive operating leverage.

And the momentum shift is already visible.

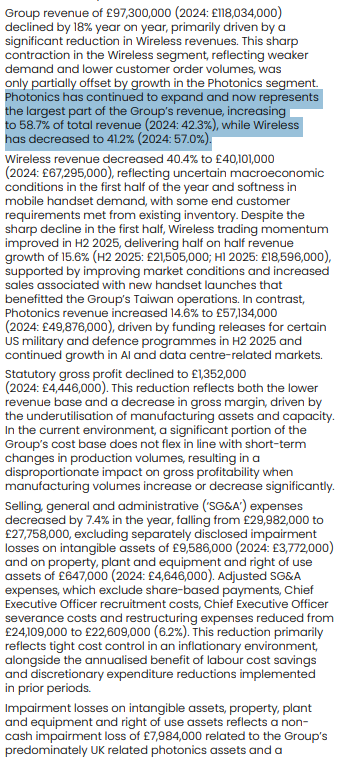

Photonics has officially overtaken wireless to become IQE’s largest segment (58.7% of revenue), propelled by surging AI data center demand and immediate US military and defense funding releases.

Think that is all?

We got another massive confirmation of their turnaround strategy.

IQE followed this up by solidifying their multi-year agreement with Tower Semiconductor ($TSEM).

Together, they are scaling Silicon Photonics (SiPh) via the heterogeneous integration of IQE’s advanced epitaxy layers directly onto Tower’s silicon wafers.

This allows them to build optical transceivers that handle the insane data transfer speeds required by modern AI architectures.

The pieces of the puzzle are coming together perfectly.

The market is still pricing $IQE like a distressed, underutilized UK small-cap because backward-looking financial data feeds haven't adjusted to the new post-deal reality.

They are missing the bigger picture.

The debt is gone, the largest players in the chip space are anchoring equity deals to secure capacity, and IQE sits right at the choke point of the entire optical computing revolution.

While the crowd is still chasing raw substrates, the smart money is moving to the epitaxy bottleneck.

Now you understand why $IQE?

Why did I even get interested in $IQE?

When the entire market went absolutely crazy over $AXTI - I was swallowing the bitter pill of being late to that specific party.

But since I hate losing, I immediately started asking myself: what is next?

I always try to look one step ahead.

That is exactly how I managed to get early into names like $IQE or $LPKF and others before the masses caught on.

But back to $IQE - why this specific company?

The global frenzy and massive demand for optical lasers are just getting started.

The market quickly realized that Indium Phosphide (InP) - the core substrate material - does not just fall from the sky.

Hence, the massive explosive run on $AXTI.

But a raw InP wafer by itself is practically useless for high-performance photonics.

You have to actually do something with it before it can become a functioning laser.

Epitaxy.

Epitaxy is the atomic-scale deposition of crystal layers onto that substrate.

Only a handful of companies globally possess the highly specialized MOCVD and MBE machinery required for this advanced process.

One company listed on the London Stock Exchange owns a significantly larger fleet of these reactors than almost anyone else, giving them a massive structural scale advantage.

Say hello to $IQE.

Look at the pure-play competition for epi-wafers. Landmark Optoelectronics possesses far fewer machines, yet because it sits on a different exchange (Taiwan), it historically traded at multiples that make IQE look like an absolute deep-value steal.

And if you want proof of their technological moat:

IQE was just confirmed as the second largest patent filer in the entire UK for semiconductor devices.

This isn't a speculative small-cap; it’s an IP powerhouse.

Now, to be completely fair, IQE had a dark cloud hanging over it.

The cyclical semiconductor downturn cut their 2025 revenue to £97m, and because chip fabs have massive fixed costs, underutilization completely crushed their near-term margins.

Worse, geopolitical tensions flared as China introduced strict export controls on critical raw materials like Gallium and Antimony.

If you check most standard financial screeners today, that ugly debt and supply-chain risk warning still pop up.

But the market is looking backward.

First, IQE completely neutralized the China risk by successfully recycling 100% of their Gallium Arsenide and Indium Phosphide wafer waste directly back into ultra-pure raw materials for their production lines.

Second, on May 28, 2026 - the ultimate balance sheet reset happened.

IQE officially completed a transformational £81 million strategic recapitalization package.

MACOM Technology Solutions ($MTSI) stepped up to anchor the deal - injecting £30m in direct equity and £15m in new convertible notes to secure a ~15% strategic stake.

Existing institutional notes were swapped into equity, and the old HSBC bank debt was entirely wiped out.

The balance sheet is clean. The financial risk is gone.

So, who is MACOM and why does this partnership matter?

MACOM is a heavyweight in high-performance semiconductor products for Data Centers, Aerospace, and Defense.

They design the brains - the optical components and ICs that power next-generation networks.

By deeply aligning with IQE, MACOM secures a stable Western supply chain for advanced epi-wafers.

For IQE, it guarantees immediate structural volume demand to fill those empty reactors and unlock massive operating leverage.

And the momentum shift is already visible.

Photonics has officially overtaken wireless to become IQE’s largest segment (58.7% of revenue), propelled by surging AI data center demand and immediate US military and defense funding releases.

Think that is all?

We got another massive confirmation of their turnaround strategy.

IQE followed this up by solidifying their multi-year agreement with Tower Semiconductor ($TSEM).

Together, they are scaling Silicon Photonics (SiPh) via the heterogeneous integration of IQE’s advanced epitaxy layers directly onto Tower’s silicon wafers.

This allows them to build optical transceivers that handle the insane data transfer speeds required by modern AI architectures.

The pieces of the puzzle are coming together perfectly.

The market is still pricing $IQE like a distressed, underutilized UK small-cap because backward-looking financial data feeds haven't adjusted to the new post-deal reality.

They are missing the bigger picture.

The debt is gone, the largest players in the chip space are anchoring equity deals to secure capacity, and IQE sits right at the choke point of the entire optical computing revolution.

While the crowd is still chasing raw substrates, the smart money is moving to the epitaxy bottleneck.

Now you understand why $IQE?

@investingluc Well said. A successful business acquaintance has just taken his own life after getting in too deep with gambling. Wife and kids left behind

16.6x forward earnings on 48.6% revenue growth.

$AMPG's PSG is 0.16, so the market is barely paying for that growth.

The cheap multiple skips the chokepoint: ultra-low-noise and cryogenic RF amplifiers are the front end that lets satcom, 5G backhaul, and quantum qubit readout hear a faint signal.

$AMPG is the obscure pure-play, while the diversified comms giants are the crowded way in.

Q1 did $5.35M at 48% gross margin against a $50M full-year guide.

It's a loss-making micro-cap with dilution and reverse-split history, so I keep it small and add near $6.50.

Where I'm wrong: it's up ~247% in 3 months and that guide cracks.

Q1 annualizes near $21M, so where does the back half come from to hit $50M?

I did not see this one coming. BREAKING NEWS folks!

Midjourney, yes the AI image company, just launched a real medical device that feels like it's straight out of Star Trek.

https://t.co/LSs2zbYViM

They’ve unveiled the Midjourney Scanner, the first working prototype of Full Body Ultrasonic Computational Tomography. It uses a ring of thousands of tiny transducers to fire ultra-precise sound waves through the body. The returning echoes are captured at a staggering 17 gigabytes per second, and the 806 terabytes of gathered data are then reconstructed by a 2 petaflop compute system into a highly detailed 3D map of your entire internal anatomy — organs, tissues, blood vessels, etc., in 60 seconds.

The resolution is extreme: each sensor can resolves motion smaller than the width of an atom, detecting internal tissue details down to half a millimeter. And unlike MRI or CT scans, it uses no radiation, just sound. Think of it like getting an ultrasound from the 22nd century.

The ambition is breathtaking. Midjourney wants to build a fleet of 50,000 of these scanners, capable of delivering a billion full body scans per month. That's enough to make comprehensive full body imaging available to every person on Earth.

They’re not hiding it in cold, clinical hospitals either. The vision includes placing these scanners inside what look like Midjourney spas, turning what’s usually an annoying medical procedure into something genuinely pleasant.

This is Star Trek level healthcare infrastructure: fast, safe, non-invasive full body imaging at planetary scale. If they pull it off, it could fundamentally shift medicine from reactive treatment to proactive, early detection on a global level.

Progress (and Midjourney going full medical) marches on. 🩺🚀

One of Naspers subsidiaries apparently donated R8 million to the corrupt ANC. Did they donate the same amount to all other political parties? No, now ask yourselves why?

I will, as an easy start, boycott the following businesses. Impact in numbers!

Takealot – Use Amazon Prime, they are amazing!

Mr D – Use Uber Eats etc.

News24 – Use X.

Property24 – Use Private Property.

What I would like to point out regarding $AMPG is that, despite the significant rise in the stock, there has been no insider selling—with the exception of forced sales due to expiring stock options. If insiders expected the stock price to fall, they would be actively selling.

2 years ago, I said to buy $MU when it was under $80. Its up 1350% already.

My target for $MU is at least $5000+ from here.

Right now, memory is the biggest bottleneck in AI says Elon Musk:

$WDC $45 → $750 up 1650%

$SNDK $45 → $2050 up 4550%

$STX $75 → $1110 up 1480%

$DRAM $25 → $75 up 300%

♻️ RESHARE this post and write 1 comment, I'll DM you the LAST memory stock no one is paying attention to that will 20x-50x.

$BRUN $DGXX $IQE $INFQ $SIVE $SIVE.ST $LPK 170626 TA Update

As always, just my 2c. Pls like and repost if you find any value in this post! It takes quite a lot of work to analyse the charts. Thank you!🙊

$SIVE $SIVEF $SIVE.ST $LPK TA Update 170626

10/20/50/200EMA => blue/purple/yellow/red

$SIVE

What a day, closed at 101.9 SEK, up over 10%. It broke out of the bull flag consolidation cleanly. Any dip to the 10EMA (87.41) or 20EMA (79.36) is a gift imo, so 79 to 87 SEK would be great areas to add. Now I want to watch how it reacts at the previous high of 110 SEK, which lines up nicely with the 2.618 extension at 109.2. Position accordingly.

$LPK

This one finally broke past the golden pocket (22.7 to 23.6 EUR) and closed strong at 25.6, up nearly 16%. It opened right at the 10/20EMA and we got a 10/20 bullish cross firing, love to see it. The 50EMA at 19.38 held to perfection on the recent pullback. Any dip back to the 10/20EMA around €22 to €22.50 is a gift imo.

Both look very nice.