@NicoperJES Great read, thank you! Would you mind to explain how you got to know that the business that Pinetree sold is ReadyTech and following that Damien then bought another Australian VMS?

William Thorndike almost never speaks. When he does, you listen.

A decade ago, in 68 seconds, he named 10 current Outsider CEOs. Mark Leonard at $CSU. Mike Pearson at Valeant. Eight more.

Leonard compounded 10x. Pearson cratered 95%.

Now ask yourself: who would you put on the list today?

Opportunity above all VMS100 Index

Volume 2 1999 1st Quarter

- YTK details as noted before

- acquire Friedman Corporation $22 million in revenue

- Friedman + Emphasys = Vela Software 2013 and FOG is a byproduct of this acquisition

$CSU.TO

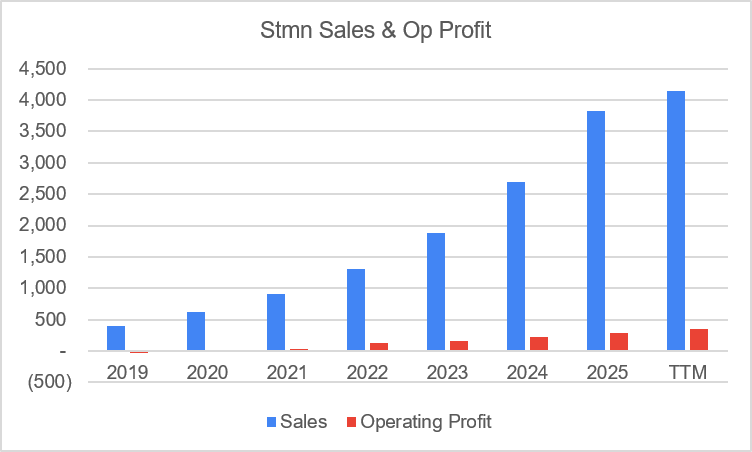

Another "only in Japan": employee engagement software company Stmn $4019.T growing organically at 40%, already reasonably profitable (9% OMs last qtr) trading <1x EV/S, 1x EV/ARR, 11x EV/EBIT and 19.5x P/E (heck even a 1.4% div yield!)

Dave Blundin from Moonshots says you need to own equity over the next decade to participate in the financial singularity

Here are some AI names you can dig into to moonshot your investment portfolio

-Leopold Aschenbrenner industries

-Recent Value Investors Club writeup

Li Lu on how to invest under $100k:

It's interesting in Korea there's a form of a securities called preferred securities.

These are essentially non-voting common stock that pay a slightly higher dividend — not much more, but they carry no voting rights.

For interesting reasons, these shares sometimes trade at a 70% to 80% discount to their voting common stock equivalents.

And within this group of securities, there are several companies that possess truly enduring franchises. These companies have been growing earnings and revenue at a compounded rate for over three or four decades.

Their businesses are like fortresses with very long purchase cycles — powerful earning machines that still have significant room for expansion. Yet they are trading at prices that represent only a tiny fraction of what they would be worth in a private transaction if someone were to buy the entire company.

In fact, even today, there are situations where the voting common stock and the non-voting shares are virtually identical in economic terms. In some of these companies, the founding family controls the voting shares anyway, so there is virtually no real difference between the voting and non-voting shares.

And yet, the non-voting shares are trading at an 80% discount — I’m not talking about 20%, but eighty percent. They are effectively trading at twenty cents on the dollar, if you believe the common stock reflects the true value.

This kind of opportunity has existed across many different securities. So if you’re young and just starting your career, and if I were starting all over again, I would first study the great examples in history where the market went to extremes on a small segment of securities — creating tremendous margin of safety. Even if things go wrong, you can still come out okay and remain in the game.

Then, study what is available today. At any given time, there are always opportunities like this. It really comes down to fundamental human psychology. And as long as humans remain the same — which I suspect they will, even after billions of years — these opportunities will continue to appear.

Warren Buffett doesn't use EPS. Most investors know that. What fewer know: he doesn't use free cash flow either. He uses a metric he defined himself in 1986, and Wall Street still largely ignores it.

It's called Owners Earnings.

Here's what it is, and how to calculate it: https://t.co/vB5rw4SKey

$CSU Click CEO shared how CSU businesses can rapidly operationalize AI agents in commercially practical ways—humanizing AI agents by giving each one a name, a MSFT Teams account, & a place on the org chart, allowing employees to interact with them like any other colleague.