What just happened?

The S&P 500 just erased nearly -$2 TRILLION of market cap just hours after 3rd strongest US jobs report in 18 months.

Meanwhile, Bitcoin is officially down over -50% from its record high in October 2025.

What's happening? Let us explain.

(a thread)

Hi Ranjit Sir

Lately in the last 40-60 days users have reported issues (not fuel economy) from multiple parts of the country and primarily in the North. In Turbo, NA & Hybrids too.

Brands are fixing things under warranty in 1-2 days to avoid panic & social media compliants. Many cars are e20 compliant.

Looks like either percentage of ethanol is silently increased at some pumps or the quality of fuel has gone completely unchecked. Me and Munish are collecting data from customers, service centres & seeing patterns.

Yesterday Mr. Gadkari said he doesn’t want to see the face of Petrol. That tells a lot. Looks like ever since we are buying oil from the US/Venezuela few geopolitical/profit issues have arrived. Can’t comment much on that.

Separate dispensers for e20 and e85 (for flex cars) is a fine solution. But increasing ethanol percentage every 2 years is extremely unfair.

80% of the customers know nothing. Brands will cover them for 3-4 yrs and after that car will start burning a hole in their pocket if blending percentage doesn’t stop at 20%

I've nothing personal against Shamika Ravi. But saying poverty has almost been eradicated in India and justifying all economic disasters is not expected from Prime Minister's Economic Advisory Council.

I don't know how many of you remember Montek Singh Ahluwalia. He was in a similar position in the previous governments. He never used to dress up anything. He was always factual and tried his best to find workable solutions. As a technocrat, his communications were never political.

We need people who acknowledge problems and then work towards addressing them.

3BHKs in Ivy County are listed around Rs 3.2 to 4.1 crore. 4BHKs around Rs 4.8 to 4.9 crore.

Even that kind of money cannot guarantee basic safety for your family.

Crores of net worth turned to ash in the time it takes to film an eight second clip, never mind the risk to the people in those rooms.

India really is Final Fantasy rendered in real life, where you cheat death and destruction at every turn and learn to call it normal.

As recently as 2019, Narendra Modi warned India was facing a “population explosion.” Today, India's total fertility rate of 1.9 is below replacement, and the TFR in major cities like Delhi (1.2) is lower than that of advanced economies.

SpaceX is simultaneously three things

- An extremely profitable and promising space launch and telecom business

- A highly speculative and capital intensive AI firm

- A massive grift using exchanges and retail for exit liquidity

If Rajesh Exports scam is true, 3 massive questions are haunting the govt in its face:

1. Why did LIC invest in it so heavily when all MFs and Insurance companies stayed away

2. Why did major investors leave before retail investors got the news of SEBI action

3. MOST IMPORTANTLY, Rajesh Export did 158 billion USD exports in the last 5 years, if this is not correct, ARE WE SURE OUR EXPORTS NUMBERS ARE CORRECT (on which the govt is basing all its confidence)

Is this is the start of the economic tsunami that’s about to hit us ?

Every new layer in the Rajesh Exports case makes the story look even more bizarre..

On 21st May 2021, Brickwork Ratings downgraded the company from A- straight to D. Not one notch. Not two notches. Directly to default.

Anyone who understands credit markets knows this is not normal. Rating agencies typically take such an extreme step only when they believe the stress is severe, credibility is questionable or there are deeper concerns around repayment itself alongside defaults..

Now think like a normal investor.

If a company gets downgraded to default, most retail shareholders would immediately exit the stock.

But then comes the real shocker.

LIC held roughly 8.86% before the downgrade.

Instead of reducing exposure after a default rating… LIC actually increased its stake to nearly 11.22% subsequently.

Why?

What was the investment thesis after a direct downgrade to D?

What additional comfort emerged post default that justified increasing exposure using public money?

And this is where the larger problem lies with many PSU investment decisions.

There is often no accountability for inaction.

When the stock was trading near Rs 600 even after the downgrade phase, LIC still had ample opportunity to exit and preserve capital. Instead, over the next 4 years, the stock collapsed towards Rs 100 and yet nothing meaningful happened.

Now with SEBI’s explosive allegations around potentially misrepresented revenues running into lakh crores, the situation looks even more unbelievable in hindsight.

This is exactly how public money quietly gets destroyed.

No aggressive review.

No accountability.

No risk management urgency.

No institutional ownership responsibility.

And in all probability, just like several other cases in Indian markets, the holding may simply keep sitting there till it eventually becomes another write off buried inside a giant portfolio.

The Rajesh Exports story is no longer just about one company.

It is equally about the quality of institutional decision making in India.

I valued SpaceX for its IPO a few weeks ago, with minimal information and a promise to revisit the valuation, when the prospectus was made public. The prospectus is public, the offering price has been set and my update is up and running. https://t.co/zRjpD1C0wv

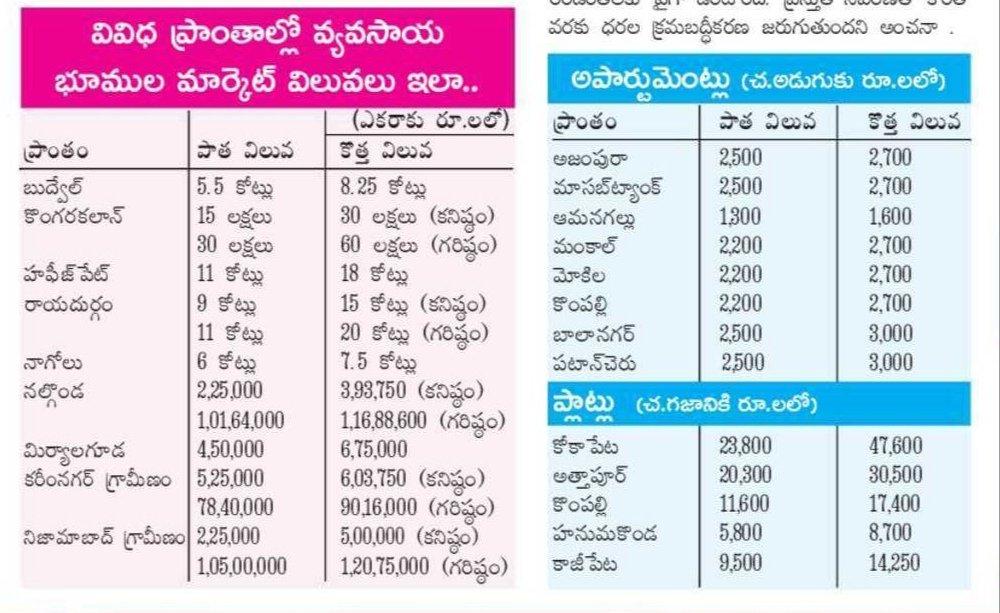

#Telangana hikes property market values

🌾 Farm lands: +50–100% 🏢 Apartments: +10–20% 📍 ORR areas see biggest jump

💰 Land values now range from ₹2.75 lakh to ₹35.29 crore per acre (Begumpet Paigah)

🏘️ #Kokapet plot rate doubled to ₹47,600/sq. yd.

Few revised values👇

India will never produce an NVIDIA, and it has nothing to do with talent. R&D is the purest form of investment, and the central bank has spent decades making investment the dumbest thing you can do with a rupee.

I've been surfing the semiconductor wave for a while now, reading 10-Ks for fun. Spent last month in the Bay Area and the gap between India and the US is not a gap; it's a different universe. Conversations about agentic AI and the next decade of hardware, with my boomer relatives Waymo-ing around SF and self-driving home on Tesla FSD like it's normal. Nobody there thinks any of this is remarkable; they already live in the future.

NVIDIA spends nearly twice as much on R&D as every listed company in India combined. Silicon Motion, the world's leading maker of NAND flash controllers and around since 1995, ploughs 29.7% of revenue back into R&D. Micron runs 10.2%, NVIDIA 9.9%, on revenue bases that dwarf anything we have. India Inc? 0.85% of turnover, and half our listed companies report zero R&D at all.

The easy move is to lambast our promoters and the dhandomaxxing capitalist class, or the foreign MNCs running India as a glorified offshoring unit, or the babus who fund nothing useful. Satisfying. But Wrong. The reason no rational Indian founder pours money into frontier R&D is that there is genuinely no payoff at the end of it. Why?

1. R&D compounds, and compounding punishes laggards. At the edge of science a 1-2% gain is a moat; Intel spent 20+ years performing impossible physics every 24 months because Moore's Law was the business model, and that consistency makes them one of the goated companies of all time even after they got mogged recently. NVIDIA lives the same way today: invent at the limit or cease to exist. If you're 50% behind, no quantum of innovation closes that. You never touch the high end. You stay a mass-market producer of things that already exist. India is precisely there.

2. The supply side is the real thesis, and it's monetary. Two decades of high inflation, high money-printing, high nominal rates. That regime subsidises consumption and taxes patience. R&D is the longest-duration, highest-variance bet on the board; it is the first thing a 8% risk-free rate kills. Frontier R&D only ever gets funded two ways: a psychopathically risk-tolerant capitalist with cheap capital, or a state with Stalin-grade control. The USSR took agrarian peasants to the first man in space in 20 years; China built its own version. India has neither the state capacity, the political will, nor the balance sheet to do that. So nobody does it.

Talent was never the bottleneck. Capital structure was. If you want a SpaceX or a TSMC born here, you need an environment where a conglomerate can deploy $10B and sleep at night: a low-rate regime that makes long-duration investment rational, IP and patent courts that actually function, and policy that doesn't get rewritten every 2-3 years on a minister's whim. Stability is the input. Innovation is the output.

Bay Area versus Bombay, we are several universes apart, and you cannot print your way across that distance; you can only compound your way there, and we've spent years optimising for the opposite. The gap won't be bridged. With luck, it narrows.

🚨Telangana Land Registration Value Revision (Effective June 5)

https://t.co/47Ko6sXFSh

• The Telangana government is revising official land registration values across the state from June 5.

• For apartments within Hyderabad, the increase in registration values will generally be capped at 20%, with some localities seeing only a 10% hike.

• Land values in Fast-growing Hyderabad suburbs within and around the ORR will see some of the biggest increases.

• Agricultural land values in areas such as Tellapur and Shamshabad are expected to double (100% increase).

• In premium locations like Jubilee Hills, the increase will be relatively moderate, with guideline values rising from around ₹80,000 per sq. yd. to ₹90,000 per sq. yd.

• In the Hyderabad Old City, land values are expected to rise by only 10% to 20%.

• In districts such as Warangal and Khammam, agricultural land values are expected to increase by 50% to 70%.

• Rural areas that already have relatively high land values, including parts of Karimnagar, are likely to see only minor revisions.

• A large number of rural villages across the state will see no change, with existing registration values remaining intact

My mind is blown away reading the 109 page SEBI order on Rajesh Exports… not that its surprising given some in last few yrs had called it a fraud but shocked on the size of it and how a Rs 3,000 crore market cap company may potentially be heading towards ZERO.! 😲

This is not a normal accounting issue. This is SEBI practically alleging that out of nearly Rs 15.45 lakh crore consolidated revenue reported over 5 years, close to Rs 15.15 lakh crore revenue itself may have been misrepresented. Yes, you read it right - lakh crore.

And the most shocking part?

The core operating subsidiary, Valcambi SA, whose numbers supposedly drove the entire global scale of the group, reportedly showed only a few hundred crores of standalone revenue annually in audited Swiss accounts. Meanwhile, the holding structure above it magically showed revenues running into several lakh crores.

SEBI’s allegation is brutally simple in layman terms: A refining business which allegedly earned only processing charges/value addition was shown at group level as if the company owned and traded the entire value of gold flowing through the system.

Imagine a toll booth operator claiming ownership of every car crossing the highway and booking the value of all cars as its own revenue. That is broadly what SEBI is questioning here.

The order repeatedly mentions:

• No proper invoices

• No customer/vendor level breakup

• No ERP access

• No journal dumps

• No confirmations

• Missing subsidiary financials

• “Swiss confidentiality laws” being cited to deny information

SEBI has also highlighted that even the forensic auditor BDO India faced severe non cooperation.

What makes this even more serious is that this is an ex parte interim order. Meaning SEBI has passed the order based on its own investigation and material gathered, without relying on cooperation from the company side. Regulators generally do not go this aggressive unless they believe the findings are extremely serious.

The statutory auditor named in the order is BSD & Co, a mid sized Bengaluru based audit firm along with P V Ramana Reddy & Co. SEBI has specifically mentioned non submission of working papers and missing subsidiary records.

Another fascinating angle:

The annual reports reportedly show borrowings of around Rs 1,000 crore, but there is very limited clarity on which banks gave these loans and against what underlying audited cash flows.

This may go down as one of the most dramatic accounting fraud allegations ever seen in Indian capital markets post Satyam..

If even a fraction of SEBI’s findings sustain, this is not just a corporate governance failure. This is a complete collapse of reported financial reality.

Absolutely insane reading.!

You can read the order here - https://t.co/RWP594BT2r

#Rajeshexports

#Hyderabad IT corridor rents are up 10–20% YoY.

📈 2BHK rents: #Madhapur ₹22k–38k, #HiTec City ₹28k–42k, #Gachibowli ₹22k–35k, #Kondapur ₹18k–40k. Premium gated homes now command ₹50k–70k/month.

🚇 Many professionals are opting for shared housing or 1–1.5 hr daily commutes.

Miracles of New India

Rajesh Exports showed 99% fake revenues, totalling more than Rs.15 lakh crores, from 2021-25. That's a cool $150 billion at least.

The SEBI has reported major accounting fraud at Rajesh Exports, including a reported ₹15.15 lakh crore revenue misstatement during FY21–FY25, linked to unverified overseas entities. Perhaps 97%–99% of revenue was inflated! SEBI has barred promoter-chairman Rajesh Mehta from stock markets. LIC holds ~10% stake in this firm, despite a steep fall in the stock.

[a question I had, which experts may comment on - would this scam have impacted India's overall exports numbers (year-wise) also?]

Every few weeks there is a debate on why India's manufacturing share isn't taking off.

Before discussing labour laws, land, logistics or social harmony, consider this:

The OECD estimates that subsidies explain 22% of market share gains for growing firms globally.

For Chinese firms, the figure is nearly 60%.

That is not a marginal advantage. It is the game.

A new OECD study covering 525 major firms across 15 industrial sectors found Chinese manufacturers receive 3–8x more government support than firms in OECD countries and substantially more than firms in countries such as India, Brazil and Indonesia.

On average, Chinese industrial subsidies were around 2.5% of annual revenue over 2005-24 and exceeded 3% of revenue in 2024. Most competing regions were below 1%.

In key sectors the numbers are even larger. Chinese semiconductor firms have at times received subsidies approaching 10% of revenue. In automobiles, Chinese firms received roughly 4x the subsidy intensity of OECD competitors. In aerospace, Chinese firms often received 2-5x more support relative to revenue.

The result is visible everywhere.

Between 2005 and 2024, China massively expanded its global share in solar panels, shipbuilding, steel and aluminium. Aluminium alone went from roughly 24% of global production to nearly 60%.

India is therefore not competing against a free market.

It is competing against one of the largest industrial subsidy systems in modern economic history: cheap capital, state banks, state-owned enterprises, tax concessions, grants and below-market financing all working toward the same objective.

Could India simply copy this model?

Probably not.

A Chinese-style manufacturing strategy ultimately means large transfers from households to industry through cheaper capital, directed lending, lower returns on savings and sustained state support. Democracies find it much harder to sustain that bargain.

The question is not "Why hasn't India become China?"

The question is:

How much manufacturing can India build while preserving democratic accountability, fiscal stability and household welfare?

Viewed from that angle, India's gains in electronics, mobile phones, renewables, defence manufacturing, rail equipment and semiconductors look less like failure and more like progress against a very strong tide.

Thankful to Rajeev for cutting the BS and saying it as it is.

When some of us pointed this out over the years, we were balked at as being anti biz commies or just jealous. And of not being live players. Only those outside who find the gate keeping know how it feels inside.

A PM who wants to leave a lasting legacy on economic growth and revival must work to rekindle the culture of entrepreneurship by having a policy and action basis for new entrants over entrenched players. Yet to see it in the scale and form that’s necessary to move the needle.