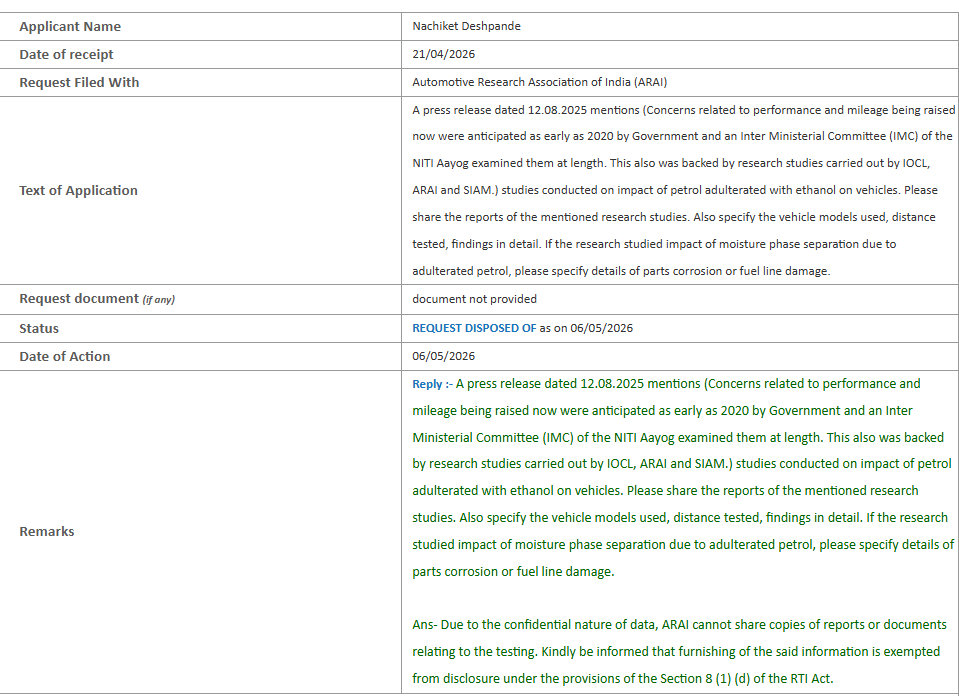

First, the Ministry of Petroleum sits on my RTI for 2 months. Then, they play a shell game, deflecting it to ARAI and OMCs. Now, ARAI hides behind "confidentiality" to suppress the research reports.

If the Govt cited IOCL, ARAI, and SIAM studies in their press release to push the E20 mandate, why is the data now a state secret? What’s "confidential" about mileage drops and engine corrosion?

This isn't about trade secrets; it’s about a total lack of accountability. The refusal to share reports only confirms the suspicion: the Ministry lied in their press release, and the "extensive research" is a ghost. Millions of vehicle owners are being used as guinea pigs for a policy backed by zero transparent science.

@PetroleumMin@HardeepSPuri@arai_india@siamindia@IndianOilcl

In my latest @bsindia piece, following an Indianomics discussion with @latha_venkatesh and Mridul Saggar, I argue that while sharpening and articulating India’s growth story is critical, policy and market distortions may also have amplified negative sentiment around the INR and deterred capital flows.

Key points:

• No cause for panic: INR weakness warrants attention, but India’s external deficits remain manageable and RBI's buffers are substantial.

• The deeper issue: India’s prolonged struggle to attract sustained net foreign capital amid persistent negative sentiment on the rupee.

• Policy silos: Interest rates, liquidity, taxation, capital flows, and currency markets are deeply interconnected, though policy debates often treat them in silos.

• Unintended consequences: Interventions to suppress interest rates, alongside tax frictions, may have unintentionally weakened capital inflows and lowered the cost of speculative positioning against the rupee.

• Distorted savings: Distortions in taxation and markets have also stunted debt market development, pushing discretionary savings disproportionately into equities.

• Navigating the Trinity: The answer is not avoiding intervention, but engaging more holistically with the “impossible trinity” linking interest rates, exchange rates, and capital flows.

• The structural fix: Rather than introducing capital controls or fresh distortions, responses should aim for deeper debt markets, balanced taxation, and a globally competitive framework for foreign capital.

The piece argues against both panic and rigid orthodoxy, in favour of a more integrated approach to monetary, currency, and fiscal policy.

https://t.co/ud4pLWvj2Q

@vivbajaj In a airport checkin queue, I did a count around me. Of 25 people, 22 were overweight.

I have done this in malls...routinely get numbers higher than 70pc.

Qsr and pharma has a long way to go.

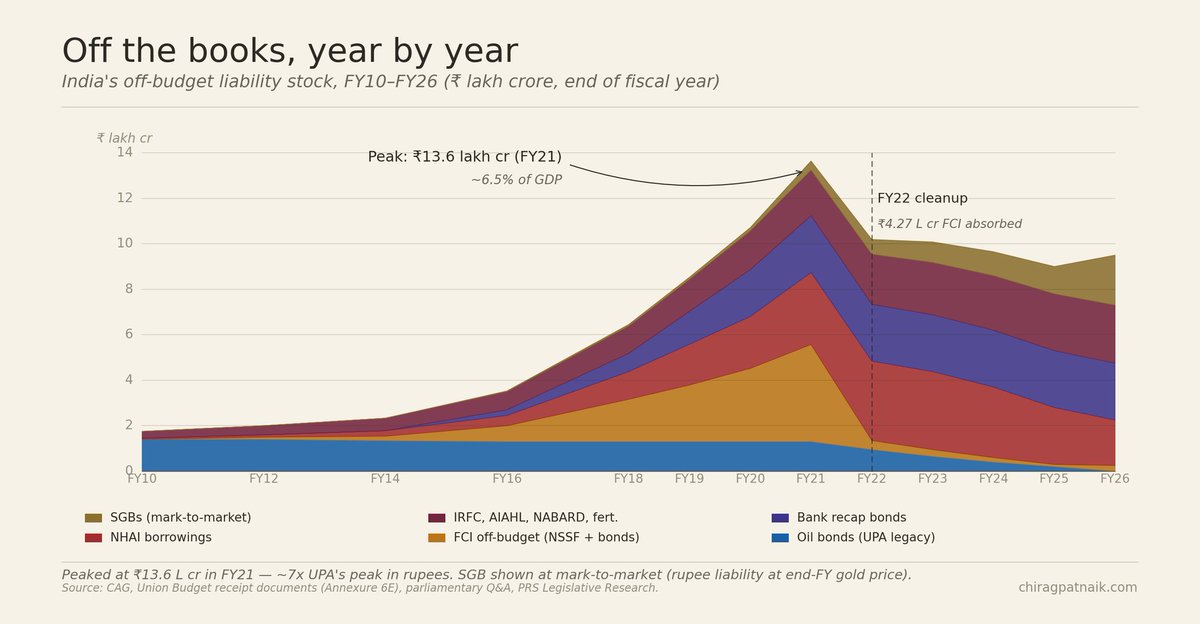

India's off-budget borrowing, FY10–FY26. - Flat under UPA.

Steep buildup through Modi-1 and Modi-2. Peak ₹13.6 lakh cr in FY21.

Still ~₹9.5 lakh cr off the books today.

https://t.co/fY9O4PFzGS

Conclusion

Indian stock markets exhibit no statistically significant response to insider trading enforcement, in contrast to the negative abnormal returns documented in the US and UK. This result is robust across SEBI final orders and SAT appellate decisions.....

Do read

Arjun Gupta, Sonam Patel and Renuka Sane have a pretty article on The Leap Blog, 11 May 2026, measuring the stock market impact upon firms where SEBI issues insider trading orders. Before you peek, ask yourself, what do you expect will happen?

https://t.co/ZuuOzD2pCx

This shortage is falling disproportionately on poor/migrants. As this report for @carboncopyinfo found, they are now paying global rates for LPG -- because they buy from private LPG bottlers -- while the middle class gets subsidised LPG. https://t.co/0w98KfyDIq

In all the debate on international investing vs. investing in India, it is a bit amusing to hear takes in media and influencers where "international = US exposure". This framing itself is wrong. There's way beyond the US or Korea or China even.

Yesterday, I spoke with the CEO of a mega fleet, who said most of his truckload business was doing well, except for one segment: food & beverage.

He called the lack of volume from this segment "unusual."

I told him we believed GLP-1s were causing a significant slowdown in food and beverage shipments, as we had just completed a market study on GLP-1's impact on freight shipments.

Our study, now published in a SONAR Sitrep, available online, estimates that 851k truckloads have been removed from the market due to GLP-1s, and this number could ramp to 1.95m by 2030.

Not only are Americans getting skinnier. Their truckloads are as well.

Probably the best story you’ll read on how India has been managing the energy crises. (As ever, by the seat of its pants, with worse to come.)

Story by Paridhi Choudhary, Shaswata Kundu Chaudhuri, and @mrajshekhar

Cc: @Rory_Johnston@JuneGoh_Sparta

https://t.co/0FkBGHY08i