💎WEEKLY Focus-Sector Wrap:

🔴 #GOLD -5.3%

🔴 #SILVER -10.4%

🔴 #PLAT -8%

🔴 $GDX -11.9%

🔴 $GDXJ -15.7%

🔴 $SIL -14.4%

🔴 $SILJ -14.7%

🔴 #SPUT -4.3%

🔴 $URNM -9.8%

🔴 $URNJ -13%

🔴 $URA -10.8%

🔴 $UEC -8.1%

🔴 $DNN -12.9%

🟢 #WTI +2%

🟢 $XLE +2.5%

While this week delivered sharp downside volatility across several of our focus sectors, this is the type of price action we've been patiently preparing for.

Pullbacks and corrections create opportunity. Our focus remains on executing our plan rather than reacting emotionally to market headlines.

Right Sectors | Right Time | Right People

We’ve successfully timed interim peaks and valleys in our focus sectors since 2020.

🔗Promo: https://t.co/1C4hqU52Wo

Feb 27 is the day before the war began.

The black line is the S&P 500; it is up 10+% since Feb 27.

The blue line is the S&P WITHOUT the AI stocks (see the description and repost). It is still DOWN 0.66%.

Maybe soaring gas prices are having an impact on the market after all?

The very fabric of space-time at the smallest scales is thought to be extremely turbulent and chaotic, described as a frothy sea called quantum foam. This concept, stemming from quantum mechanics and general relativity, suggests that the very nature of space-time is bubbling with tiny wormholes and fluctuations that appear and disappear within fractions of a second.

📷by Johann Rosario

Chamath just delivered the clearest diagnosis of what is happening to enterprise software and the OpenAI Deployment Company is the most damning piece of evidence he could have picked.

"The low end of the market is basically finished. There is no safe space."

90% of public SaaS stocks are down 30-80% from their 52 week highs, the median software stock is now negative over the last 3-6 months.

Goldman Sachs reported that software forward P/E multiples fell from 35x to 20x, the lowest absolute level since 2014 and the smallest premium to the S&P 500 since 2010.

The low end died first and fastest, because AI replaced it most directly.

The small business tools, the lightweight project managers, the single function SaaS products that charged $49 a month per seat, those are being replaced by AI agents that do the same work as a workflow, not a product.

You do not buy an AI powered tool, you describe what you need and it builds it and the seat based model that created the SaaS industry simply does not apply to that transaction.

But Chamath's more interesting argument is about the high end and the tell he points to is perfect.

OpenAI just raised $4 billion from 19 investors including TPG, Brookfield, Bain, and McKinsey to launch a consulting company and guaranteed those investors a 17.5% annual return to do it.

On $4 billion in committed capital, that is roughly $700 million per year in guaranteed payouts, owed by a company that is projected to lose $14 billion in 2026.

The goal of this venture is to compete directly with Deloitte, PwC, Ernst & Young, Andersen, and Cognizant.

Think about what that structure reveals.

OpenAI lost half of its enterprise LLM API market share from 50% to 25% between late 2023 and mid-2025, with Anthropic now leading at 32%.

Its response was not to build a better model but rather to raise $4 billion, offer guaranteed PE-tier returns and hire embedded engineers to physically sit inside client organizations and make AI actually work in production.

The reason, as Chamath identified, is that the high end of the market is not easy.

"It's not like boop boop boop, put in a prompt and beep bap boop, it all works," he said and the data confirms exactly that.

88% of organizations running AI agents reported a security incident in the past year, 42% of C-suite executives say AI adoption is creating internal organizational conflict.

The average enterprise AI consulting implementation costs $228,000 in year one versus $77,000 for platform-based approaches and most still stall before reaching production.

Anthropic immediately matched OpenAI with a competing $1.5 billion consulting venture backed by Blackstone, Goldman Sachs, and Hellman & Friedman bringing the combined spend by the two leading AI labs on human powered enterprise deployment to $5.5 billion in a single month

Chamath's read is that the high end, the large enterprise platforms like Salesforce with proprietary data flywheels, Palantir with its FDE model already proven at scale, Oracle with vertical specific data moats will survive and consolidate.

The mid-market point solutions, the single function tools, the lightweight enterprise apps without defensible data assets, those are on the conveyor belt.

The AI industry is not just disrupting the companies that use software but rather disrupting the companies that sell it.

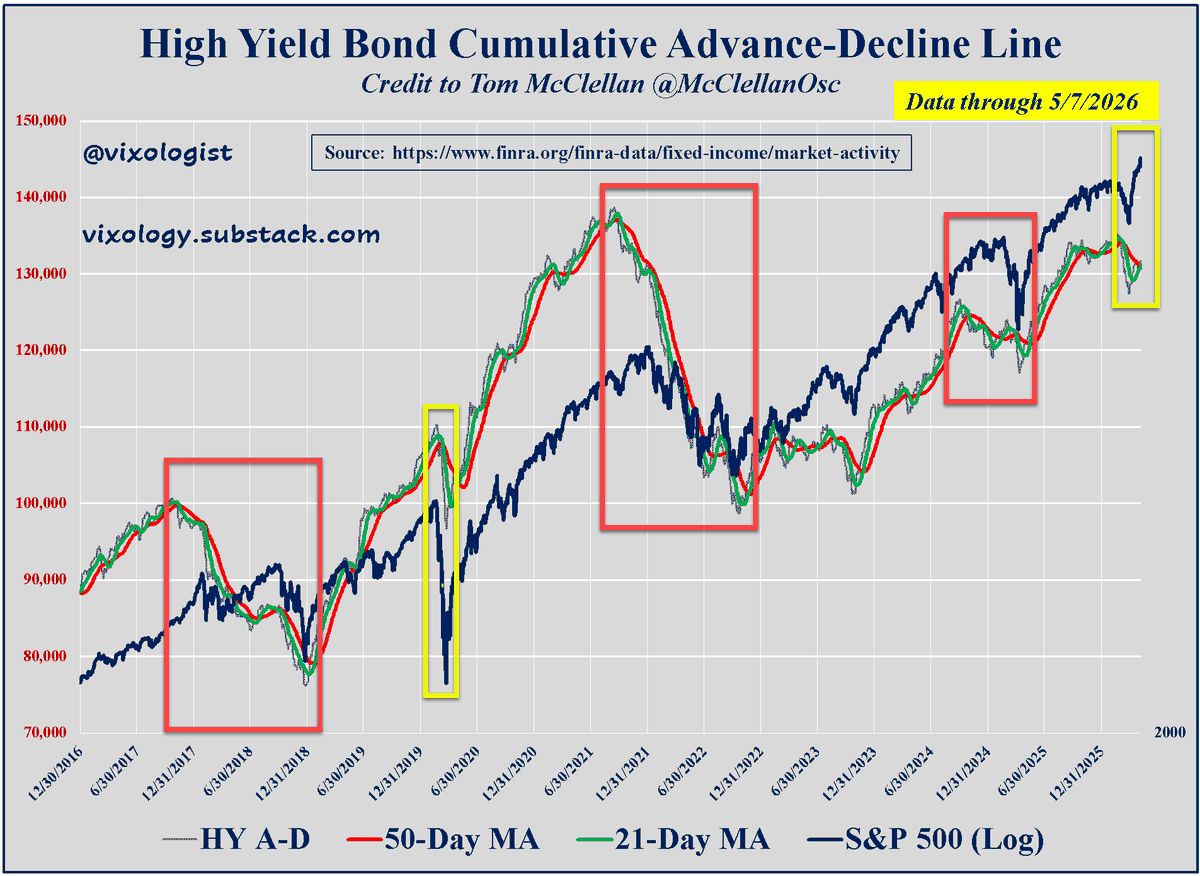

Tom clued me into this a number of years ago. Here's a look that goes back farther and highlights a couple of other times when it's been valuable (2018 and 2022). Nothing's perfect but this one should be on your watch list IMO.