There is no AI bubble.

In fact, some of the highest-quality companies on Earth are trading at surprisingly compressed valuations.

Forward P/E estimates (2028):

• $NVDA → 16.1x

• $MSFT → 16.8x

• $META → 13.8x

• $AVGO → 16.2x

• $AMZN → 17.9x

• $GOOGL → 20.6x

Think about that for a second.

The market is pricing:

❌ AI execution risk

❌ Slowing growth

❌ Margin pressure

❌ Excessive CapEx

But largely ignoring:

✅ AI monetization

✅ Proprietary silicon

✅ Cloud acceleration

✅ Robotics & automation

✅ Operating leverage

A few observations:

• $MSFT might be the cheapest AI stock in large-cap tech.

• $META is trading at a discount because investors don’t trust the AI spending story.

• $NVDA’s valuation implies a much sharper slowdown than current demand suggests.

• $AVGO remains one of the most underappreciated AI infrastructure winners.

Meanwhile, all four remain in strong technical uptrends.

If earnings continue to grow the way management teams expect, today’s valuations may look absurdly cheap in hindsight.

My highest-conviction names for Q3–Q4:

1. $NVDA

2. $MSFT

3. $META

4. $AVGO

The biggest opportunities often appear when sentiment and fundamentals diverge.

What am I missing?

Amazon is investing a massive $10B in Missouri to expand AI and cloud infrastructure 🚀🤖⚡. Another clear sign that hyperscalers are racing to build the backbone of the AI era. $AMZN #Amazon#AI#CloudComputing#TechStocks

Google is investing $1.5B to expand its AI data center campus in Alabama through 2027 🤖⚡🚀. $GOOGL is doubling down on AI infrastructure, power capacity, and long-term growth. #GOOGL#AI#DataCenters#TechStocks

NVIDIA is set to raise $20B in its first bond offering in 5 years 💰🚀🤖, fueling the next wave of AI infrastructure and next-gen chip innovation. Wall Street is betting big on the AI leader. $NVDA #NVIDIA#AI#Semiconductors#TechStocks

NVIDIA ($NVDA): files for a proposed notes offering, with sizing yet to be disclosed 📈💰🚀. Investors will be watching closely for capital allocation and future growth plans. #NVIDIA#AI#Semiconductors#TechStocks

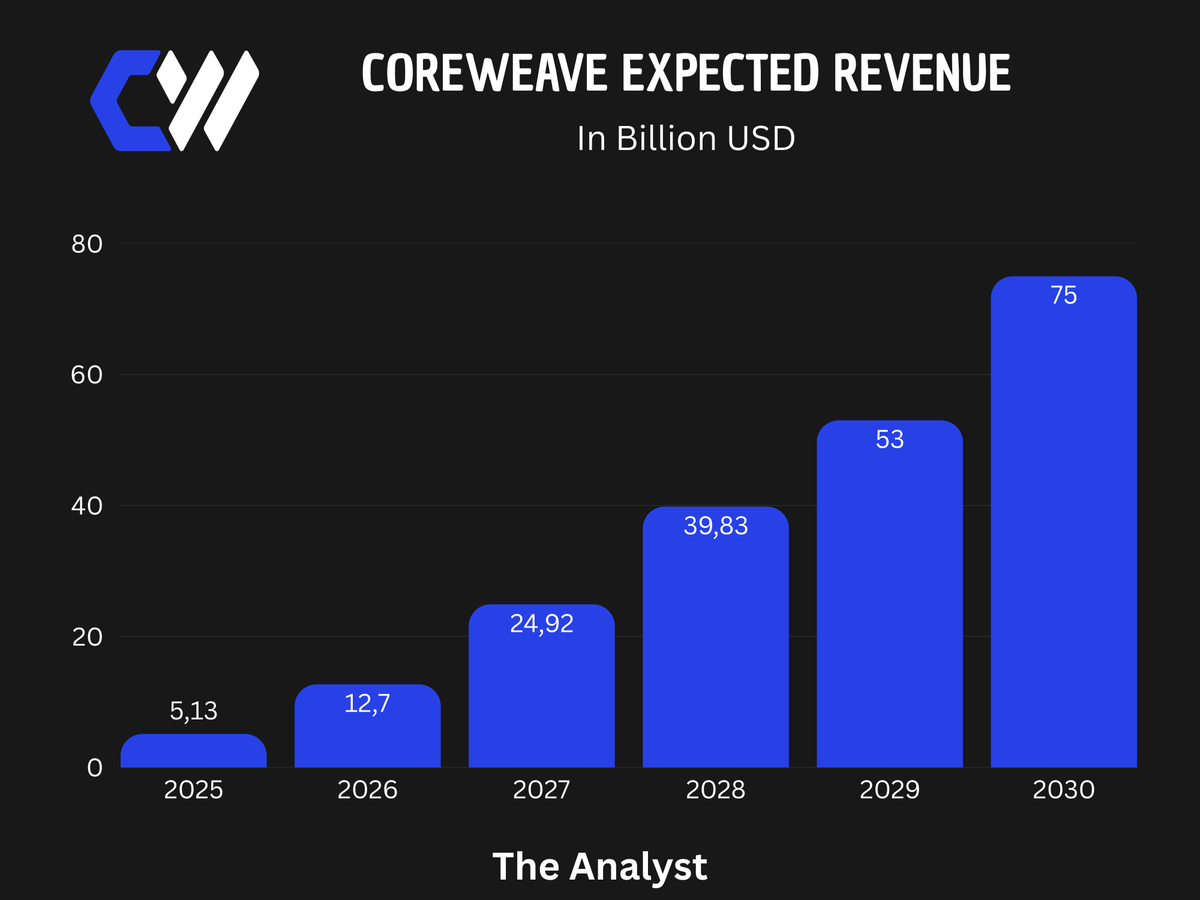

$CRWV is the most attractive buy amongst AI-Infrastructure companies.

And the math makes this reaally obvious:

Currently valued at $55B

Company expects to do $53B in revenue 2029 alone.

The demand remains huge.

Interest expenses will decline strongly over the next years.

The $NVDA partnership is making this a whole lot more attractive.

The reason this is so cheap now is most likely that $NBIS for a long time just seemed like the more attractive bet.

But $NBIS being valued more than $CRWV is just ridiculous.

To justify this valuation gap, $NBIS margins would need to remain more than twice of $CRWV's over the long-term.

Most likely not going to happen.