@DarioCpx@barnes_law I’m increasingly convinced that the US wants Hormuz shut forever. It forces anti-involution on China and booms our economy. Then helps offset all the Mercantilism from Asia and Europe through higher energy prices. Just sayin’…

The US naval blockade is definitely biting, and Iranian crude exports are cratering, but the street is completely misreading the mechanics here.

Iran's oil export engine is nothing but a massive, structural money-and-logistics laundering matrix. On the physical side, the whole game is evading US eyes to scrub Iranian barrels and make them look completely kosher on paper.

The second these tankers clear the Strait of Hormuz or hit the Indian Ocean, they flip the switch and turn off their AIS. They’ll even manually paint over or mask the hull numbers to stay invisible to satellite tracking.

The real action happens via STS transfers in the EOPL or UAE, bleeding the cargo into un-sanctioned dark fleet.

While doing this, they doctor the Bill of Lading to wipe the origin clean, magically re-christening Iranian crude as Malaysian Blend or Omani barrels.

Those barrels eventually show up at the doorsteps of Shandong Teapots in China to discharge. That’s exactly why Beijing's official import prints show a massive spike in Malaysian volumes, while Iranian imports look like zero.

Obviously, standard trade finance rails like SWIFT and USD clearing are dead in the water. To bypass this, Tehran runs a bulletproof shadow banking network.

They’ve layered dozens of shell companies across Dubai, Hong Kong, and Turkey. Domestic Iranian networks, like the Amin Exchange, act as the central bank for these offshore front accounts.

The tape settles in RMB or AED, never greenbacks. Once a teapot wires cash to a shell account, the funds are instantly fractured and routed across multiple front profiles via Hawala style to completely blind any tracking.

When cash routing hits a brick wall, they just pivot to straight-up barter—clearing the oil bill in exchange for Chinese refined products, industrial machinery, consumer goods, or military hardware components.

This entire clunky setup creates a massive lag in the cash conversion cycle. Moving from Iranian loading docks, steaming dark at low speeds, floating in international waters waiting for an STS window, forging the papers, and finally getting the teapots to clear customs takes a solid 60 to 90 days.

Even when the teapots pay up, washing that money back through UAE and Hong Kong shells until it turns into spendable dry powder (or hard goods) for Tehran or the IRGC takes another 60 to 90 days.

Bottom line: Iran is running on a 3 to 6 month delay from the time the oil leaves the ground to when they can actually spend the cash.

This duration risk and the structural discount blow out even wider whenever the US drops a combined hammer—like the Economic Fury campaign—targeting not just the dark fleet, but the financial nodes and clearing desks in Hong Kong and the UAE at the same time.

Every sweep locks up accounts and forces them to rebuild their routing from scratch.

So the liquidity hitting Iran's balance sheet today is cash from oil traded months ago. Since they're still clearing out the oil on water floating outside the Strait, it’s going to take months before their actual financial runway gets cut off.

But the real macro question everyone is missing is this: these guys already proved they can survive on zero exports during the COVID pandemic. Why is everyone so sure this cycle plays out differently? Who breaks first under the weight of time—Tehran or Washington?

That’s the real chart worth watching.

#oott #iran

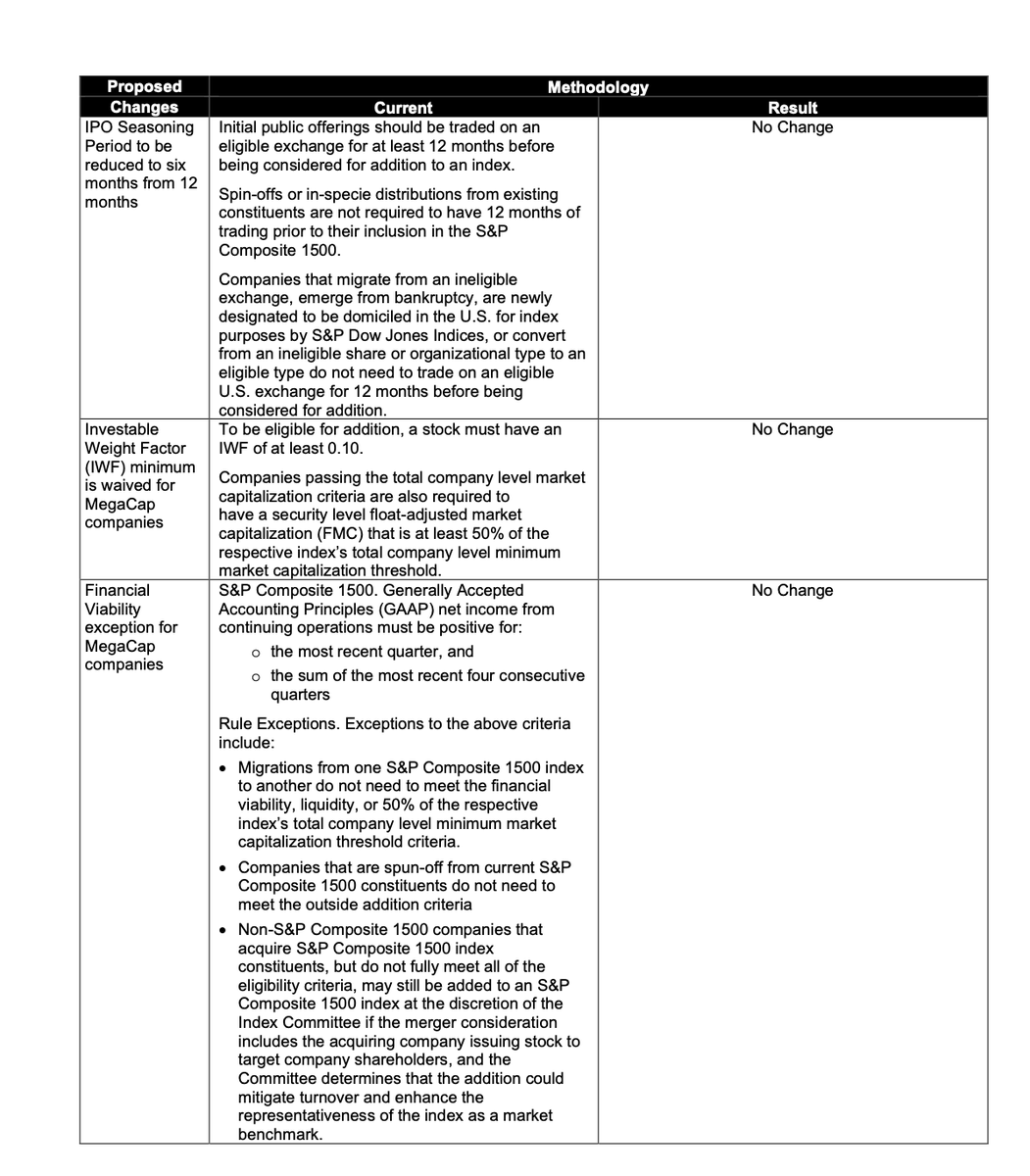

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

🚨 do you understand what just happened with the SpaceX IPO..

Fidelity quietly dropped its minimum account requirement from $500,000 to $2,000 - a 99.6% cut that lets millions of small retail investors in days before the biggest stock debut in history.

The catch is who they need to sell to.

- SpaceX reserved up to 30% of the offering for retail, far above the usual single-digit share

- Selling within the first 15 days triggers Fidelity penalties up to a permanent IPO ban

- At a ~$1.675T pre-money valuation this IPO creates more exit value than every VC-backed IPO of the last decade combined

- The xAI side lost $6.4B from operations in 2025, dragging a Starlink-powered company billions into the red

They opened the gates right when the smart money needs someone to sell to. Read the prospectus before you become it.

AI bubble highlights

Anthropic :“Hey guys please

lend us money.”

Debt Financiers: “Great let’s see the numbers.”

Anthropic: “We would rather not!”

Ends well.

The easy explanation is that a few trillion-dollar tech companies are dragging up the average.

It's true, but it's still not the answer.

The records are everywhere: manufacturing margins hit 15% in 2022 and sit near 13% today, the highest in 25 years.

3/

Correct. And just like the shale boom, the entire industry is stuck in a prisoner’s dilemma where every player must keep spending or risk beeing seen as a laggard in the race to zero

If you want to visualize the next decade of big tech returns, just plot the $xle from 2012 - 2021

If this is really a stealth manufacturing boom, why is the Employment Index still contracting at 48.6, why has manufacturing employment contracted for 32 straight months and in 40 of the last 41 months since January 2023, why were only 25% of respondent comments positive while 69% were negative, why is the Prices Index still at 82.1 with raw material prices rising for the 20th straight month and zero commodities listed as down in price?

And why are Supplier Deliveries at 60.6 being treated as strength when slower deliveries mechanically lift the PMI and the report ties those delays to Iran, energy, petroleum products, tariffs, freight, semiconductors, steel, aluminum, and supply chain stress, why did New Orders rise while the share reporting higher orders actually fell from 31.6% to 30.9%, why did Production rise while the share reporting higher production fell from 28.3% to 26.7%, why are backlogs only 52.2 and still below February’s 56.6 and March’s 54.4, and why did exports barely return to expansion at 50.6 while only 5 of 18 industries reported export growth and export comments were negative by 2 to 1?

Ai says it would take a team of four professional divers 2 to 5 days just to clean a single ship propeller of barnacles

Now extrapolate this to over a thousand ships and not just the propeller

We may be in deep trouble