@sweatystartup The best explanation that I have heard is that it is akin to Electricity. The end tools need to be developed yet to realize its full potential. The relatively few use cases thus far are very impressive imo.

Not necessarily, but I would much rather have a company gain 7% per year than payout a dividend of 7%.

Dividends are simply a forced return of capital.

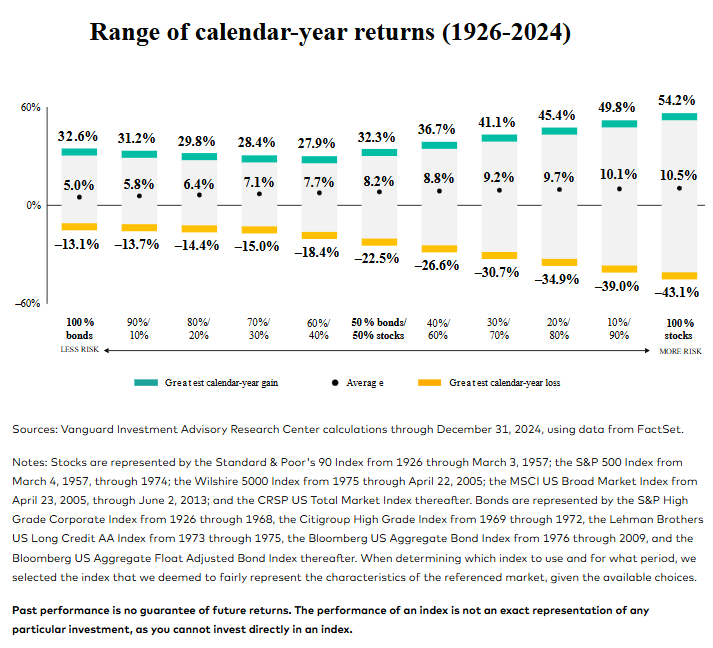

A portfolio consisting entirely of U.S. Treasury Bills can actually be more risky than an all stock portfolio.

Sounds counterintuitive, as bonds are generally thought of as "safe".

Risk can be thought of as the possibility of not reaching your goals. Depending on your goals, playing it "safe" and holding all bonds can actually ensure that you will never reach your goals.

Many investors need a minimum rate of return on their investments to retire/maintain their retirement spending. Thus, the least risky route is often to invest in the relatively volatile stock market - which has historically delivered higher average returns.

In short, investing in the stock market, over a long period of time, often provides the returns needed to meet your goals.

#retirementplanning #financialplanning

Underrated aspects of having a wealth management team in your corner:

-immediate access to an advisor as a sounding board year round

-access to the advisors professional network

-beneficiaries confirmed annually

-all account details confirmed at least annually

@JeffBezos I’ve always thought that a straight sales tax and nothing else would be the best system. Of course might be a disincentive towards economic spending and growth.

@dieworkwear On a similar note, most material items cause more stress than they are worth. Extra cars, houses.. all extra things to worry about. Optimize for happiness and peace

One of my favorite planning cases from last year:

-Married couple - unusually high $1.2M AGI.

-Massive tax bill estimated.

-Had charitable giving goals and a Donor Advised Fund (DAF) already set up.

Solution:

-Loaded up the DAF with highly appreciated stocks bought in the early 2000’s that had become concentrated positions.

-Donated up to the 30% of AGI limit for deductions in a single year with appreciated securities.

Solved 3 problems at once.

1. Reduced current year tax bill. The entire donation is tax-deductible - in a high tax bracket year.

2. Lowered individual stock concentration without incurring capital gains tax. The charitable organization can sell the stock tax-free.

3. Achieved charitable giving goals in a tax-efficient manner.

#financialplanning #investing

Not sure how this one slipped through the cracks of my reading list in the past, but it has been a great book through the first few chapters! Enjoyable read.

I started a newsletter. Not for the sake of starting a newsletter, but more so for my own mental clarity and a desire to improve my writing skills.

I would appreciate some honest feedback.

Latest article here:

https://t.co/SRY8cl01g3

Todays agenda:

Reviewing a 401(k) plan and a potential $12,000 cost savings to the participants. Annually.

If you are wondering if your 401(k) plan costs are reasonable, DM me. Happy to take a look.

A lot of room for improvement in many of the plans that I see out there. Not only on the fee side, but also the investment selection.