My company, Newfound Research, turned 15 today.

Coming up on this anniversary, I reflected quite a bit on my career. I’m not sure why, but this milestone feels larger than I would've expected.

So I decided to write something.

15 Ideas, Frameworks, and Lessons from 15 Years

@FactorRoom Yes, because if you have millions of retail users providing non-toxic maker flow, there's no way the makers will want to show up on the other side.

Regardless, worst case the protocol market making vaults can bootstrap maker liquidity.

We’re excited to announce that the Return Stacked® International Stocks & Managed Futures ETF ($RSIT) has crossed $50M in AUM!

Thanks for all of the support.

For more information, visit https://t.co/fRHfN6ooF3

🗣️ @RodGordilloP and @choffstein recently hosted a live deep dive into RSST and RSSY, breaking down where returns came from over the last 12 months, why trend and carry are designed to complement rather than cancel each other, and how each strategy behaves differently across market environments.

The on-demand replay is now available.

Vlad has stated, explicitly in the past, that the expectation with equity investors (of which I am one) is that the value will accrue to the token (https://t.co/5HYDWrdTwX)

And the team explicitly said this at TGE (https://t.co/IDeLKBpQvD) and reiterated it since (https://t.co/IEWnEnr5R8)

The buyback activity to date explicitly supports this stance.

The value created by all Lighter products and services will fully accrue to LIT holders. We are building in the USA and the token is issued directly from our C-Corp, which will continue to operate the protocol at cost.

Box spreads as collateral for what? Your futures contracts? Not explicitly.

You could do something like $75 of box spreads and $25 in T-Bills to run $100 of S&P 500 futures + $100 of managed futures exposure.

I'm seeing 3-month SPX box spread rates at 449bp.

S&P 500 futures are currently around SOFR+95 = 463bp.

Start with a Managed Futures fund.

You put $100 in the fund; the fund will hold $100 in T-Bills and get $100 of exposure to their managed futures strategy (using, say, $20 as collateral).

Let's say we now want to make it S&P 500 + Managed Futures. There's (at least) two ways to add S&P 500 beta in:

1. Use some of the T-Bills as collateral to buy $100 of S&P 500 exposure via a derivative (futures or swap)

2. Use some of the T-Bills to buy physical S&P 500 exposure and then get the remainder through derivatives.

In #1, you're eating the full financing spread in the derivative.

In #2, you're only eating the proportional amount where you're using the derivative.

So, let's say you take $75 of T-Bills and put it into $IVV, getting the remaining $25 of exposure through futures.

Your funding costs relative to someone doing it only with futures is 75% lower.

The trade-off, of course, is that you have less immediate cash on hand to manage collateral needs.

Not wrong – I don't think anyone is doing yield pickup + futures.

But, also, I'm not fully convinced there would be much appetite in the wealth channel.

The complexity/perceived risk of a basis blowout vs the potential bps pickup probably wouldn't get many advisors to adopt it.

@macrocephalopod It does. That's the entire premise between PIMCO's StocksPLUS suite going back to the 1980s.

(I can't tell if you're being sarcastic here...)

In this specific example, we want Equity + Trend.

So you need to get the equity beta somehow.

But, yes, if you think that "Enhanced Cash Idea - S&P 500 Futures Financing > 0" it can make sense to replace T-Bills with the more complicated thing and keep the futures there for beta.

Start with a Managed Futures fund.

You put $100 in the fund; the fund will hold $100 in T-Bills and get $100 of exposure to their managed futures strategy (using, say, $20 as collateral).

Let's say we now want to make it S&P 500 + Managed Futures. There's (at least) two ways to add S&P 500 beta in:

1. Use some of the T-Bills as collateral to buy $100 of S&P 500 exposure via a derivative (futures or swap)

2. Use some of the T-Bills to buy physical S&P 500 exposure and then get the remainder through derivatives.

In #1, you're eating the full financing spread in the derivative.

In #2, you're only eating the proportional amount where you're using the derivative.

So, let's say you take $75 of T-Bills and put it into $IVV, getting the remaining $25 of exposure through futures.

Your funding costs relative to someone doing it only with futures is 75% lower.

The trade-off, of course, is that you have less immediate cash on hand to manage collateral needs.

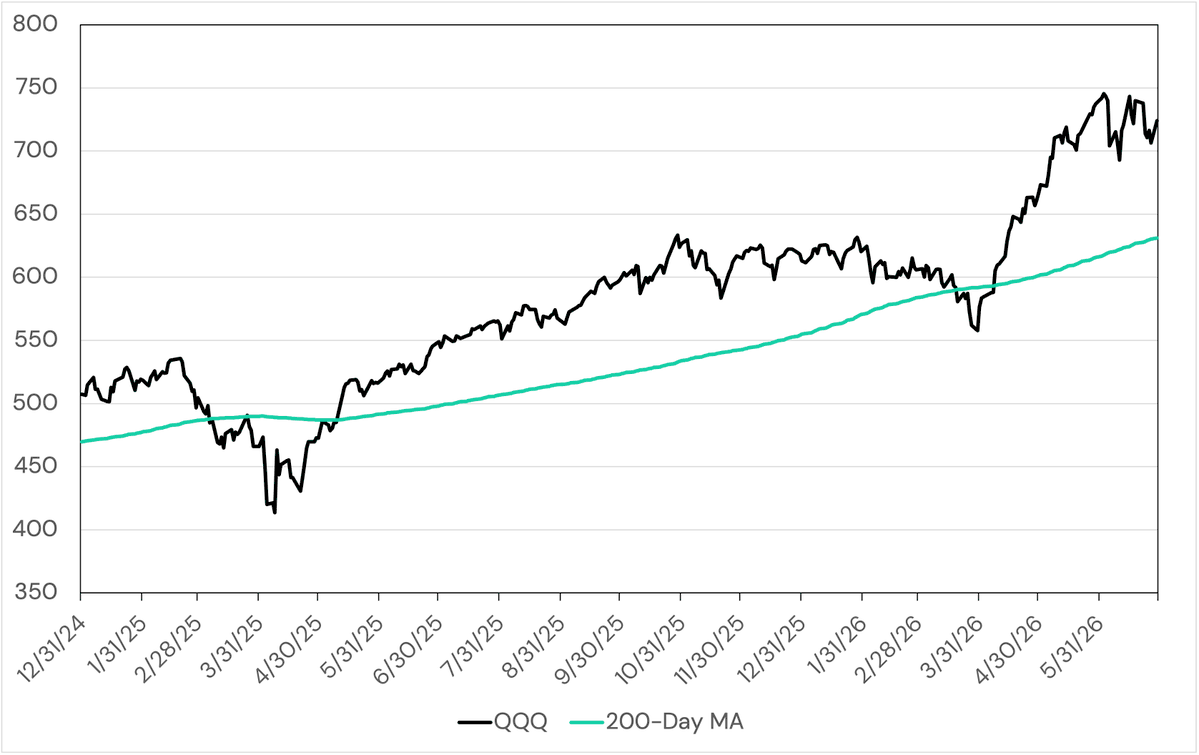

@Ksidiii Okay, you're right – they have come down considerably from where they were a few days ago.

Though, they're still considerably higher than they were a few months ago.

I know it's kind of stupid, but when something is 20% above its 200-day moving average, you'd need to see ~61% annualized return to maintain that distance.

g ≈ 2Y / (N-1)

(g is the daily growth rate; Y is the distance above moving average; N is the length of the moving average.)

1. Balance sheet has a cost

2. The borrow on the single name stocks may be quite high, and variable, creating high hedging costs for the bank

3. Banks can get away with it because the buyers of these products are usually just holding for a very short period of time

With leveraged ETFs gaining a lot of momentum this year, it is important to note the costs outside of the expense ratio.

The cost of leverage can be significant with one fund even financing some total return swaps at 1,950bps + OBFR.

Without taking a look at the holdings, it may not seem nearly as expensive as it really is.