Anyone notice that since they changed the name to @X you get a lot more followers like miapoppy who are devoted to all things #investorrelations 😂

"you had me at disclosure..." she was heard to say.

@OtterMarket@iancassel Harris - I follow your sage commentaries on MCC & am impressed. I saw this M&A news from our former client $NNUP - which has been quiet & building a cash hoard the past few years so perhaps worth a closer look? This adds $5M in rev to their $2M base...

https://t.co/JAIcsQqn6H

Spec. Ink Maker $NNUP Fires Up Growth

*Buys Polymeric US w/ >$5M FY26 Rev. for $2.7M - turbocharging its '25 Rev of $1.5M.

*Ex/Bayer Corp CEO Greg Babe named Exec. Director Op's

*Babe & @HorizonKinetics to each invest $200k @ $1.50/share

https://t.co/JAIcsQqn6H

Nice summation of cinema equipment & services provider $MITQ's Q3 Results via @zacks_com

MITQ's Q3 Loss Narrows Y/Y as DCS Audio Sales Gain Traction

https://t.co/E0xQoznUKI @MovingiMageNews

Reminder #23,917: Why you should look into biometric authentication solutions (used by leading global military/defense groups) offered by our client $BKYI @BIO_keyIR - BEFORE the breach!

via @WSJCyber subscription newsletter

https://t.co/TXL1pqSMYt

Long-time client $BKYI is putting together the quarters to reach profitability - while dealing with Nasdaq continued listing issues. $4 share price surpasses $1 min closing bid but missed 10 day requirement prior to May 4th deadline so they are seeking a Nasdaq hearing

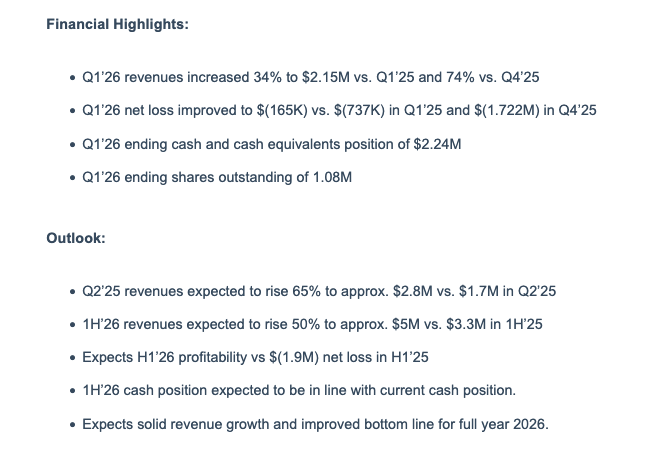

$BKYI @BIO_keyIR Q1 call at 10am ET today

Sees solid traction for biometric identity & access mgmt. solutions

* Q1 Rev +34% w/ strong bottom line improvement

* Sees Q2 Rev +65% and 1H'26 Rev +50%

* Expects 1H'26 profitability vs. 1H'25 $(1.9M) loss

https://t.co/bl7WwhUm01

$MITQ sees initial revenue from its DCS Cinema Loudspeaker line - and expects Q4 Rev's to improve to $5.3M - reflecting seasonally stronger Q4 & Q1 periods.

Moving iMage $MITQ Reports Revenue of $3.39M, Bolstered by DCS #Cinema#Loudspeaker Shipments; Hosts Call Today at 11am ET @SCNmag@AVTechnologyMag https://t.co/wS43Jqde5Y

$ACFN reports Q1 with continued growth in 90%+ margin remote monitoring & control revenue but lower hardware sales due to very large cellphone provider contract benefit in year ago period.

LT track record is very impressive

Call today at 11am ET (yes a client!)

$ACFN Acorn Reports Q1 Revenue of $2.2M with Steady Growth in High Margin, Recurring Remote Monitoring and Control Revenue; Investor Call Today at 11am ET, Dial-in #: 1-800-715-9871 #Generators#Infrastructure https://t.co/TJTcyExKJC

Following $SPCB since Nov. & their electronic offender monitoring biz progress is VERY impressive -

today w/ 4 new county wins in NY. Would love to help them with IR! 😎

https://t.co/E76ResrXlL

I recall when Fed regulation was relaxed in radio broadcasting - setting up a consolidation surge that drove amazing valuation increases...

Wonder how Fed marijuana moves will impact cannabis industry which is constrained by lack of Federal approvals... $MSOS $TLRY $CGC $CRON

Love the $SPCB story - own the stock in the mid $8s and hope they step their IR efforts ; ) to secure a valuation deserved by a rapidly growing recurring rev. business with competitive strengths driving a great record of wins displacing competitors.

$SPCB: I believe SuperCom’s underlying business is growing at a rapid 80% yoy, but this is currently hidden by the accounting of the Romanian contract. Because of specific rules, 80% of that contract’s value was recognized during 2023 and 2024. Let me explain why:

SuperCom uses a cost based accounting method. At the beginning of a contract, they estimate the total cost of the project; they then recognize revenue as a percentage of the costs incurred. Because the company's European contracts are heavily weighted toward the beginning, SuperCom incurs most costs early when producing and delivering hardware. As a result, the majority of revenue is recognized at the start of the contract.

The Romanian contract was worth $33m with a four year duration. The annual report shows a massive jump in revenue and a customer concentration of 50% in 2023 and 53% in 2024. I am confident this customer is the Romanian government. By my calculations, roughly 80% of the total contract value was recognized as revenue in 2023 and 2024.

If we assume that 10% of the contract is recognized in 2025 and 10% in 2026, we can normalize the data. By excluding the 53% from the Q3 2024 YTD figure and my estimate of $2.25m from the Q3 2025 YTD figure, we see adjusted revenues of $10m and $18m. This indicates that excluding the Romanian deal, the company actually grew 80%. This growth likely stems from the U.S. business, as gross margins have expanded from 48% in 2024 to 61% YTD Q3.

I posted a full write-up about SuperCom on my substack. Link in bio

@GagHendo007@Aksel465 Sure seems like there's a great growth story here - that's lost in the noise of the dilution and repositioning of the business on electronic monitoring that was required to create a compelling growth opportunity.