@EdsLFC English soccer / football fans can’t have it both ways. They can’t complain about paying up and at the same time demand top tier talent and facilities.

$4.1B to $39M sounds brutal. But the framing matters. Allbirds the company is dissolving. Allbirds the brand is getting acquired by a firm that buys distressed IP and turns it into licensing revenue. AXNY did the same thing with Aerosoles, Ed Hardy, Born. They don’t run brands. They rent them out. The market didn’t misprice Allbirds at $4.1B. It priced a DTC growth story. That story failed. The brand name is the only part that survived. $39M might be exactly right for what’s left.

72% of fans want free broadcast. 100% of leagues want the highest bidder.

Broadcast was never free. It was subsidized by ads. That model stopped scaling. Now Amazon, Apple, and YouTube are in the rights auction alongside ESPN and Fox.

Fans didn’t lose access because of greed. Leagues just learned what their product was actually worth.

The NFL isn’t launching a flag football league. It’s filing a trademark on the Olympic format before anyone else can. Flag football hits the 2028 Games. The NFL wants to own the rules, the talent pipeline, and the broadcast rights before the world figures out it likes this sport. Silver Lake and Arctos aren’t investing in flag football. They’re investing in the NFL’s international expansion disguised as a startup.

@FOS@readDanwrite Alabama spent $1.2M on private jets. Nebraska spent $1.1M. Both play in conferences that now span the entire country. Conference realignment wasn’t free. The TV money just made the travel costs invisible

@BracketNky The NCAA doesn’t see a dollar of that $9 water. The United Center does. The NCAA is paying them to use the building. What the NCAA gets is the TV deal. Two completely different businesses running on the same court.

@iJordanMoore MLB teams depend on gate revenue more than any other major sport. That is the whole answer. A 1pm Monday game with 15,000 fans is not “exposure.” It is a team losing real money on a revenue stream the NFL and NBA do not need to worry about.

Soccer averages 60 minutes of ball-in-play time per match. FIFA’s target is 64. These rules exist to close that gap.

10-second sub window. 5-second throw-in clock. Injuries treated off the pitch. Every rule maps to the same metric. More minutes of live action per broadcast hour.

This isn’t a rules committee decision. It’s a product spec. FIFA reverse-engineered the rules from a KPI.

And the timed sub rule? MLS invented it. FIFA adopted it for the biggest tournament in history. The league everyone dismisses as minor league is now exporting rules to the World Cup. On American soil.

PBR Teams is three years old and already expanding for the second time. That’s not organic demand outstripping supply. That’s the playbook.

Launch small. Create scarcity. Sell expansion slots at a markup. Use the fees to recapitalize existing owners. Repeat.

They’re not scaling a sport. They’re scaling a format.

The math looks scary until you realize nobody thinks all three IPO in the same quarter.

Spread across 18-24 months at 3-5% float each, you’re looking at $30-50B per deal. The US IPO market absorbed $46B in 2024 alone.

There’s no liquidity problem here. There’s a scheduling question.

Everyone’s talking about 18 games and bye weeks. The real story is the Super Bowl landing on Presidents Day Weekend. That’s the NFL quietly getting what it’s wanted for years: a de facto national holiday the Monday after the game. No act of Congress needed. Just move the calendar.

A 24-team competition across 12 markets with permanent spots and qualifiers. That’s not a league. That’s Champions League for basketball. Which means the real question isn’t who gets in. It’s which current EuroLeague clubs just became mid-table afterthoughts the moment London and Paris walk into the room.

Uber buys Blacklane. Lyft bought TBR for $110M five months ago. Wheely just launched in NYC from London.

Everyone sees a luxury ride-hailing war. The real story is simpler. Uber already won the commodity ride. Growth now comes from moving upmarket.

Blacklane operates in 500 cities across 60 countries with corporate clients already locked in. Pre-booked Reserve trips are one of Uber’s fastest growing segments. This isn’t a car service acquisition. It’s a distribution purchase into the corporate T&E budget, where the buyer isn’t the rider and nobody’s price-shopping.

Three companies all moving upmarket at the same time tells you everything about where the margin is in ride-hailing. And where it isn’t.

The operational story was always the cover. The real return driver was multiple expansion. Buy at 8x, sell at 12x, collect the fee.

2021 vintages got caught when that ended. Meanwhile the S&P is up 50% since then. The debt stayed. The multiple didn’t. LPs are starting to do that math.

@unusual_whales Nicotine in the office is framed as a productivity story. The more interesting angle is employer as supplier creates dependency. That’s a different relationship than employer as employer. Retention has stranger levers than people admit.

Every enterprise tech company has built a consulting arm. Salesforce, Oracle, SAP. The difference this time is who does the consulting. The traditional model is Accenture sending 50 people for an 18-month implementation. The AI model might be 5 engineers who actually understand the product replacing that entire team. AI companies aren't just filling the same gap. They might be eliminating the system integrator layer entirely.

@inpredict 9.2 quintillion possible brackets in a 64-team field. 90% unique out of 20,000 would be hard to avoid. The real question is how 2,000 people managed to submit the same bracket as someone else.

The model isn't the problem. Codex CLI already handles general questions, coding, and everything in between from the same terminal. I mix general questions, general automation tasks, coding, inference on my general obsidian vault, web search all from one codex CLI terminal and it's great. The model is general purpose.

The issue is the app. Codex desktop is heavy, hangs, eats processing power. Meanwhile Anthropic's Cowork runs smooth as a native desktop experience.

OpenAI needs to make the app layer not suck. The model can already do it all. The packaging is what's broken.

Everyone is converging on the same idea from completely different directions.

DoorDash is paying Dashers to strap on body cameras and film themselves washing dishes, folding clothes, loading dishwashers. That footage trains AI and robotics models. 8 million couriers already positioned across the country. Instant physical data collection network.

In southern India, startups run "arm farms" where engineers wear GoPros on their foreheads and fold towels on repeat to train humanoid robots. If a towel takes longer than 60 seconds, they start over. (LA Times documented this late last year.)

1X's $20,000 home robot NEO ships this year. WSJ tested it. It couldn't complete a single task on its own. Every chore was controlled by a remote human wearing a Quest 3 headset.

The pattern is clear. "Physical intelligence" in 2026 doesn't mean robots replacing humans. It means humans doing the work on camera so machines can eventually learn to copy them.

Andy Fang calls it "building the frontier of physical intelligence." Right now that frontier is just a better system for routing humans, collecting their movements, and selling the data upstream.

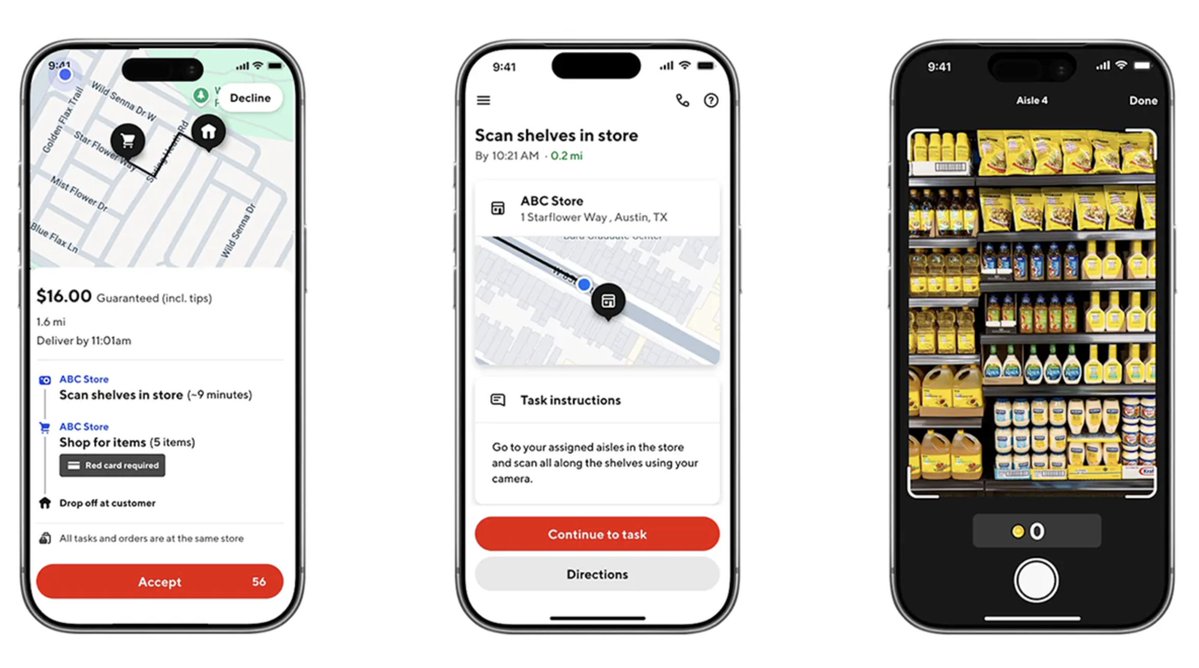

DoorDash realized the delivery network was always the asset. The food was just the first use case.

Introducing Dasher Tasks

Dashers can now get paid to do general tasks. We think this will be huge for building the frontier of physical intelligence. Look forward to seeing where this goes!