So Meta, Google, Anthropic, SpaceX, and OpenAI will raise around $350B-$400B from the public markets in the next 9-12 months

At this rate, Amazon & Microsoft will join the party too

We might even see $550B-$600B raised from the public markets

Harvey is valued at $11B. Legora just raised at $5.5B. I built their entire web application in two weeks and I'm making it open-source and free for everyone to use. Say hi to Mike: https://t.co/NdtTt5MSJ2.

When I got the chance to try Harvey and Legora, I was surprised by how simple they were. A thought came to mind: I could probably build something similar in no time at all with Claude. And so I did.

Assistant, project, tabular review and workflows. You get it all without vendor lock-in.

Mike offers law firms an alternative, where they own the application layer and aren't stuck with a vendor they're renewing forever.

You can try Mike in the demo on the website, or go to the GitHub link on the site to download the code and run a local version yourself.

Asked GPT and Claude (both paid versions) which mega cap is likely to have the best / worst post earnings reaction today.

GPT

best $META

worst $MSFT

Claude

best $GOOGL

worst $MSFT

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

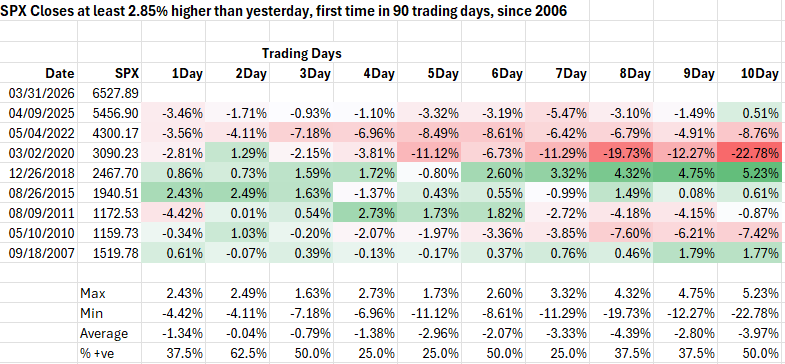

SPX rallied 2.9% today. This marks the first time in 90 trading days that SPX finished at least 2.85% above the prior close.

Historically, these outsized upside shocks have tended to precede higher volatility rather than sustained momentum. Looking back to 2006, similar occurrences have generally been followed by choppier price action and weaker risk‑adjusted returns over the subsequent one to two weeks.

What stands out in the data:

1) Near term returns skew negative. Average performance is negative across every horizon from 1 to 10 days, indicating poor follow through after the initial surge.

2) Weakness tends to deepen with time. Drawdowns are modest early but deteriorate meaningfully after Day 4, with the Days 6-8 window showing the worst combination of win rate and average return.

3) Volatility increases with a lag. The largest downside outcomes do not occur immediately; historical worst‑cases widen from single digit declines early on to roughly ‑20% or more within two weeks.

4) Upside tails are narrow. Strong positive follow through beyond one week is rare and largely driven by a single historical episode.

5) Even at horizons where outcomes are positive roughly 50% of the time, average returns remain firmly negative, implying losses have historically outweighed gains.

Bottom line:

Large upside shock days have tended to mark inflection points within downtrends rather than new trend accelerations. Price action becomes choppier and risk skews to the downside. History argues for expecting higher volatility and poorer risk-adjusted returns, not a smooth continuation higher.

Thanks.

It just feels awfully coincidental that on one side of the world you have overproduction forced upon western markets at below cost prices and ultimately funded by financial repression. And on the other side of the world you have a private credit binge keeping people employed in equally inefficient companies, many of them also going after scale at any price and funded by historic liquidity, now consciously being removed.

The whole SV emerging tech unicorn phenomenon is to me the mirror of Chinese industrial policy. Most of the corps coming out of that space “win” by giving away their product for free or at below cost prices until they capture enough market share to kill off all their competitors. But the model is perpetual meaning there are alway new loss makers entering the market hoping to undercut the dominant ones.

So just like in China you get this insane competition until only one dominant player can survive, and in emerging they eat up all the other players at pennies on the dollar in a way that allows them to extend and pretend via consolidation.

But it’s also a quota based rather than price based system. Even in the west the market has over the past decade been conditioned to rewarding companies for growth at any cost rather than for profit, sustaining unprofitable companies for years and years providing they just keep growing.

And they’re only able to keep growing because of the deep pocketed support of private equity corps or VCs, most of whom are funded by real money pension funds, and rewarded in paper returns expressed through rising stock prices rather than dividends.

That is the only difference. Except now that pension funds are being drawn on because of demographic forces that is going to become much harder to sustain. These investors need cashflows not unrealised stock market gains.

As it stands, it’s just a deferred form of financial repression. The illusion that it’s not was maintained by Fed liquidity. People will eventually realise their investments are worthless (or rather only worth anything for as long as they don’t draw on them), but only when they try to draw on them.

And where does the quota based effect come in in the west? I think via the compensation channel.

Remember private credit mostly became a thing to support the businesses that were over invested in by private equity just to keep their opaque valuations up, an to maintain the pay checks of all the people who became dependent on the original capital misallocation. To me it is akin to the circularity of the Chinese financial institution model, wherein banks buy the debt of local municipalities which then support projects that keep the failing firms going. Except where Chinese banks are funded by depositors at repressed rates, private credit is funded by pooled long term investment capital, at fantasy return promises.

But the key point is that managers at private credit firms earn large rewards through carried interest, bonuses, and equity tied to the size and performance of their funds, which creates incentives to raise larger pools of capital and lend it quickly on the promise that these companies will grow at any cost. Compensation becomes tied to growth.

And as competition increases, this leads to higher leverage and weaker loan protections for borrowers.

That is involution. Eventually every unit of new credit extend simply feeds a loss making business model that only makes it more expensive to fund the next unit of growth.

Austria issued a 100 year bond at zero yield in 2020. The guys that bought it are all deep under water and should be fired yes but what puzzles me more is why no other country followed suit.

Just few years ago, people were paying to lend money to Germany for 30 years. Why on earth would someone do that and not get fired afterward?

Chart: @MacroMicroMe

The most productive form of civilization is the high-trust liberal republic where everyone follows the rules and forgoes tribalism.

The only way to defend such a society is by being suspicious, defensive, illiberal, and tribalist.

So it goes.

@TheCromenockle I have 4 kids including a 3 month old who is now sleeping through the night.

It can absolutely be done. Books by Gina Ford on how to establish a routine have been very helpful.