@TKopelman You basically answered my question.

On my side we typically include assets like cash, non managed positions in total AUM even though we don’t “manage” it.

@TKopelman@grok Hah lmk what you think @TKopelman .. I’m sick of of this 6% mortgage. Been doing 500 extra a month since I got the home and considering a lump sum versus lump sum recast and just continuing to make same payments.

@TKopelman@grok Does it make sense to do a recast and continue making same monthly payments prior to recasting. Will I pay off my mortgage faster doing that rather than just doing a lump sum and not recasting?

If you got a $1mil mortgage at 6%

Then in the first 5 years, 81% of the payments you make will go to interest

If you increase it to 7%, then 85.5% of your payments would go to interest

This is exactly why buying a home is not a good move in the short term

You front load interest, have closing costs, etc.

And then when you sell you have more costs

Buying wins in the long term, but rarely in the short term

Dangerous things happen when you only look at financial decisions through the lens of tax savings

Taxes matter, of course, but they are just one piece of your financial plan

Focusing solely on deductions, credits, or write-offs can lead to decisions that actually reduce your long-term wealth

The bigger goal is maximum wealth, not minimum taxes

Every decision should be evaluated by how it impacts your overall financial picture, not just the number on your tax return

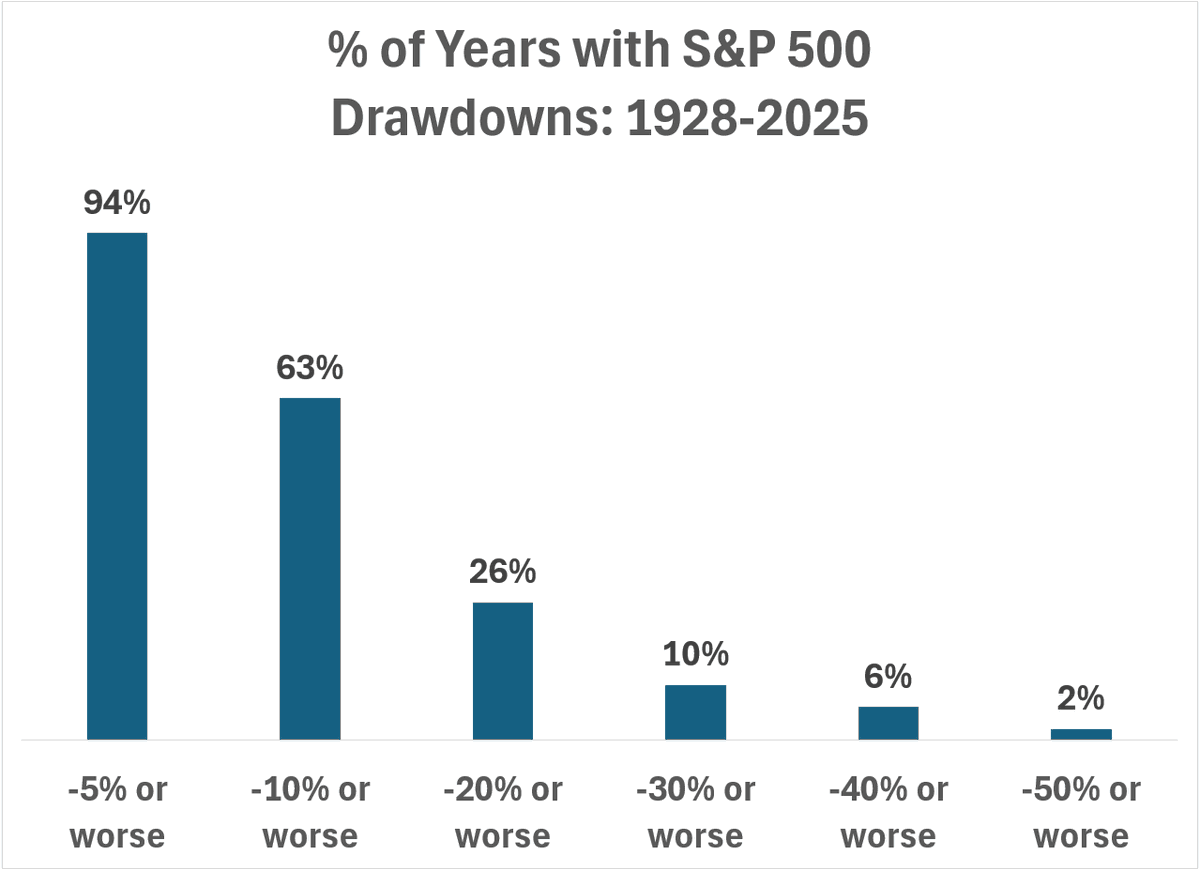

How often S&P 500 drawdowns occurred in a given year since 1928:

-5%: 94% of all years

-10%: 63% of all years

-20%: 26% of all years

-30%: 10% of all years

-40%: 6% of all years

-50%: 2% of all years

https://t.co/aDaCdrPCq3

Financial planning is not an expense

It's an investment in your current and future self

To help you:

- become more educated

- free up more time

- feel more confident in the decisions you are making

- avoid mistakes

- reduce your tax liability

- etc

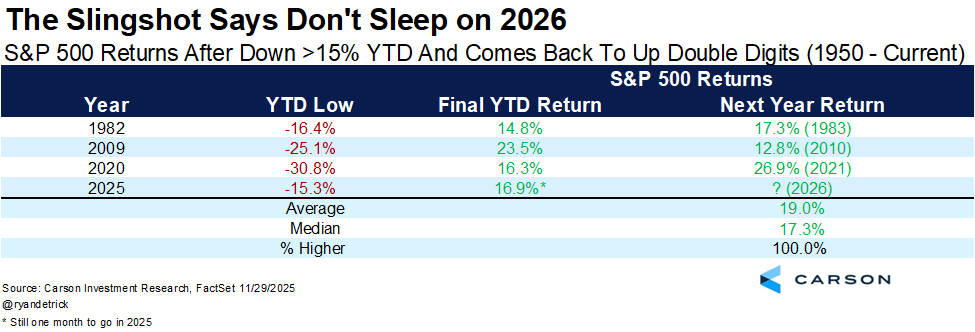

S&P 500 down 10% YTD at some point and finishes the year up >15%?

Good chance it happens this year for only the 4th time ever.

The slingshot effect is real, as the next year was up at least double digits each time and up 19% on avg.

How often does stock market decline?

1% drop: 50-60 times a year

3% drop: 7-8 times a year

5% drop: 3-4 times a year

10% drop: every 1.1 years

15% drop: every 2 years

20% drop: every 3 ½ years

25% drop: every 5-7 years

(S&P 500 avg since 1928)

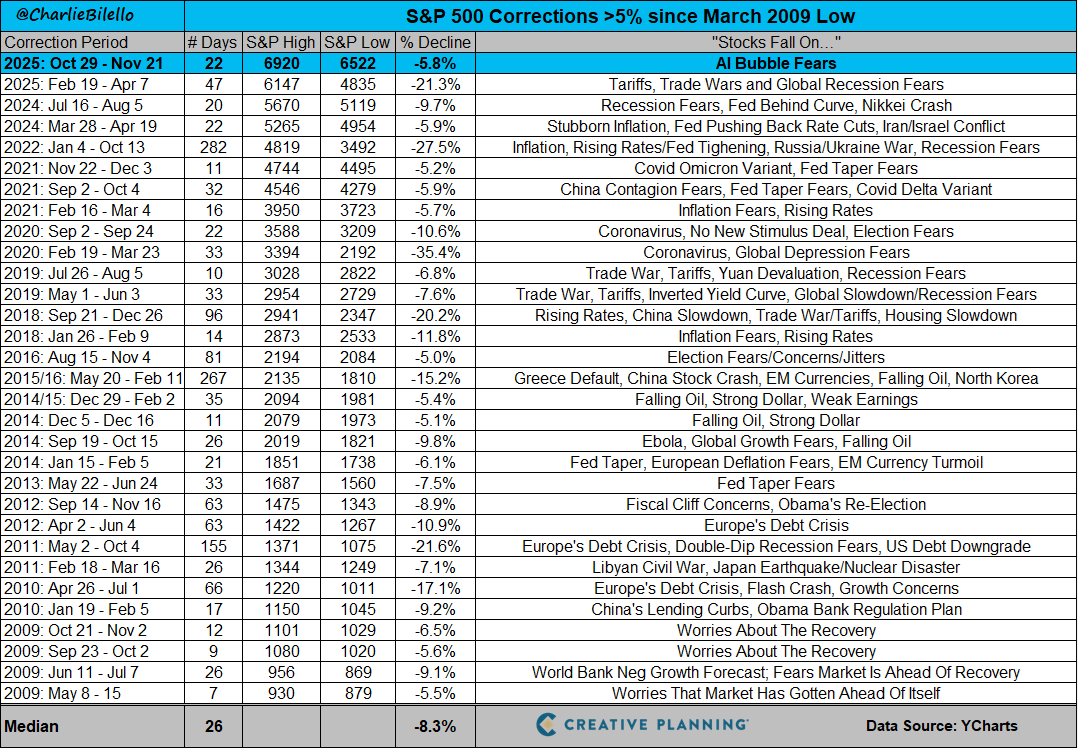

At today's low, the S&P 500 was down 5.8% from its Oct 29 peak, the 31st pullback >5% since the March 2009 low.

Each one came with a scary headline.

Each one felt like the end of the world.

And yet ... the world didn’t end and the market eventually recovered to hit new highs.

I’m a financial advisor and I probably look at stock prices less often than the average person

Investing isn’t about the price today

It’s about 10, 20, or 30+ years from now

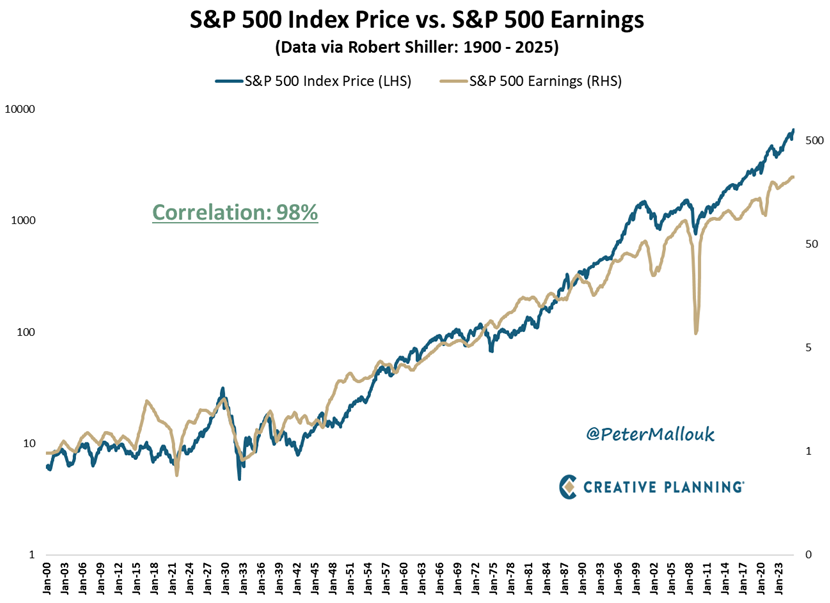

125 years of market history tell a simple story...

Stocks and earnings move together with a 98% correlation.

The short run is all about noise.

The long run is all about profits.

Speculators chase noise. Investors follow profits.

A good financial advisor is:

-a teacher

-a listener

-a guide

-an accountability partner

-a friend who truly cares about your success

- a coach

- a therapist

- an unbiased third part

- someone who should challenge you

- there for you in the biggest moments/decisions

Splitting investments between you and a financial advisor to “see who does better?”

You are not testing performance

You are setting up a competition you are guaranteed to lose

Here is why it is a bad idea: