HOLY $SHT.

If there was ever any doubt from all the rumors that $NVDA was a customer… well those doubts are gone.

I just got direct confirmation from the company's own shareholders' introduction presentation.

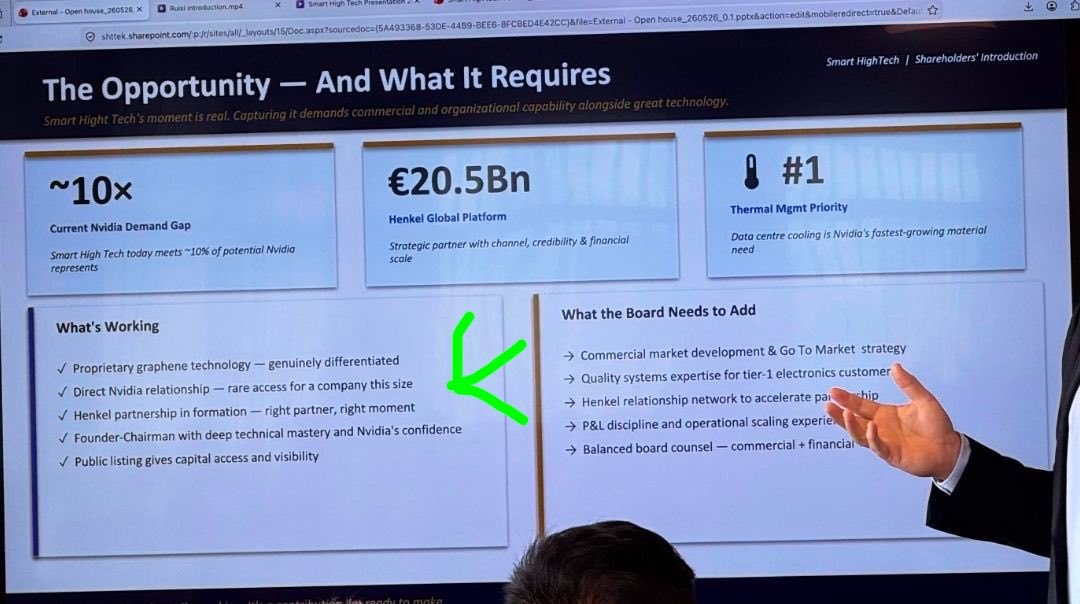

~10x is the gap between supply and current NVIDIA demand gap.

€20.5Bn. That is the Henkel global platform behind them. Channel, credibility, and financial scale.

#1. Data center cooling is NVIDIA's fastest-growing material need. Not a material need. The fastest-growing one.

In the company's own words. "Direct Nvidia relationship -- rare access for a company this size." "Founder-Chairman with deep technical mastery and Nvidia's confidence."

To top it all?

They also have AMD as a customer. Volume orders from AMD since 2024 to integrate SHT's products into their datacenter chips. That is in the public record.

The two biggest chip makers in the word as your customers… 10x demand gap from NVIDIA alone…

Holy sh..t I mean holy $SHT

Do what you want with this information. I am buying and I am holding this for a very long time.

Bullish $SHT.

Not financial advice.

I am long $SHT Smart High-Tech.

I’ve done a much deeper dive in this name and I only like what I find. And now at a much more attractive entry point.

SHT makes graphene-enhanced thermal interface material, GT-TIM, the layer that pulls heat off a chip. As GPUs and CPUs get bigger and hotter, the old two-layer TIM stack cannot keep up. SHT is pushing TIM 1.5, a single-layer replacement that management believes becomes the new standard. The chips outgrew the old solution. SHT built the new one.

Here is why I hold conviction, in order.

One. The progression is real and documented. Prototype orders from Huawei in 2022. AMD choosing GT-TIM for chip test systems in 2024, which means recurring volume across AMD and its contract manufacturers. Thermal Grizzly selling their KryoSheet into 90-plus countries. A second US electronics giant approving them. Then Henkel, deepening from MOU to strategic partner to onsite audit to approved TIM supplier. Three years of climbing, step by step, from development company to commercial company. I read the whole timeline and it holds together.

Two. Henkel is the tell. Henkel did over $20B in sales in 2025. For a company that size to enter a strategic partnership with a Swedish micro-cap, commit internal resources and capital, and help navigate brutal qualification processes, without seeing a very large commercial opportunity, is difficult for me to believe. Henkel will sell SHT material under the Loctite brand. They do not attach that brand to a science project. That single fact carries a lot of my conviction.

Three. The NVIDIA angle. And I want to be precise. It is not in an official press release. But in the last presentation, Professor Johan Liu, the founder, executive chairman, and the key technical mind behind this company, pointed directly at NVIDIA as the customer they are working toward and are approved by. Michael Quail, a career Henkel executive now on the board, said the same at the AGM. Liu went further, that liquid metal does not work for NVIDIA, that competing solutions show problems, that NVIDIA wants full module solutions including GPU. The NVIDIA angle has been hinted at the whole time. Hearing the founder point at it this directly was the moment it clicked.

Four. The recent hard catalysts. First delivery to a world-leading AI hardware company on May 25. End-customer approval passed. A $300K prepayment inside a $5M 2026 framework.

Pre-confirmation I would have rated this case 7 to 8 out of 10. With these developments I am at 9 to 10.

The obvious risk.

One -- SHT has struggled with production before. The whole bet now comes down to one question. Can they manufacture at scale and meet demand? They have an automated China factory at 35,000 units a month approved, machines built for 100,000 units each, and management calls the setup a gold mine. Scale it and the upside is extreme. Stumble on the ramp and that is the ceiling.

Two -- Dilution. Governance concerns were raised at the AGM over a recent directed share issue. Capital will be needed and dilution is a real risk.

I’m long because the technology is validated, the partnerships are real, a $20B partner is putting its brand on the line, the founder is pointing at the biggest customer in AI hardware, and the first deliveries are already out the door. That is an asymmetric setup.

Execution is everything from here. But I want to be positioned before the ramp proves out, not after.

Asymmetric upside. Execution is the whole bet. This name is just getting started.

I’m long $SHT

Not financial advice.

MARKETS OPEN IN 20.

every day is different.

I will post unusual volume as I see it.

I will give long thesis for potential 10x on small caps.

We won’t miss another. Here’s another $DDD

I give ideas on stocks that fly under the radar you won’t see me talking about the names 90% x are on. Be different. Be unique. Be you.

Ideas are ideas. But finding another account working harder

Good luck. 😤

Research 24/7

Scanning charts daily

500% runners & 10x longs

I’m a real person

DMs always open

I’m shouting out legends every day who provide value

I also just unfollowed 117 accounts who didn’t want rock with us.

If you’re working hard and want to be seen and found on here. Follow and subscribe. I’m trying to find new hard workers and legends daily.

Engaging with me means I’ll go straight to your account and do the same and if I like your content I make lists daily to do shouts.

Plus. Alpha. Alpha. Alpha. More alpha

Here’s some accounts you all should look into following

@Edge_Bolt@LeifInvests@rotten_guts5@WolfOfTrenchess@raichutokenized@DorisDi3@wealthyfranklin@perspez@gpaisa7@theFInvestor@enogrowth@kurrensy_trades@Dmytro_Lebid@Billerrr1

Let’s all bank fam. Subscribe for just 1$

The community I’m building here on x will be one to remember. Follow me. Follow the people I suggest to follow. Subscribe. 🏦 BANK.

$DDD is shifting into a high-value manufacturing platform positioned across:

• AI data center thermal systems

• semiconductor capital equipment

• aerospace & defense production

• medical & dental manufacturing

THE NUMBERS THAT MATTER

• Revenue (Q1 2026): $95.5M (+1% YoY, +11% ex-divestitures)

• Healthcare segment: $50.1M (+21% YoY)

• Gross margin: ~35.9–36.1% (expanding YoY)

• Adjusted EBITDA: + $2.1M (from -$23.9M last year)

• Cash: ~$86.5M

• Market cap: ~$350M–$500M range (micro-cap re-rating zone)

WHY THIS STORY IS DIFFERENT NOW

1) AI DATA CENTER COOLING DEMAND IS EXPLODING

AI racks are moving into:

• 30–140kW+ per rack

• liquid cooling becoming mandatory

• thermal engineering becoming critical infrastructure

DDD already works in:

• semiconductor wafer-stage thermal control

• precision fluid manifolds

• vacuum/cleanroom-compatible metal parts

• ultra-high accuracy cooling systems

That directly translates to:

• cold plates

• heat exchangers

• direct-to-chip liquid cooling hardware

2) SEMICONDUCTOR + PRECISION ENGINEERING MOAT

DDD’s advantage is not “printing parts.”

It’s precision thermal + fluid physics manufacturing.

They already solve:

• <4 mK thermal stability systems

• microfluidic channel optimization

• vibration reduction via monolithic metal design

• complex copper and alloy geometries

3) DEFENSE + ONSHORE MANUFACTURING TAILWIND

Exposure across:

• aerospace & defense programs

• U.S. Air Force initiatives

• naval + advanced materials supply chains

• America Makes ecosystem

Trend tailwind:

👉 reshoring + secure domestic production

Defense buyers prioritize:

• reliability

• qualification

• supply chain security

not lowest cost

$DDD fits that model.

4) TURNAROUND METRICS ARE IMPROVING

What changed vs prior cycle:

• Operating losses sharply reduced

• ~$55M cost cuts implemented

• SG&A materially down

• EBITDA inflection achieved

• Healthcare now a core growth engine

5) MIX SHIFT = HIGHER QUALITY REVENUE

Growth areas:

• Dental + MedTech (+20%+)

• Aerospace & defense (double-digit growth)

• materials + recurring consumables

This is a $350–500M micro-cap showing:

• positive EBITDA inflection

• expanding margins

• AI infrastructure adjacency

• defense + semicap exposure

• healthcare growth engine

If execution continues, the rerating case is not about “3D printing hype” — it’s about whether the market starts valuing it as critical thermal + precision manufacturing infrastructure for AI and defense.

$VOO $HIVE $HYLN $VELO $HYFT $CELH $PLTR $HIMS $RDDT $AIB $FEMY $JOBY $TE $SIVE $ZS $MRVL $SNPS $SNOW $DELL $LAES

$APRTE entry swedish stock. One of the lead investors in $SHT.B (up 65% today after my share) also invested in APR Technologies.

APR Technologies is a small-cap Swedish thermal management specialist focused on high-performance cooling solutions for electronics, with relevance to the AI infrastructure boom—including potential indirect exposure to the VR200/Rubin rack power/heat challenges.

APR Tech fits as a speculative Swedish thermal proxy in the broader AI supply chain (alongside SHT.B). It could see torque from liquid cooling adoption trends in Rubin-era racks, but it's earlier-stage with binary risks around customer wins and production scale-up.

$SMOL Smoltek Nanotech Holding AB is a publicly listed deep tech company based in Gothenburg, Sweden, that pioneers carbon nanotechnology for the semiconductor and hydrogen industries.

Their core innovation is a patented technology that makes it possible to grow conductive nanostructures on a substrate in a controlled way, using carbon nanostructures as an assembly platform for advanced semiconductor packaging.

The company operates through two subsidiaries:

Smoltek Semi focused on breakthrough technologies for the semiconductor industry, developing CNF-MIM capacitors ultra-thin capacitors that provide extremely high capacitance in relation to their volume, designed to be placed directly on the underside of chips to maximize chip performance while maintaining stable power delivery. Unlike existing alternatives, CNF-MIM technology uses an additive manufacturing approach requiring fewer production steps, resulting in cost savings and greater design flexibility for next-generation electronics.

Smoltek Hydrogen focused on breakthrough technologies for the renewable energy and hydrogen sector. Their product, Smoltek PTE, is a Catalyst Coated Substrate for PEM electrolyzers that delivers full functionality with minimal precious metal usage. Their carbon nanofiber technology creates a 30× larger active surface area, ensuring nearly all catalyst material actively participates in the reaction cutting iridium use in PEM electrolyzers by up to 95%.

In short, Smoltek is a deep-tech nanotechnology company working on two major challenges: making AI chips faster and more power-efficient, and making green hydrogen production cheaper.

Reliability validated: An independent third-party reliability test of the CNF-MIM capacitor technology confirmed stable performance over 1,000 hours under applied voltage — with zero failures and no degradation in capacitance, equivalent series resistance, or insulation resistance. A follow-up test further confirmed stable performance after 2,000 hours.

Production capacity established: Smoltek has signed several new NDAs with potential industrial partners and established initial production capacity for capacitor prototypes through new ALD equipment and collaboration with ITRI in Taiwan.

Hydrogen expansion: Smoltek Hydrogen was selected as one of nine Swedish cleantech companies to join the Swedish-German Cleantech Platform 2026, aimed at accelerating commercial expansion into Germany's green hydrogen and fuel cell market.

🚨 I’M GOING HEAVY TOMORROW 🚨

Breakout confirmed. Setup is clean.

RT and I’ll send you this ONCE in a lifetime setup.

THIS CAN GO 1750%+ like $CAR

Be ready by 9:25 AM EST. I’m calling it live.

$NOK

Nokia Federal Solutions, Lockheed Martin introduce mission-critical 5G solution for U.S. Department of War open suite of standards.

$NOK is coming back…

$OBDU B gets a big order, they do the same as IQE in photonics, but only 10musd MC.

my favorite stocks in photonics right now is $sive $lpk $obdu B obducat is on the swedish stockmarket