Biggest event of this earnings season is over - NVDA's beat-and-raise. $81.6B rev (vs ~$79B), $1.87 EPS (vs $1.77), $91B Q2 guide (vs ~$86B consensus, $90B whisper). Stock flat

The surprising focus of the call was the added color on CPU, let's talk about that.

Vera CPU: ~$20B in standalone CPU revenue visibility this year. Arm-based. Purpose-built for agentic AI. $200B TAM. Not included in the $1T Blackwell/Rubin figure everyone was already modeling.

This is NVIDIA entering the server CPU market at scale, not as a side project bundled with GPUs, but as a standalone product line with four distinct configurations and every hyperscaler signed up.

The economics pitch: x86 optimizes for dollars-per-core (legacy cloud). Vera optimizes for tokens-per-dollar (AI-native). 1.5x faster per core, 2x per watt, 4x density per rack vs x86. Different architecture for a different era.

Who wins: ARM. Every hyperscaler and NVIDIA designing their own AI CPU chose Arm: Vera, Grace, Axion, Graviton, Cobalt. few keeping x86. AMD still ships EPYC into these data centers, but the design wins for purpose-built AI CPUs are going one direction.

Who loses: Near-term, the agentic CPU demand wave is probably big enough to lift all boats. AMD and INTC server CPU businesses can still grow this year as the overall TAM expands. But CY27 is where NVIDIA's full-scale entrance starts to bite. Once Vera is ramping at volume alongside Rubin, the share shift math gets challenging, especially for INTC, which is already losing CPU share to AMD and now faces a third front from NVIDIA with no competitive GPU or custom silicon to fall back on. AMD gets squeezed on both CPU and inference as NVIDIA gains Anthropic and sweeps MLPerf.

The other number that should be in focus: ACIE (AI clouds, industrial, enterprise) at $37B growing 31% q/q, nearly equal to Hyperscale at $38B and almost entirely NVIDIA-captive. Custom silicon doesn't play here.

Vera Rubin ships Q3. Jensen says supply constrained through its entire life. Anthropic now a strategic partner from ~zero. Every frontier model on NVIDIA.

Also notable: Jensen name-dropped UBER (Robotaxi fleet across 30 cities by 2028), CDNS, and SNPS (accelerating EDA tools for CUDA/GPU) as key partners in the agentic and physical AI stack.

The stock traded flat. The fundamentals didn't.

Amazing! Yes, that would be a welcome feature as well. But more generally would be good to just be able to track multiple lists of stocks in the watchlist feature and have an easy way to manage bulk or individual changes. Your news summary features very powerful for those lists of stocks

Weekly Markets Note 1/18/2026

Macro

Geopolitics remain front and center. Trump escalated rhetoric around Greenland, announcing new tariffs on eight NATO allies, explicitly tied to opposition to his aim to purchase Greenland. European leaders warned of a dangerous downward spiral in relations, with protests in Nuuk and Copenhagen and emergency EU ambassador meetings set to take place ahead of Davos.

At the other end of the globe, Canada’s Prime Minister Mark Carney struck a deal with Xi Jinping, opening the door to Chinese EV imports under a low-tariff quota, increasing competition to the US auto industry in Canada. It signals a pivot toward deeper China ties as US tariff pressure reshapes global trade dynamics.

On the economic front, US macro data remains steady. December CPI came in at 2.7% YoY, unchanged from the prior month. Retail sales beat expectations, jobless claims stayed low, and Atlanta Fed GDPNow for Q4 was revised higher to ~5.3%, indicating growth and stability. Bank earnings last week were mixed but generally solid. Rate-cut expectations have moderated, with CME FedWatch showing ~30% odds of an April cut and June more likely.

On Fed leadership, Trump signaled reluctance to move Kevin Hassett into the seat, boosting odds for Kevin Warsh, who now leads on Polymarket. Attention now turns to Davos, where tariffs, geopolitics, and policy will dominate discussions.

Crypto

Crypto policy hit turbulence. The Senate’s “Clarity Act” stalled this week and Coinbase CEO Brian Armstrong withdrew support, calling the latest draft worse than the status quo. Concerns centered on restrictions around tokenized equities, limits on stablecoin rewards, and provisions that could allow banks to crowd out competition. The Banking Committee markup was delayed, with hopes for a reworked version.

Jefferies announced they removed BTC from their model portfolios on the back of pressure tied to quantum computing risks. Investors want to see more progress from the bitcoin developer community on quantum-resistant encryption as quantum capabilities continue to advance.

Semiconductors

TSMC delivered another strong quarter, reinforcing the AI-driven semiconductor cycle. The company guided to ~32% revenue growth in 2025 and raised 2026 capex meaningfully to ~$52–56bn. That keeps the wafer-fab equipment (WFE) upcycle intact across deposition, etch, patterning, and metrology.

Management highlighted robust hyperscaler demand, noting it has spoken directly to “customers’ customers” to validate capacity needs, after a period of hesitation amid concerns about over-investment in a historically cyclical industry. Capacity constraints at leading-edge nodes remain the key bottleneck, and signals from hyperscalers suggest end demand is firmly there.

AI Infrastructure

AI’s collision with energy markets is becoming increasingly apparent. The Trump administration is pushing to shift grid-expansion costs onto large datacenter users and encourage “bring your own power” solutions for hyperscalers until infrastructure catches up. Microsoft set an important precedent, committing to a “pay our own way” model that covers elevated electricity and grid-upgrade costs for its US AI datacenters, avoiding pass-through to local ratepayers. Trump publicly praised the move as a template for others, as political pressure builds around datacenter expansion and rising energy costs. Datacenter energy infrastructure players and neoclouds responded positively on the news, as it becomes clearer that hyperscalers alone cannot meet near-term compute demand and that power availability, land, and local regulation all matter in the infrastructure buildout.

Meta is going all-in AI, launching “Meta Compute” to scale tens of gigawatts of infrastructure this decade, with ambitions to reach hundreds of gigawatts long term. Infrastructure is being positioned as a core strategic edge in the race toward superintelligence, backed by major energy deals and direct involvement from Zuckerberg. At the same time, Meta has shifted away from its open-source Llama roots toward proprietary frontier models, including Mango for image and video generation and Avocado, a reasoning-focused LLM.

Inference continues to become increasingly important and competitive. Following Nvidia’s late-2025 ~$20bn Groq deal for non-exclusive LPU licensing, OpenAI announced a major multi-year partnership with Cerebras to secure up to 750MW of ultra-low-latency wafer-scale compute rolling out from 2026. The focus is on faster responses and real-time AI as the market pivots from training toward high-volume, low-latency inference.

Software

Software and SaaS stocks continue to bleed and remain under pressure as AI disruption weighs on the durability of traditional business models. The market is struggling to form a positive outlook given the impact of inference costs, agents, and the ongoing enterprise shift toward build-versus-buy decisions, leaving uncertainty around where value ultimately accrues.

Anthropic continues to gain share across LLM usage. Claude now leads OpenRouter by token usage, ahead of Gemini, GPT, Grok, and several Chinese models. Reports suggest Anthropic is exploring a $25bn+ raise at a ~$350bn valuation, with a potential IPO in 2026–27. OpenAI also appears to be shifting strategy, previewing ad-based monetization after previously calling ads a last resort, highlighting the growing pressure to improve unit economics amidst increasing competition.

*Market commentary for informational purposes only. Views are my own and not investment advice.*

Weekend thoughts on the markets 1/10/2026📉

Macro

Last week’s US labor data came in a bit soft, but the underlying picture still looks stable. Headline non-farm payrolls rose by 50k in December, below the 70k consensus. Despite that, the jobs market still feels tight, essentially stuck in a “no hire, no fire” mode. Initial jobless claims ticked up but stayed below expectations, reinforcing the idea that conditions are steady rather than deteriorating.

Growth expectations remain strong. The Atlanta Fed’s GDPNow tracker is running near/above 5%, pointing to solid momentum in the US economy. AI-driven productivity gains and tariff-related front-loading effects are likely providing near-term support and could set 2026 up as a strong year of economic growth.

The next test is inflation, with CPI due Tuesday. A benign print would further support expectations for rate cuts, while a hotter number could push timing back. That said, Trump has been clear about wanting lower rates, and with a new Fed chair coming, pressure for easier monetary policy looks set to build regardless of the data. Markets price the next cut for April/June. Speculation continues around the Fed chair, reportedly a battle between Kevin Warsh and Kevin Hassett. Polymarket odds remain close, but once they move decisively, we will likely have our answer. Trump’s announcement this week pushing Fannie Mae and Freddie Mac to buy up to $200bn in mortgage bonds would also help push long end yields lower.

Equity market breadth continues to improve. Performance is becoming less concentrated in the Mag 7, with Schwab calling this a “stock pickers’ market” as leadership broadens across sectors.

Macro and geopolitical risks remain elevated. Rising instability in Iran, reports of hypersonic missile use in the Russia-Ukraine conflict, post-Maduro Venezuela, and renewed focus on Greenland are all adding noise and energy volatility. The bigger macro wildcard may be tariffs. An upcoming Supreme Court ruling that forces reversals or refunds could create real market disruption.

Other policy headlines are also driving sector moves. Trump’s comments around a 10% consumer credit incentive could support retail spending and add fuel to growth, though potentially at the expense of banks and card issuers. With bank earnings coming up, management commentary here will matter. Trump’s comments about banning corporate ownership of single-family homes pressured private-equity-linked real estate names like Blackstone. Separately, his proposal to raise the 2027 US defense budget from $1 trillion to $1.5 trillion sparked another leg higher in global defense stocks.

Factors

On the factor side, higher beta and higher volatility stocks continue to lead. Momentum is still working. Small caps also caught a bid over the past week, with a noticeable resurgence in small-cap growth. The market feels less concentrated and more rotational, consistent with the idea that we’re moving deeper into a stock pickers’ market, potentially driven by dispersion across macro, geopolitics, and a rapidly evolving tech landscape.

Crypto & Blockchain

Bitcoin has recovered modestly over the past couple of weeks, bouncing off holiday lows and reflecting a slightly more risk-on tone. Nothing euphoric, but sentiment feels more constructive than it did into year-end. There’s also some speculation around US involvement with Venezuelan-linked bitcoin, though that remains more narrative than catalyst. It highlights interest in bitcoin at the sovereign level as a strategic asset, somewhat akin to gold or oil (i.e. countries having reserves), though obviously the nature of the digital asset is very different. The market itself remains in wait-and-see mode, with upcoming crypto ETF launches and regulatory developments in DC, including the market structure bill.

Tokenization continues to be one of the more interesting long-term themes. Prediction markets, tokenized equities, and blockchain-based settlement all point to how financial infrastructure could evolve. Coinbase rolling out stock trading and prediction markets directly inside its main app is another signal that the lines between traditional finance and crypto continue to blur.

US spot crypto funds saw net outflows again last week, extending a trend that’s been in place for roughly three months. That likely reflects profit-taking and tax-related selling in Q4 rather than a collapse in conviction in the asset class.

Internationally, South Korea announced plans to allow spot bitcoin ETFs later this year as part of a broader digital asset push. Another reminder that adoption is progressing globally, albeit at different paces.

Technology & AI

CES (Consumer Electronics Show) was the big tech event drawing investor attention this week in Las Vegas. Firms showcased their latest technology, with Jensen Huang (Nvidia), Lisa Su (AMD), and other executives delivering keynotes. Investor focus was on the rollout of next-generation chips like Nvidia’s Vera Rubin and AMD’s MI455X, as well as the ecosystems surrounding them. Nvidia continues to lean into its full-stack approach, expanding deeper into networking and systems to internalize more value and extend its edge in “AI factories.”

Leaders continued to cite robust demand and incremental upside tied to both physical AI and agentic AI workloads. OpenAI co-founder Greg Brockman highlighted the ongoing supply-demand squeeze for compute, reinforcing that AI infrastructure buildout momentum remains strong. Bank of America’s semiconductor note echoed this, pointing to tight availability of datacenter land and shells, which may help explain recent support in neocloud names alongside strong earnings from Applied Digital.

Memory was also back in focus. Supply remains tight, with Micron pushing to all-time highs on strong demand for high-bandwidth memory and DRAM. Other players across the memory stack including SanDisk in flash and Seagate and Western Digital in HDDs and SSDs continue to benefit as AI models require more data to be moved at faster speeds. This ties directly to inference efficiency, which has become increasingly important. Google’s Gemini models running on TPUs have pressured parts of the GPU ecosystem, helping explain Nvidia’s recent partnership with Groq around LPUs and proprietary SRAM technology to gain an advantage in inference and edge workloads. Nvidia is still the clear leader in AI model training.

Beyond the keynotes and chip rollouts, CES also had a strong focus on what many investors are calling “physical AI” - advanced robotics with embodied intelligence. Humanoid robots like Boston Dynamics’ Atlas were on full display. Hyundai shares jumped on the back of this as the majority owner of Boston Dynamics, and as the company stated plans to deploy humanoid robots in factories between 2028 and 2030. ARM also announced moves toward launching a physical AI unit, while Mobileye announced acquisition of Mentee Robotics. It’s an interesting shift as AI capabilities continue to improve and move closer to real-world and edge deployment.

Another major announcement was Nvidia’s move deeper into autonomous driving with the launch of its Alpamayo AV reasoning stack. This narrative potentially alleviates some pressure on Uber and Lyft, while increasing pressure on Tesla. Analysts increasingly see Uber and Lyft as asset-light fleet managers in an AV world, where proprietary AV technology sits with players like Tesla or Waymo. With Nvidia stepping in to offer the software layer, AV technology may become more democratized, allowing more economics to accrue to platforms that offer ride marketplaces rather than owning the underlying technology directly. Nvidia’s continued robotics push also appeared to add pressure on Tesla’s humanoid ambitions. Robotics, AI, and AV are becoming highly competitive areas, with some of the world’s best firms involved. Google remains a major competitor as well, with Waymo scaling and Gemini set to be the “brain” behind Boston Dynamics’ Atlas.

Overall, CES helped reinvigorate AI market momentum, but not in the same way we’ve seen in the past when gains were concentrated in mega-cap hyperscalers. Dispersion across the AI value chain continues to increase. Recent strength in semicap names and constructive outlooks into 2027 have kept investors bullish. Goldman Sachs remains constructive on the group, driven by AI node transitions in both logic and memory, alongside rising volume needs. Advanced packaging also remains tight, with CoWoS capacity shaping who can actually ship AI silicon at scale.

Other areas such as optics have also performed well over recent quarters. Investors remain constructive, though valuation concerns are creeping in and require more selectivity. The memory market also suffers from this valuation concern, as well as other areas like energy infrastructure. That said, the AI infrastructure tailwinds remain strong, with announcements like xAI confirming another big order for natural gas turbines from Doosan Enerbility to power their massive data-center buildouts.

Software continues to lag. We did see a brief spark in cybersecurity this week, but AI disruption across SaaS business models is still playing out, even at very cheap valuations. 2026 is expected to be the year of AI agents, and while rollout is underway, meaningful adoption for software companies requires absorbing inference costs into COGS. That pressures margins, fundamentally changes business models, and weighs on valuations in the near term. High stock-based compensation in some names also continues to dilute investors and drag on cash flows.

In private markets, the picture looks different. AI software is scaling at an unprecedented pace, with several companies reaching $100m in ARR within just a few years. Teams are building apps with tools like Claude Code and scaling rapidly. The software landscape is changing quickly, with AI pressuring incumbents in the public markets.

A few other things I’m watching: Google Gemini continues to take user share from OpenAI’s ChatGPT, though Nvidia Vera Rubin-trained models rolling out in the second half of the year could shift momentum again. It remains important for ChatGPT to show strong revenue growth to support its infrastructure spend commitments. OpenAI is also working to expand monetization -integrating ads, rolling out ChatGPT Health for medical questions, and partnering with early players like Shopify and Stripe to enable in-app purchases. Still early days, with product and data challenges to work through, but directionally important.

*Market commentary for informational purposes only. Views are my own and not investment advice.*

This is a big test of the narrative in Bitcoin

If it breaks higher on fiscal woes and higher long bond yields, it is a BIG litmus test passed here

Let's see

Weekend thoughts on the markets 5/18/25 📈:

Markets started the week on a positive note after the U.S. temporarily paused tariffs on China, lifting sentiment and equity markets. May CPI data showed a continued slowdown in inflation, easing concerns that tariffs would immediately drive prices higher. Economists still caution that inflation could still pick up in May or June as the full impact of tariffs filters through. Rate cut expectations from the Federal Reserve were dialed back slightly.

Walmart’s earnings call reinforced this inflation concern. Management noted they expect tariff-driven price increases in the near term and plan to pass a meaningful portion on to consumers.

Another key development this week was President Trump’s tour through the Middle East, where he announced over $600 billion in investment commitments across the Gulf region. A notable example came from Saudi Arabia, which struck several strategic deals spanning AI and defense infrastructure - including agreements with Boeing, GE, and NVIDIA. The deal with NVIDIA highlights the growing demand for AI infrastructure not only at the corporate level but increasingly at the sovereign level as well.

We’ve also seen signs of continued demand in recent mega-cap tech earnings, where firms like Meta are continuing to ramp up capex for datacenter infrastructure. A PM I spoke with this week was constructive on the outlook for AI infrastructure - particularly advanced memory like HBM (high bandwidth memory), which complements GPUs, TPUs, and other computing chips central to AI training and inference.

Google CEO Sundar Pichai, in a recent podcast appearance, spoke about the transition from internet search’s ‘10 blue links’ model to a more conversational, AI-native interface powered by LLMs. Google appears well-positioned given its custom-designed TPUs and the hardware-software alignment that helps reduce inference costs as demand continues to scale. Even amid antitrust scrutiny, the company seems equipped to compete with OpenAI, whose $300B valuation is partially held by public shareholders via Microsoft and SoftBank. Interestingly, some market participants believe that in the event of a breakup, a ‘sum of the parts’ scenario could actually unlock additional value for Google.

Elsewhere, Microsoft announced layoffs of roughly 3% of its workforce - focused on reducing layers of middle management. This appears to reflect a broader trend of operational efficiency driven by AI. Personally, I’ve found a ~30% productivity boost from these tools - something that, if scaled properly across organizations, could translate to significant cost savings and margin improvements for early adopters.

Despite the strong week for equities, Friday brought a notable development. Moody’s downgraded U.S. sovereign debt from AAA to Aa1, the last of the three major ratings agencies to do so. The rationale was straightforward - successive administrations have failed to rein in growing deficits, exacerbated by growing interest costs. The same day, the House Budget Committee failed to advance the Trump administration’s latest fiscal bill, which, according to the Joint Committee on Taxation, would add another 1.1% of GDP to the deficit, on top of a level approaching 7% of GDP, a level typically seen only during recessions or wartime.

The concern is that the U.S. risks entering a debt spiral and foreign investors begin to question the reliability of U.S. Treasuries as the choice ‘risk-free asset’. We’ve already seen some capital repatriation since ‘liberation day’, and Treasury yields have remained elevated.

Higher yields are now a function of both perceived default risk and inflation risk (as well as growth concerns). History shows that countries often try to ‘inflate their way out’ of high debt loads, which adds another layer of complexity for bond investors - even if yields appear attractive on a nominal basis relative to recent years. It’s clear we’re in a new market regime, and investors may need to stay nimble.

Where are now, three key themes stand out:

· Inflation and hard assets: Inflation risks remain elevated - driven by tariffs, fiscal deficits, and structural shifts in bond markets. This continues to challenge the role of U.S. Treasuries as a safe haven, especially with currency volatility eating into real returns for foreign investors. In this context, gold and bitcoin, which are both near all-time highs, have shown resilience and continue to serve as potential hedges.

· Quality equities still matter: Despite macro headwinds, equities - particularly high-quality, dividend-paying companies with strong cash flows - have continued to perform well. Businesses able to defend margins and sustain growth through this cycle remain compelling in a higher-rate environment.

· AI infrastructure buildout continues: Demand for compute, datacenter capacity, and advanced chips shows no immediate signs of slowing. From sovereigns to hyperscalers, investment in AI infrastructure continues. Recent developments suggest we’re still in the early stages of a broader transition - one that includes robotics and software built on top of these AI foundations. The long-term growth narrative remains intact, with strong signals pointing to continued growth over the next several years.

Sunday Reading📖:

Software multiple compression - cloud update: https://t.co/bcsZeIHXr8

What big tech is saying about tariffs:

https://t.co/deRMeM6wNB

Bessent wants yields down - US Treasury's tools for the yield curve if the fed is slow to act:

https://t.co/KMhCm53TyM

Hedge fund buyers increasingly important as source of treasury demand; leverage leading to volatility:

https://t.co/Jhmiaut0WK

Sharing a few interesting stories from past few days for your weekend eyes on markets 👀

Bitcoin decoupling from stocks- notable shift from what we have seen recently https://t.co/qUl5StPyFq

Return of the bond vigilantes - bond markets push back on tariffs: https://t.co/Onw3HE5XnH

China Tariff Exemptions - some things have limited alternatives: https://t.co/gt5NhVRJGb

Can Lip-Bu Tan save Intel? - turnaround story to watch https://t.co/xUeva4T1rk

Gold and silver divergence - why silver might surprise https://t.co/Ty05KanqFj

Weekly Summary - Mixed earnings this week with indications of weaker consumer demand; upcoming mega cap earnings and jobs report next week to serve as market catalysts

https://t.co/Kc9vFlHMDz

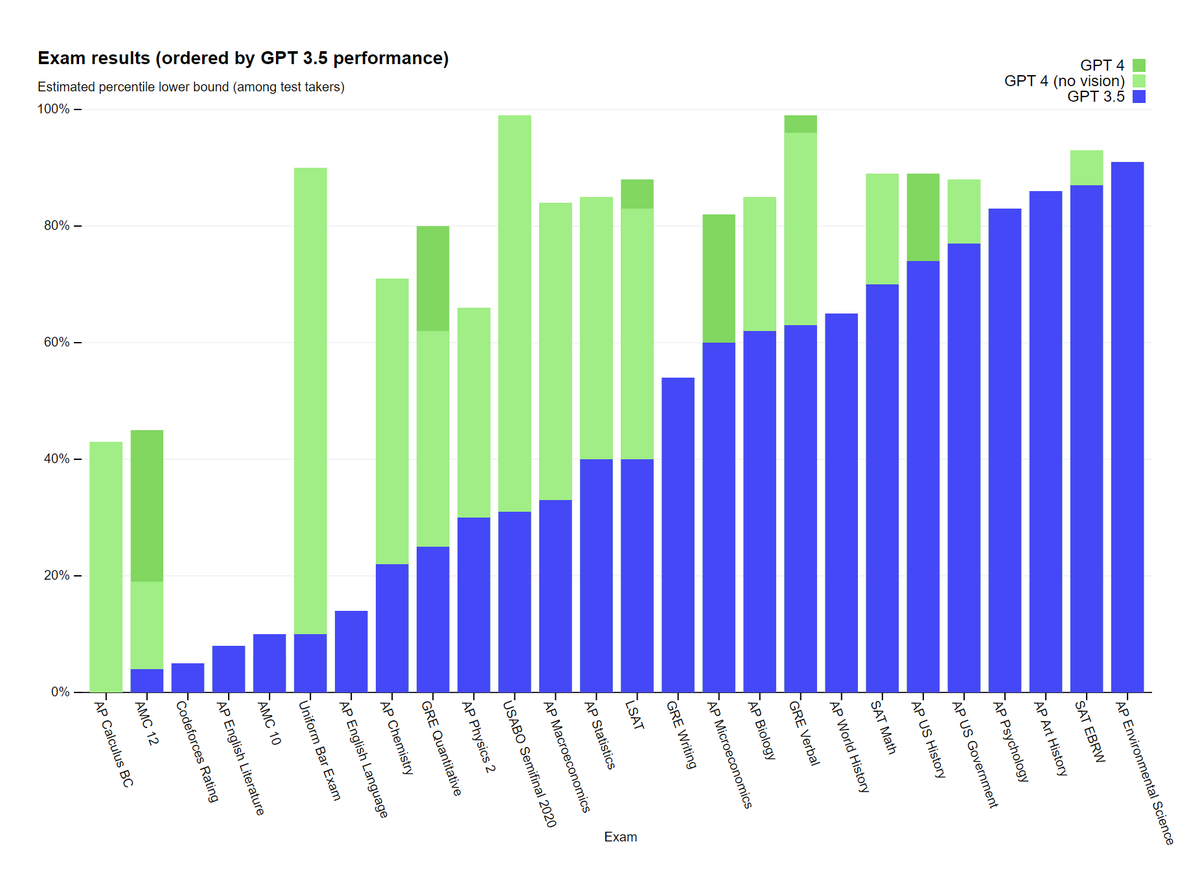

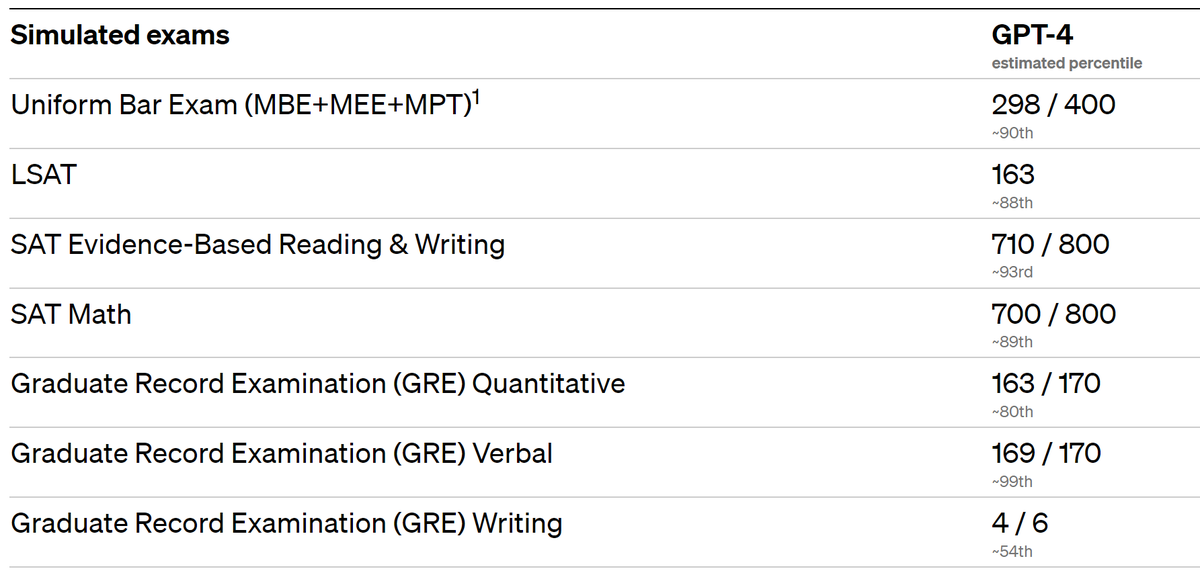

@OpenAI just released GPT-4. Their research shows it got 88th percentile on the LSAT... and also knocked SAT and GRE out of the park #AI#ChatGPT#ArtificialIntelligence

The reopening momentum will likely last a few more months in China. Instant take from Zhang Zhiwei, President & Chief Economist at Pinpoint Asset. He was there when these blowout numbers broke.

Gentle reminder that digital assets often have their own inherent cycles and monetary policy. In #Bitcoin you have the halving cycle, and with #Ethereum you have the merge that took place last year causing very mild deflation - see https://t.co/2iJMlngadx

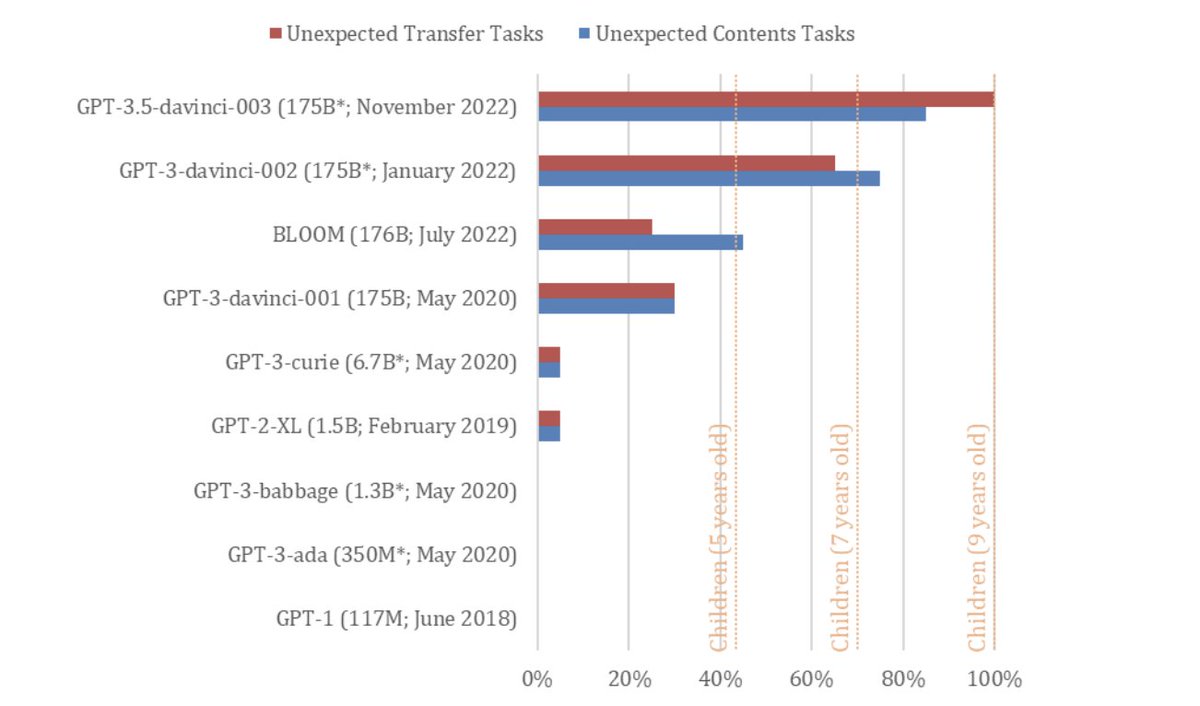

This new study suggests LLMs can now perform theory of mind tasks (ability to understand what others think and believe) as well as 9-year-old children.

Theory of mind was once thought to be a unique human attribute, as well as a few animals.

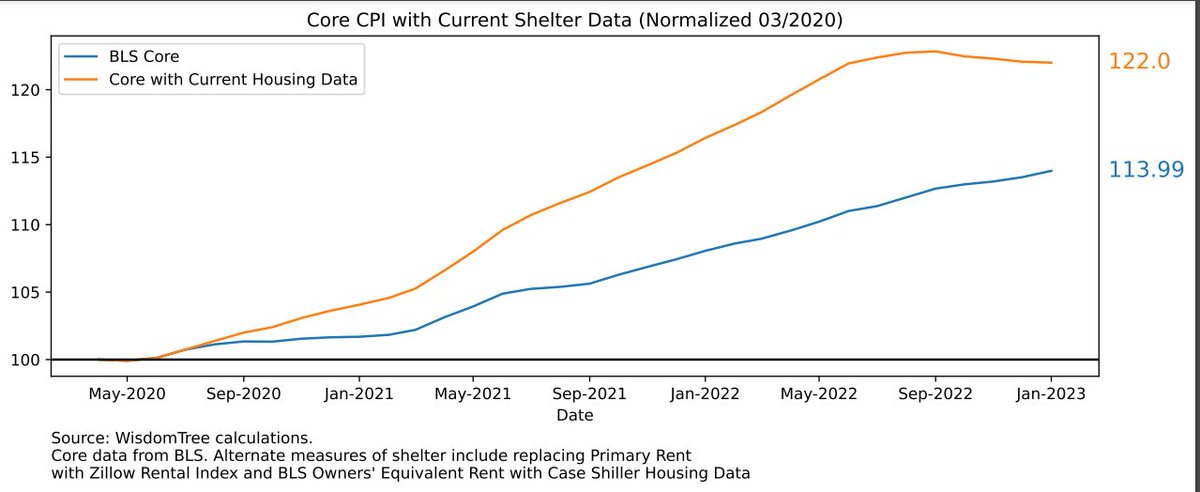

We've had 4 months in a row of negative core CPI prints if one factors in more current housing data.

Last 4m average Core CPI: +0.3%

Last 4m Core CPI w/ Current Housing Data: -0.2%

Inflation Rollin Negative....