Before New York was New York, it was New Amsterdam, a Dutch colony built on pluralism, capitalism, and a radical idea that tolerance could be a competitive advantage. Russell Shorto (@RussellShorto) joins me on Open Book to tell the story of how a bloodless standoff in 1664 didn't just transfer a city from one empire to another; it set the genetic code for everything New York, and really America, would become.

Watch on X, YouTube, Spotify, or wherever you get your podcasts.

Timestamps

0:00 Russell Shorto Introduction

1:33 What drew Russell to writing about NYC history?

4:35 The 12,000 pages of Dutch records that changed everything

6:17 What was pioneered in NYC: pluralism, capitalism, and the stock exchange

10:50 New York's deep-water geography and the Hudson-Mohawk highway into the continent

14:34 How unusual was religious and ethnic diversity in 17th-century Europe?

16:08 Anthony "NYC is the land of opportunity."

17:44 The paradoxes of early New York: tolerance alongside slavery and Native displacement

22:15 Liberalism, tolerance, and capitalism as core topics

24:37 If Nicholls and Stuyvesant toured modern Manhattan, what would they think?

26:22 Five Words

“I have secured an indictment against Jenny. This bitch will think twice before she threatens the president again.” — Extreme alcohol enthusiast, Jeanine Pirro

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

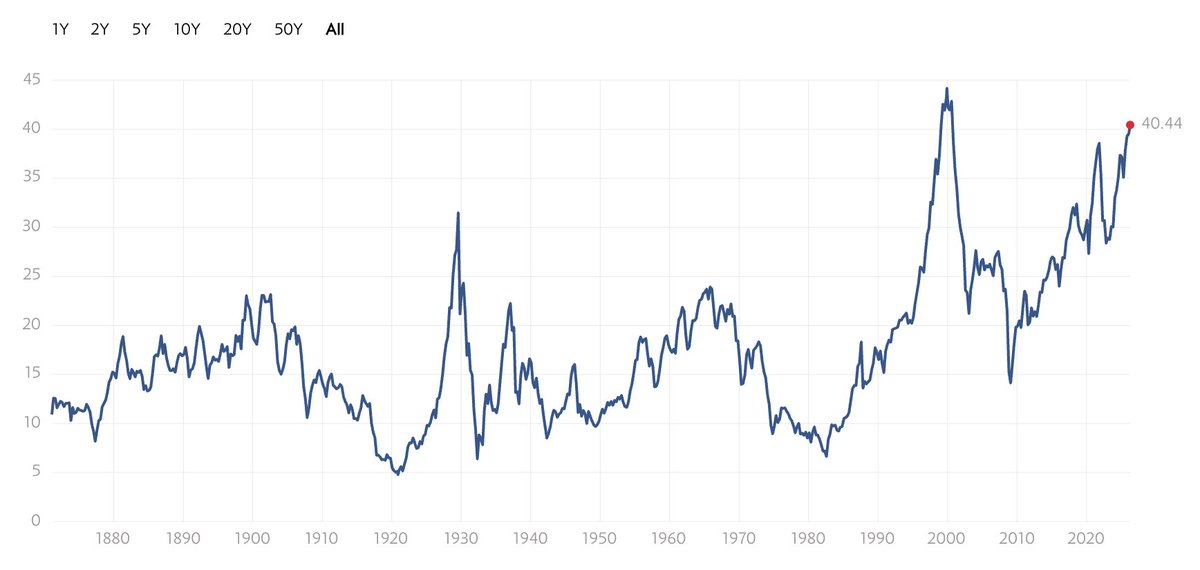

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy:

"We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%.

If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years.

Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.

In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country.

And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008.

The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows.

So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now.

Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."

The reporting on OpenAI and Sam Altman that I've been working on for the past year and a half, for @NewYorker, with @andrewmarantz: https://t.co/HEPHN4E54P

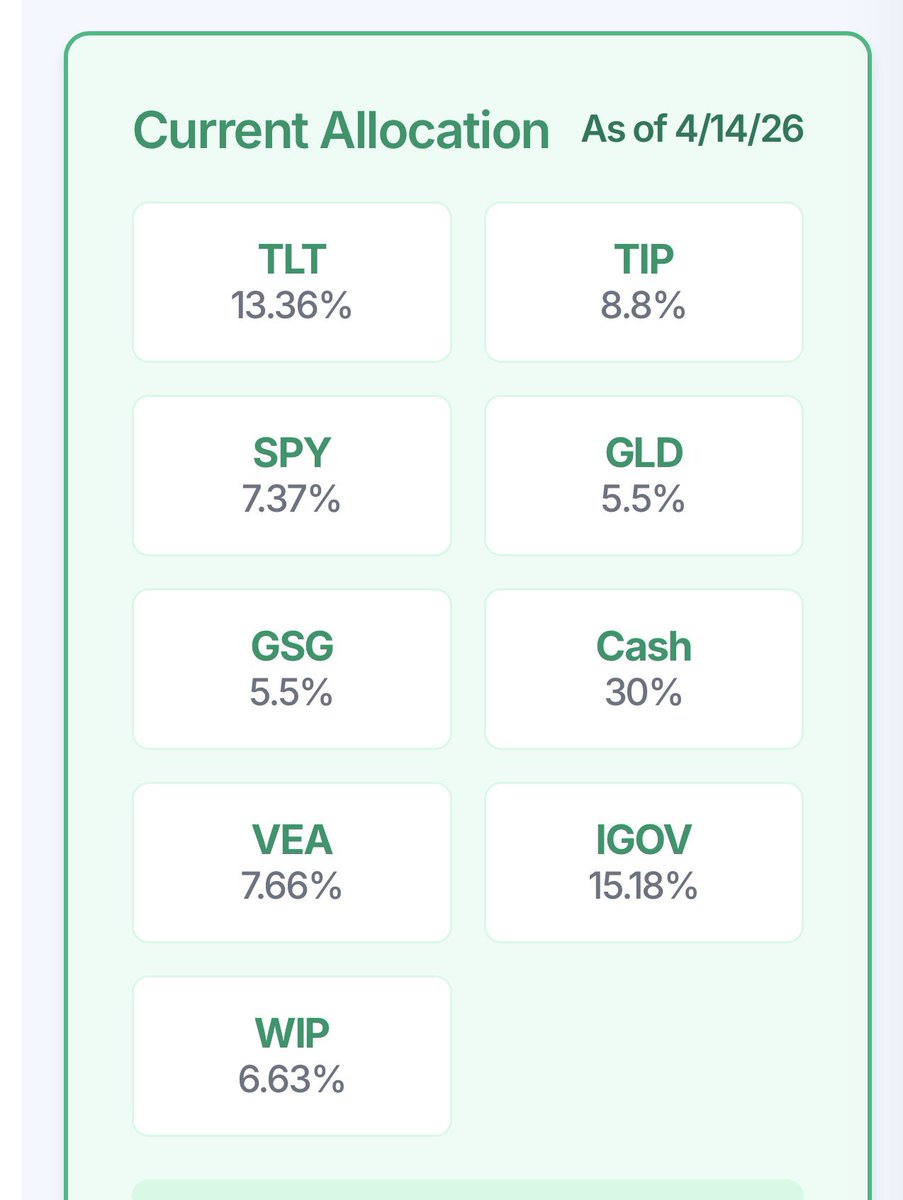

I manage my wealth this way in general and I am positioned this way within this framework today 101

I take $100 of cash

And invest in DSSmart Beta which is always long global stocks bonds, gold, and commodity indices. That allocation size is between $50 to $130. At the low allocation I have $50 of cash invested in global money market mutual funds. At the high I am leveraged 30% which I fund by shifting from ETF's to futures and via other low cost leverage

With the $100 portfolio as described as my "collateral" I buy options, buy 1x1 options spreads, sell 1x1 option spreads in a strategy called DSAlpha. This portfolio construction results in 💯 certain worst case loss at any particular time. On rare occasions (like today) I also hold futures contracts (long or short) with wide stop losses which could result in unlimited loss but that is unusual.

The net return on my $100 is then the dollar pnl of each strategy summed up and divided by my investment amount. Thats DSAlphaBeta return

DSSmartBeta can be reported separately but its denominator is $100 regardless of its allocation

DSAlpha needs a denominator too. People cheat to show high returns by using low denominators. I do not cheat and simply divide the PNL by the same $100 meaning the total pnl of both strategies, the pnl of beta and the pnl of alpha are all first in dollars and second divided by the same denominator which is my wealth. Their sizing in terms of pnl and risk contribution is roughly the same and targeted at 10% annual volatility AND the two strategies are meant to be uncorrelated and are not "hedging" each other but are diversifying each other

Anyway currently this is DSSmartBeta allocation which is long roughly 16% of global equities

Based on current marks my DSAlpha book of equity puts, oil shorts and a small STIR bet has $3 of put spreads which will be worthless by June (most) and September (less) if equity markets stay here.

The DSAlphabeta portfolio currently has 16% long equities from SmartBeta and the $3 of puts generates a short delta of 50% for an overall portfolio delta of -34%.

It just so happens that alpha is short and beta is long and my net is short which would imply alpha is a hedge. Its not. In 2021 SmartBeta was 130% long and alpha was max long. Today one is long (always long) and the other is max short. Beta is always long and had a lifetime horizon. Alpha is long short or no position and has a 2-6 month horizon. I treat them separately because I think they are separate activities. I've though market timing and long only investing are separate skills for my whole career. Bridgewater training further crystallized that distinction for me. Some disagree. Particularly those who want to charge high fees for beta returns (pretty much everyone on the planet grifting you)

I can't be more clear than this and if you don't understand what I am talking about feel free to search my feed with the prompt "101" where I articulate basic concepts in money management, portfolio construction and options investing. Also there are great people who can help you through these concepts including @perfiliev and @KrisAbdelmessih (two of my favorites).

🦔A researcher invented a fake eye condition called bixonimania, uploaded two obviously fraudulent papers about it to an academic server, and watched major AI systems present it as real medicine within weeks.

The fake papers thanked Starfleet Academy, cited funding from the Professor Sideshow Bob Foundation and the University of Fellowship of the Ring, and stated mid-paper that the entire thing was made up. Google's Gemini told users it was caused by blue light. Perplexity cited its prevalence at one in 90,000 people.

ChatGPT advised users whether their symptoms matched. The fake research was then cited in a peer-reviewed journal that only retracted it after Nature contacted the publisher.

My Take

The researcher made the papers as obviously fake as possible on purpose. The AI systems didn't catch it. Neither did the human researchers who cited it in real journals, which means people are feeding AI-generated references into their work without reading what they're actually citing.

I've covered the FDA using AI for drug review, the NYC hospital CEO ready to replace radiologists, and ChatGPT Health launching this year. All of that is happening in the same environment where a condition funded by a Simpsons character and endorsed by the crew of the Enterprise was being presented as emerging medical consensus. The people making these deployment decisions seem to believe the pipeline from research to AI to patient is more supervised than it actually is. This experiment suggests it isn't supervised much at all.

Hedgie🤗

https://t.co/8Kg8FOrgHW

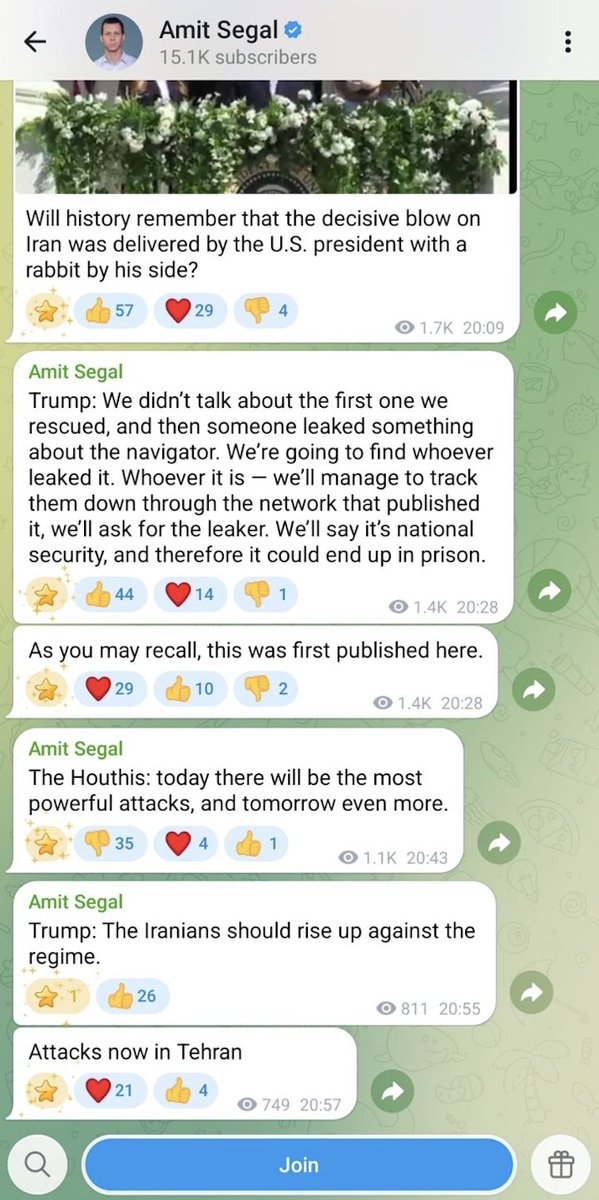

As @AmitSegal just acknowledged on his Telegram channel, he was the first to publish details about the missing second airman. Segal is an Israeli journalist known for his immediate proximity to Netanyahu.

Trump has threatened to jail the journalist who first reported on the missing airman in order to force him to confess the identity of his source. Segal does not appear concerned.

With the current expectations, prices don’t return to what they were pre-war.

There is a world where war happens, and there is more traffic from the strait, but it’s MORE expensive due to toll, increased insurance and lower supply.

Markets likely:

* Sell off on boots on the ground

* Rally on Strait traffic with optimism

* Then grind down as actual margin compression and inflationary pressures set it

Oil:

* Spikes to a high on boots

* Quickly recovers as traffic opens up

* Creeps up as lower volume and higher fees settle in

That’s a world of sustained $80+ barrels of oil.

It means:

* Tech, AI and pharma are probably a buy on any initial dips, if not exposed to energy sensitive sectors.

* Energy sensitive sectors are a short after initial rally

-Airlines

-Shipping freight companies

-Logistics & delivery

-Petrochemical companies/manufactures of plastic

-Plastic heavy consumer products (wish Tupperware was still around to short)

-Heavy weight shipping goods (paper products, furniture, etc)

-Bottled goods/CPG heavy on plastic packaging

* Rate sensitive businesses are a short:

-Anything with leveraged debt such as some telecom or healthcare

-REITs with short term debt

-Homebuilders

* Rate benefactors could be a long if reasonable P/E as we’ve overly priced in rate cuts that may not materialize

* Aerospace & defence is (sadly) a long as this sustains and large repair bills of multiyear projects in the Gulf

* Gulf heavy luxury brands, tourism, and real estate are a high risk long, even if they don’t reach prior highs, boots on the ground focuses conflict into Iran, lowering the regional risk slightly

* Gold likely a long, after the heavy state selling it likely continues accumulation in an uncertain world

* EU defence and Canadian defence are a strong long, as NATO uncertainty continues and they seek US independence

Overall the TL;DR:

* This market will chop both ways on fear and optimism before grinding towards something that reflects the reality.

* That reality is an increased long term cost, but that cost is materially lower than current levels.

* Buyers positioned for the long term, can buy strong fwd P/Es here but MUST expect volatility.

Tesla Self-Driving sucks and doesn't work.

This compressed video shows 90 minutes of Tesla's V14.2.2.5 moving through the heart of Philadelphia, and back to the suburbs for some errands.

As you watch this clip, you'll start to realize that Tesla's goal of autonomy at-scale is very far from here, and probably won't ever actually happen. The entire charade is nonsense. Tesla cars have level 2 ADAS just like SuperCruise and BlueCruise.

Yes, your Chevy Silverado does do this.

More music by the homie @StainlessOne

In 2019, MIT professor Patrick Winston gave a legendary 1-hour lecture called “How to Speak.”

It has 18M+ views for a reason.

His frameworks:

• Your ideas are like your children

• The 5-minute rule for job talks

• Why jokes fail at the start

15 lessons on communication:

Why Tesla "Robotaxis" Won't Be Driverless for a Long Time! by @BradMunchen

Deep Dive into FSD Crash Data Shows Incidents Becoming More Dangerous for Tesla Owners,

While Tesla's Austin Robotaxis Already Crash 4x more Frequently than Human Drivers!

https://t.co/cdYr0ozCa7

I have to say @Emilia_Javorsky has just conducted a masterclass in criticizing the current AI hype without throwing the baby out with the bathwater. It's 30 minutes long, I don't care. Watch it all. I don't agree with all of it, but this is how you move the needle on discourse.