What happens when your data team stops using AI as a tool and starts using it as infrastructure?

In our latest blog, the Securitize data team explains how they embedded AI into their data architecture so every output is governed, auditable, and never leaves their perimeter.

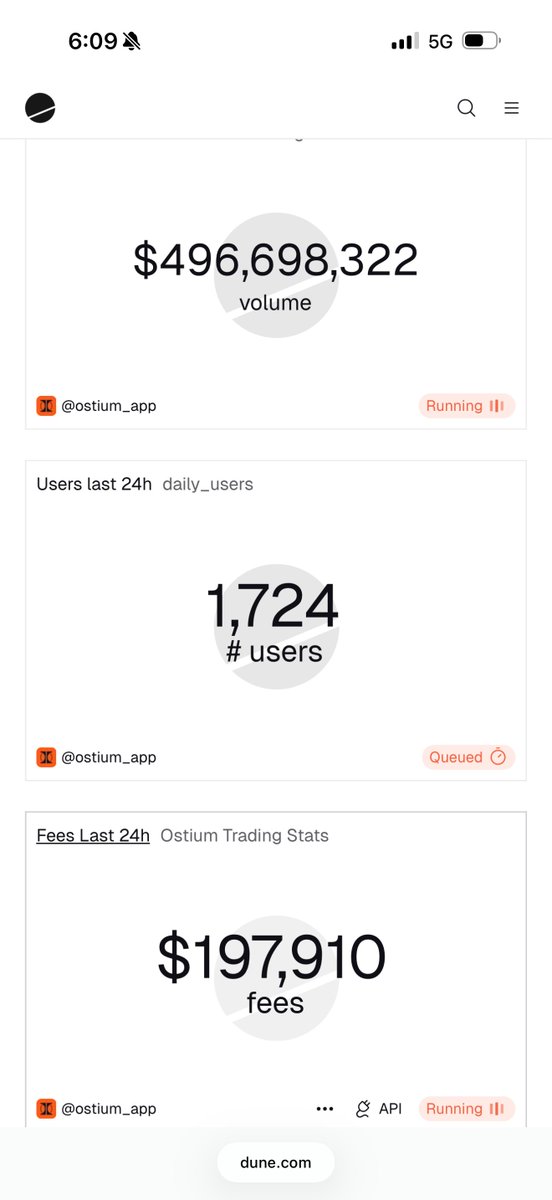

it's great day to be ostium

> launch URA

> first place to trade uranium onchain

> new ATH in daily users

> $500m in daily volume

> $200k L24H revenue ($71m annualized)

> all top 10 assets are RWAs

> silver and gold alone do $280m in L24H volume

trade the RWA renaissance onchain.

@TheTileApp - my battery died within a few months and you make it impossible to contact you for a replacement. No links found on all the pages. Please contact me

@elonmusk why not sell sky link to all the airlines so anyone on traveling that needs to access wifi doesn't have to tear their hair out bc it literally never works.

Battle of the perp DEXes --> @HyperliquidX vs @ostium: Comprehensive Comparison

As more traders migrate from CEXes to onchain (due to availability of tokens, security), perp DEXes are competing to offer speed/usability, liquidity, and innovative mechanics. 2 standout contenders — Hyperliquid and Ostium — are taking different approaches.

Below is a comprehensive breakdown of their strengths, risks, and how they’re positioning for the future.

- - - - -

1. Unique Selling Points

a) Hyperliquid

• On-chain order book: High-performance + fully transparent

• Purpose-Built L1: Custom L1 designed specifically for trading (CEX-like speed)

• HyperEVM Integration: Allows devs to build dApps that directly interact with the order book (for liq)

• Community-First: Self-funded w/o VCs --> substantial token distributed to early users

• Spot Ecosystem: Native token standard + auction system for launching new tokens (@Hypurrfun)

b) Ostium

• RWA focus: Specifically designed for trading tradfi (forex, commodities, and indices)

• Dual Liquidity Architecture: Liquidity Buffer + Market Making Vault structure mitigates adversarial r/s between traders and LPs

• High Leverage Capacity: Offers up to 200x leverage

• Market Hours Integration: Built to handle trading schedules, market closures, and holidays of traditional markets

• Risk-Adjusted Fee Structure: Dynamic fee system --> depends on position size, OI imbalance, and volatility

- - - - -

2. Risks and Drawbacks

a) Hyperliquid

• Centralised Validators: Currently operated by 4 nodes (controlled by the team)

• Single Point of Failure: Due to their custom L1 may have undiscovered vulnerabilities

• Oracle Dependency: Relies on price feeds that could be manipulated, particularly for less liquid assets

• Competition from Established CEXs: Competing directly with big CEXes (more well capitalised)

• Regulatory Uncertainty: non-KYC + operating w/o a formal licence

• EVM eco quality: Success depends on attracting high-quality projects to build on HyperEVM

b) Ostium

• Layer 2 Dependency: Relies heavily on Arbitrum (security and performance)

• Oracle Complexity: RWA markets require complex oracle solutions with many points of failure

• Limited Production Testing: Limited data on performance under high-stress conditions

• Late Market Entry: Entering a red ocean perp DEX space

• Difficulty Expanding the TAM: The platform may not offer significant ui/ux advantages to attract trad traders

• Market Hours Complexity: Managing trading schedules and closures for dozens of different traditional markets

• Regulatory Exposure: RWA focus may attract more regulatory attention

• LP Risk Management: Ensuring MMV liquidity providers understand + compensated for directional exposure risk

- - - - -

3. Conclusion

Both platforms represent innovative approaches to onchain perps, but with different focuses.

Hyperliquid has established itself as a leading perp DEX with a custom L1 and onchain order book, gaining significant traction in the crypto-native community. Since it is self-funded, its community-first approach strategy has has resonated very well with its (cult-like) users, though centralisation of its validator set remains a key concern.

Ostium is an up and coming platform which positions itself as a specialised platform for bringing RWAs onchain through perps, with a unique dual liquidity structure designed to align incentives between traders and LPs.

Both however will face regulatory and technical challenges which is typical in DeFi, and will be interesting to monitor how they overcome such hurdles.

More Leverage + No Liquidations

The Magic of Perpetual Options 🔥

The big take away from my post last year on why options have not boomed like perps was that we need to simplify options to fit within the perpetual futures framework. The beauty of the perp framework is traders only need to care about:

Entry price

Exit price

Funding paid/received

So we built Perpetual Options, which do exactly that.

The beauty of Perp Options is that perp traders don’t need to change how they think or trade. If you trade perp futures, you’re basically just trading leveraged spot.

And the cost of that leverage is the funding rate (basis).

The problem with leverage is that if the price moves against you, you get liquidated unless you post margin.

Now what if I told you that, for a few extra basis points in funding, you can eliminate that downside?

That’s what Perpetual Options do.

With perp options, the funding rate now includes two components

+ the cost of leverage (basis)

+ the cost of insurance or price protection (convexity)

In return, you get

+ MOAR leverage (OTM options give you >100x )

+ NO liquidations (by price)

The tradeoff is higher funding

It sounds almost too good to be true, but it’s real, and we think we’ve nailed the design.

Look at the image below—it looks like a perp.

And that’s the point. All you care about is:

+ Entry price

+ Exit price

+ Funding

Retardio proof

P.S. In the screenshot, we include the perp futures funding next to the perp options funding, so you can see exactly how much extra you're paying for the “insurance.” That difference between the two is the cost of convexity........expressed as a funding rate

Crypto cycles are around 4 years not because of the bitcoin halving but because of the length of the vesting schedules of useless L1s. I call it L1 ponzi rotation