MS on $GEV:

"Our view remains that gas turbine industry orders decrease in 2027 (vs 2026 levels of ~117GW). This view is driven by (1) an already high level of behind the meter gas turbine data center orders relative to build rates, and (2) our view that Middle East power infrastructure investments may see some delays"

"But, any way you cut the data, the Gas turbine market looks balanced at best in 2030, and more likely it starts to look over-supplied into the 2030"

So SemiAnalysis dropped a headline that looks bearish for memory, and everyone is misreading it. $MU

The claim: NVDA is cutting Rubin NVL72 SOCAMM DRAM from ~55TB to ~28TB per rack. Most Rubin systems move to 96GB modules instead of 192GB. Rack cost drops from $7.6M to $6.8M, TCO from $4.16 to $3.90 per GPU-hour.

Surface read: they are halving the memory. Sell memory.

Here is the part most people get wrong.

SOCAMM is LPDDR5X. It is not HBM. The thing they trimmed is the commodity DRAM bolted to the Vera CPU.

The HBM4 on the actual Rubin GPU is untouched, still 8 stacks, 288GB per GPU. The high-margin link in the chain did not move an inch.

So why cut at all?

Because memory is the current bottleneck and NVDA knows it.

SemiAnalysis has SOCAMM contract pricing near $8/GB in 1Q26, a sharp step-up driven by the LPDDR5X surge and broad DRAM tightness.

When your input is scarce and repricing higher every quarter, you ration it. You spec it down. You manage TCO.

That is not demand weakness. That is a buyer flinching at how tight supply is.

→ NVDA still calls SOCAMM a $300B TAM. They are managing specs inside a shortage, not walking away.

→ The cut is on the cheap DRAM. The scarce, sold-out, margin-rich part is HBM, and that allocation is locked.

→ MU confirmed its HBM4 36G 12H in high-volume production for Vera Rubin. At GTC Taipei NVDA named all three suppliers. SK Hynix takes the largest share, Samsung next, MU the smallest slice. But MU is in the build.

The frame I keep coming back to: the bottleneck moved from chips to memory, and the durable one is power.

This SOCAMM story is NVDA actively managing the memory link. You do not manage what is abundant.

The risks remain:

→ $MU is the smallest of the three on Rubin HBM4. Share, not access, is the open question.

→ If LPDDR pricing is what NVDA is really pushing back on, that pressures commodity-DRAM margin even as HBM holds.

A headline that screams bearish is NVDA confirming memory is the choke point.

They cut the cheap stuff and protected the expensive stuff.

That is the whole tell.

JUST IN: GOOGLE $GOOGL JUST ANNOUNCED AN $80 BILLION CAPITAL RAISE TO BUILD AI INFRASTRUCTURE

And Berkshire Hathaway $BRK.B is writing a $10 billion check to get in.

Here's the full breakdown:

THE DEAL:

- $30B in underwritten public offerings

- $40B through an at-the-market stock program starting Q3 2026

- $10B private placement to Berkshire Hathaway

THE BERKSHIRE PIECE:

- $5B in Class A Common Stock at $351.81 per share

- $5B in Class C Capital Stock at $348.20 per share

- Berkshire has been building this position since Q3 2025

THE PURPOSE:

- Scale AI compute infrastructure to meet "unprecedented customer demand"

- Approximately $30B of the ATM proceeds will cover 2026 employee equity tax obligations

- Remaining proceeds go directly to AI infrastructure buildout

JPM talks about datacenters not coming online in 2027, and delays, but no one has mentioned the reasons behind it, and as a reporter, I cannot let this go.

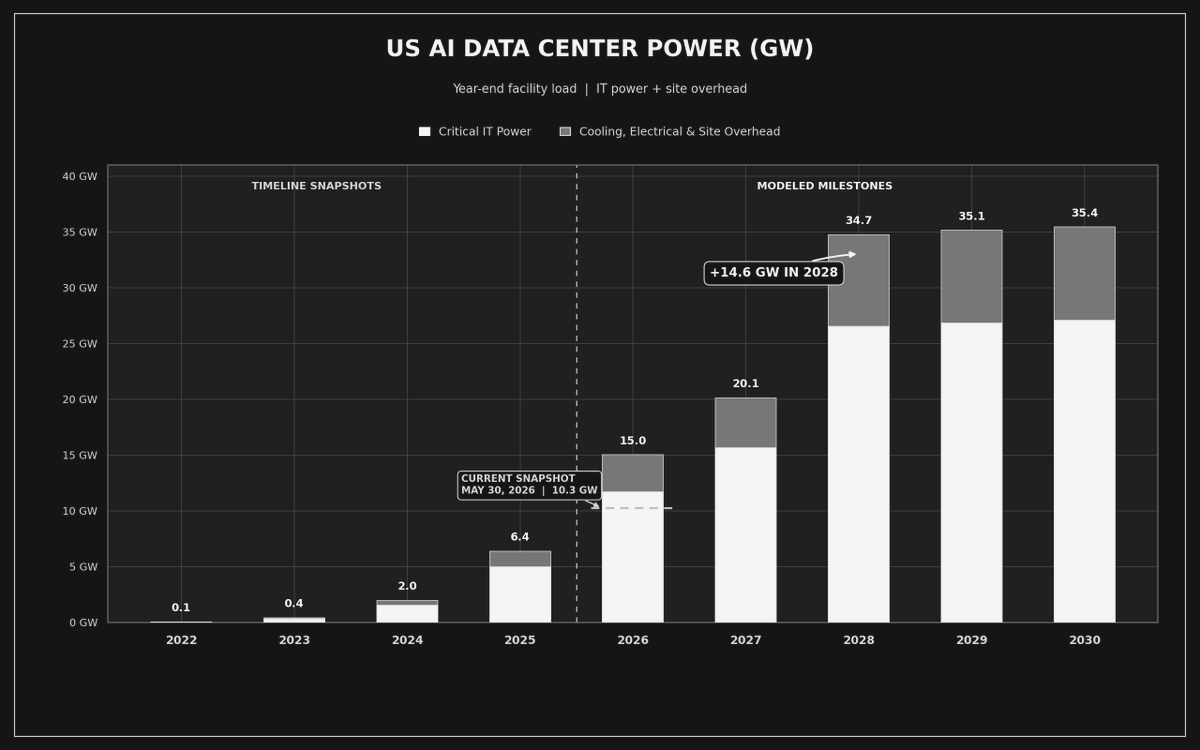

I tracked Epoch's most recent DC data release, and some of the information on power usage has surprised me a lot:

- At the modeled completion, tracked data centers are rising in power usage from 10.3 GW to 35.4 GW, and the 3x increase in consumption is coming just by 2028. And, a huge chunk of this modeled power consumption is accounted for by data centers that are directly accessing the US grid.

- Many of the completed data centers are waiting on substations, transmission lines, cooling equipment, or utility load delivery. And 67% of the US pipeline comes from greenfield sites with zero operational power today.

So, this makes one thing clear: the biggest threat to datacenter buildout is energization, and regulatory compliance as well. Not CapEX/hyperscaler funding, or shortages.

Taiwan is now deeply tied to AI — and it can no longer get off this ship.

According to Goldman Sachs, Taiwan’s AI industry contribution to GDP growth has already far exceeded that of the United States and South Korea. The core reason is that Taiwan sits at the heart of the global AI supply chain. From foundry manufacturing and advanced packaging to AI servers and the HBM supply chain, Taiwan is capturing almost the full dividend of the AI capex cycle.

If Taiwan wants to sustain the strong economic momentum of recent years, the global AI investment boom cannot stop. Today’s Taiwan is no longer an economy supported mainly by traditional domestic demand or real estate. Increasingly, the entire society is beginning to revolve around AI infrastructure.