nice places get crowded which creates competition for nice things like houses, price goes up and not everyone can afford it, they move elsewhere making it less crowded. everyone wants to live in nice places, not everyone can. Like the cost of going to the superbowl or a browns game (lifelong browns fan)

not income, value of production per person

GDP per capita is the gross domestic product of a country divided by its mid-year population (or average population for the year).GDP = The total monetary value of all final goods and services produced within a country's borders in a specific period (usually one year).

Per capita = "Per person" (from Latin: per = by, capita = heads).

@WallStreetApes we elect people, to appoint people to prosecute crimes, we know they don't/won't what we are feeling now is helpless to effect any outcome. trump, biden, trump,obama,obama,bush,bush, clinton, clinton, bush, blah, blah, blah

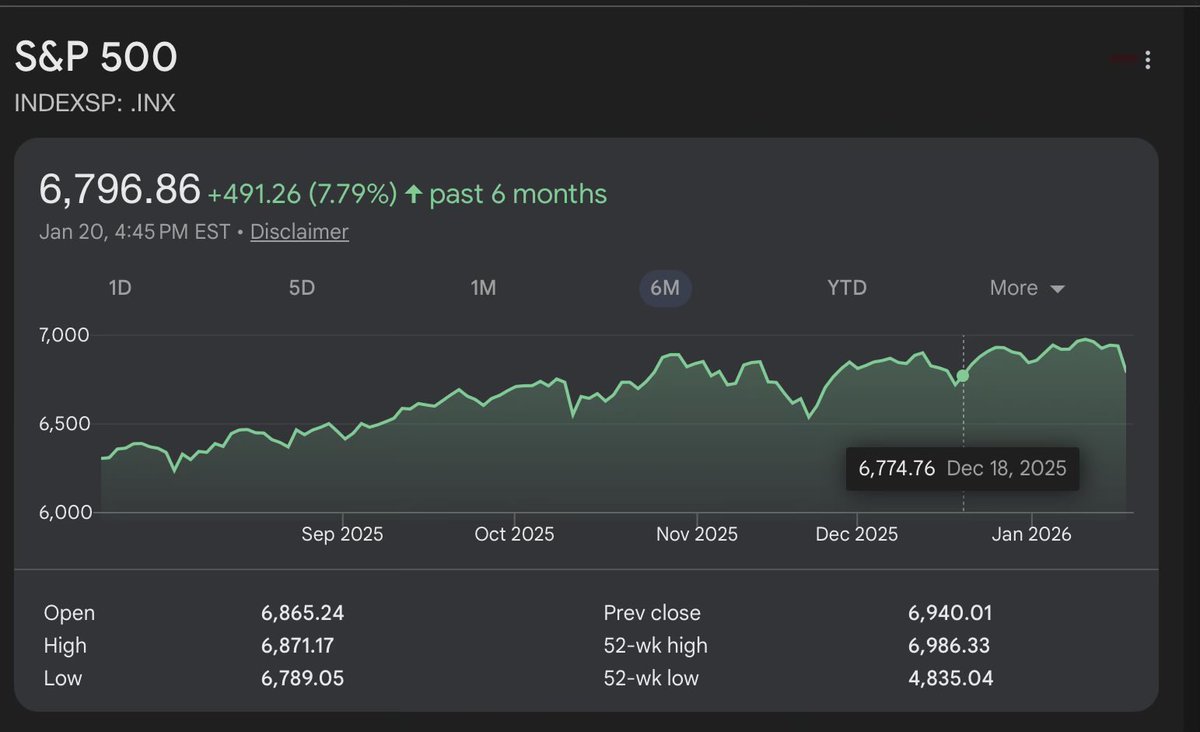

"After 35 years in the markets, I've seen the same pattern repeatedly: When prices surge rapidly (especially in assets like stocks or gold), almost no one questions it or digs into the 'why.' Everyone just rides the wave, assuming it's justified—smart money piling in, momentum at work. But when those same assets give back even a portion of the gains, suddenly the sky is falling: 'The system's collapsing,' 'bubble bursting,' endless doom-scrolling. Look at gold right now. It was up roughly 10% in January 2026 alone (after hitting explosive new highs above $5,500–$5,600/oz amid geopolitical tensions, tariff threats, dollar weakness, and massive central bank buying). Over the trailing 12 months, it's gained around 70–90% (depending on exact entry points, with some sources showing even higher year-over-year returns from early 2025 levels). No one batted an eye or asked too many questions during that rocket ride—comfortable, confident, 'this time it's different.'Then gold pulls back ~12% (from peaks near $5,600+ down toward $4,900 levels in late January/early February, with sharp sessions wiping out billions in paper value). Suddenly, it's panic mode: systemic collapse, crash narratives everywhere.'Markets move faster than ever before. Hot money flows in and out at warp speed—both directions. Volatility is amplified, but the underlying drivers (safe-haven demand, uncertainty, de-dollarization trends) haven't vanished. Pullbacks are normal after parabolic runs; they're healthy, often shake out weak hands, and set up the next leg higher if fundamentals hold.The asymmetry in reaction is human nature: greed is quiet, fear is loud."

When you sell (or "write") a call option, the buyer on the other side is purchasing it from you. They pay you a premium upfront for that right.

Sometimes, market exuberance (like hype, FOMO, or strong bullish momentum) can inflate option premiums significantly, making selling calls more attractive in the short term. However, that kind of exuberance is usually temporary—premiums often dry up once the excitement fades. For example, I did this with NVDA for about a year during its high-volatility run, collecting nice premiums at first, but eventually the inflated premiums disappeared as the market normalized.

Important point: When you sell a call, you're obligated to deliver the underlying stock at the predetermined strike price if the buyer exercises the option. This exposes you to real risk:

If it's a covered call (you already own the shares), your main risk is opportunity cost—if the stock surges way above the strike, your shares get called away, and you miss out on further upside. You also face downside risk if the stock drops sharply (though the premium you collected provides some cushion).

If it's a naked/uncovered call (you don't own the shares), the risk is theoretically unlimited because the stock price can rise indefinitely, forcing you to buy shares at a much higher market price to deliver them.

Stocks don't always go up—they can drop 20%, 50%, or more in corrections, crashes, or bad news. The person on the other side of the trade might be smarter than you, or you might be smarter than them. That's exactly what makes a market: two parties with opposing views agreeing to a trade.

Selling calls can generate income, but it's not "free money"—it comes with real obligations and risks that need careful management. Always know whether your position is covered or naked, and size trades according to your risk tolerance.

Blue Chip

$ENPH (Enphase Energy) — Solar microinverters and energy solutions. Recent prices around $34–35 (e.g., ~$34.98 in some feeds, with intraday/open near $35). It's been volatile, down significantly over the past year but showing some stabilization. Analysts have mixed views, with average targets in the low $40s and some seeing 2026 as a potential trough before recovery tied to energy demand.

$OSCR (Oscar Health) — Tech-driven health insurance. Trading around $16–17 (e.g., ~$16.57–$16.87 recently). Volatile with high volume; beta >1 suggests it moves with the market.

$ZETA (Zeta Global) — AI-powered marketing cloud platform. Around $20–22 (e.g., ~$20.38 in recent data). Strong buy ratings from some analysts with targets up to mid-$40s, implying solid upside potential.

$CELH (Celsius Holdings) — Energy drinks (functional beverages). Higher-priced name, recently in the $50s–$54 range (e.g., ~$54). Strong performer in recent years with retail momentum and PepsiCo ties, though P/E is elevated.

$SOFI (SoFi Technologies) — Fintech (lending, banking, investing). Around $26–27 (e.g., ~$26.19–$26.40). High volume and beta; continuing to show profitability improvements and growth narrative.

$GTLB (GitLab) — DevSecOps platform. Around $34 (e.g., ~$34.20). Down from highs but in a range; some technical setups noted for potential reversal.

$HIMS (Hims & Hers Health) — Telehealth and wellness (e.g., hair loss, ED, weight management). Around $31 (e.g., ~$31.38–$31.49). Volatile with high beta; some bullish chatter in communities targeting higher levels.