Had a Jane Street interview in 2013 that still bothers me.

It was my 6th round. Final interview. The guy walks in carrying no laptop, no notebook, just a cold brew and what I later realized was a single IKEA tea candle.

He writes on the whiteboard:

food: $200

rent: $800

utilities: $150

candles: $3,600

family: dying

Then he turns around and says, “Optimize.”

I laughed because I thought it was a culture-fit bit. He did not laugh.

So I said, “Well, obviously you spend less on candles.”

He says, “Assume candles are non-discretionary.”

Okay.

I start building a model. Basic constraint satisfaction. Family survival as a soft penalty. Candles as a state variable. Maybe there’s an arbitrage where you buy wholesale paraffin and convert the $3,600 line item into inventory.

He stops me.

“You’re thinking like a consultant.”

That’s when I knew I was in trouble.

He says, “Give me a bid-ask on family dying.”

I say, “What?”

He says, “You’re long candles, short family. Where do you make markets?”

I try to recover. I say the real issue is liquidity: rent and utilities are fixed, food is elastic, candles are emotionally inelastic. Therefore the optimal strategy is to securitize future candle enjoyment and borrow against it.

He nods for the first time.

Then he asks, “What time do you sell the candles?”

I say, “Whenever the market is liquid?”

He says, “Be more specific.”

I say, “Uh… 10 a.m. Eastern?”

For the first time, he smiles.

He goes, “Every day?”

I say, “Every day.”

He says, “In size?”

I say, “In size.”

He says, “And what do we call that?”

I say, “Market manipulation?”

The room gets very quiet.

He looks disappointed and writes something down.

“No. We call it providing liquidity to candle ETFs during the U.S. cash open.”

I try to save it. “Right. Of course. The family isn’t dying because we underfunded them. They’re just experiencing temporary price discovery.”

He nods again.

Then he points back at the board.

I had missed it. The utility bill was $150, but candles provide light. You can zero out utilities.

I update the budget:

food: $200

rent: $800

utilities: $0

candles: $3,750

family: still dying, but now in a more capital-efficient way

He says, “How confident are you?”

I say, “0.95.”

He smiles and circles candles.

“0.95 huh?”

Then he asks me to estimate how many leveraged longs get liquidated if we dump $3,750 of candles at 10:00:01 every morning for 90 consecutive trading days.

Needless to say I did not get the offer.

Introducing the Synthesis CLI, SDK and API

Built for agents, builders, vibetraders and institutions

Get markets, execute faster trades and consume more data from a single suite of tools for prediction markets

Introducing Claude Code Security, now in limited research preview.

It scans codebases for vulnerabilities and suggests targeted software patches for human review, allowing teams to find and fix issues that traditional tools often miss.

Learn more: https://t.co/n4SZ9EIklG

On December 24, I posted my last tweet on Polymarket. A few people probably assumed I went quiet because of the holidays. Christmas. New Year. Time off. That wasn’t the case. While most people were celebrating, I was locked in my room. Eighteen hours a day. No trading. No scrolling. Just logs, papers, and markets. My mom was the only one who knew I hadn’t gone anywhere.

For six months before that, I had been “studying” prediction markets. Mostly Polymarket, but also Opinion and Kalshi. I read the same news as everyone else. Watched the same debates. Tried to predict outcomes better than the crowd. Yet the same pattern kept repeating: a small group of accounts printed quietly while most traders slowly became liquidity. That gap bothered me. So instead of asking what will happen, I asked a different question. Why do the same wallets keep winning, regardless of the event?

The answer wasn’t prediction skill. It was purely execution.

Polymarket isn’t about forecasting better than others. It’s a technical system with real constraints. Order placement, timing, queue position, and how liquidity shifts minute to minute matter more than opinions. I kept seeing the same belief produce different results depending on execution details. That’s when I stopped trading and focused purely on understanding how the system behaves under load. One quick shoutout to @thejayden for creating Polymarket Lounge community it helped me a lot on the technical side whenever Polymarket’s docs weren’t enough or something in the system didn’t behave as expected

For weeks, I tracked 12–15 wallets simultaneously across different niches. 15 mins BTC markets. Sports markets. Weather predictions. Even odd markets like Elon Musk tweet counts. Multiple screens open. Pen and paper on my desk. Every entry, every partial fill, every exit. How size changed. How positions were reduced. When they hesitated. When they didn’t. I wasn’t searching for a strategy. I was trying to understand behavior that stayed consistent across markets. This isn’t something you get by reading threads, prompting Claude Code, or deploying some script you found online. And definitely not by stealing someone’s GitHub repo. That only copies the surface. The real edge lives underneath.

Once patterns became clear, I started coding. The first script failed. The second failed differently. I rewrote it again and again. By January 26 (today), I was on version 41. Each iteration removed assumptions rather than adding features. Some changes improved results. Others broke things. That feedback loop was the work. Over time, execution stabilized and outcomes became less emotional and more repeatable.

At some point, the P&L curve changed.

Quietly. The attached graph isn’t about the number. It’s about consistency. Fewer surprises. Fewer forced decisions. A process starting to behave like a system instead of a gamble.

From here on, I will be fully focused on prediction markets. Polymarket especially. Breaking down how these markets actually work, where mispricings come from, how gaps form, where arbitrage appears, and why execution decides who wins. No signals. No shortcuts. Just deep work, documented in public. If that’s what you’re here for, this is only the beginning

No complexity. No accident.

10/10 was caused by irresponsible marketing campaigns by certain companies.

On October 10, tens of billions of dollars were liquidated. As CEO of OKX, we observed clearly that the crypto market’s microstructure fundamentally changed after that day.

Many industry participants believe the damage was more severe than the FTX collapse. Since then, there has been extensive discussion about why it happened and how to prevent a recurrence. The root causes are not difficult to identify.

⸻

What actually happened

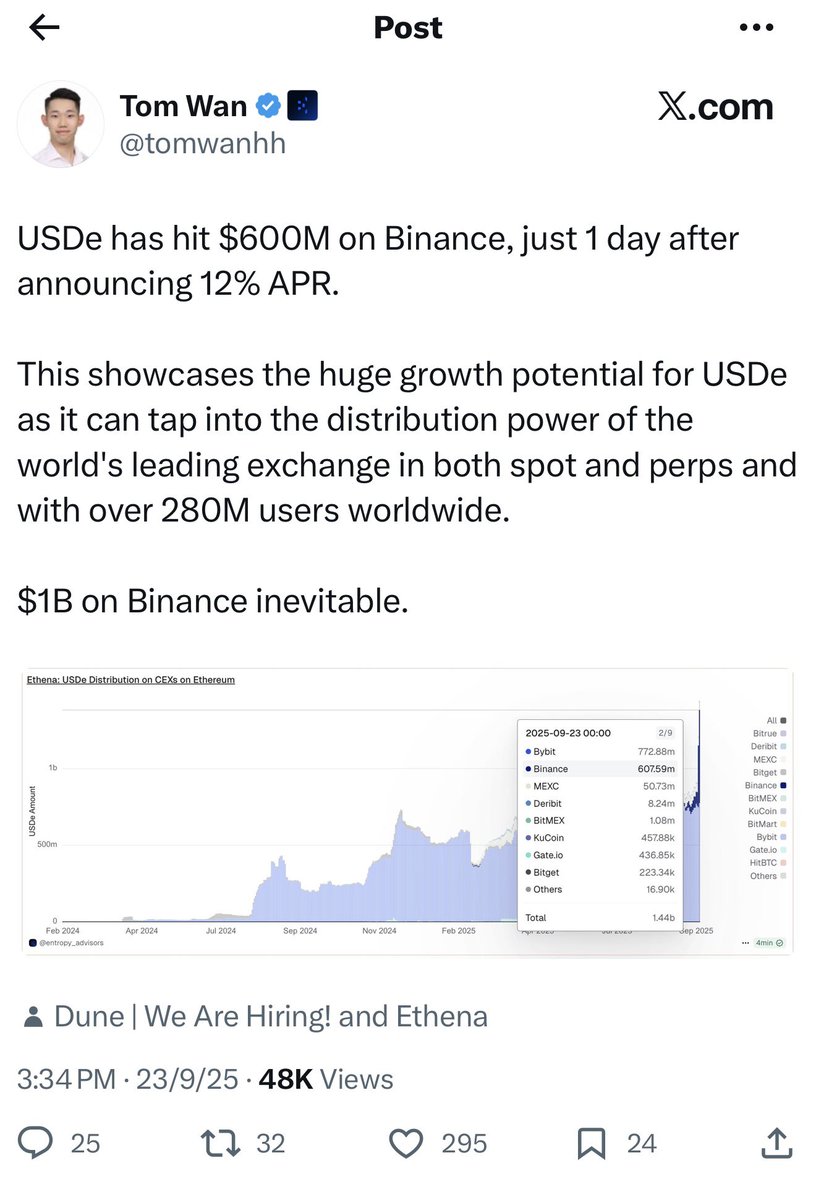

1.Binance launched a temporary user-acquisition campaign offering 12% APY on USDe, while allowing USDe to be used as collateral with the same treatment as USDT and USDC, and without effective limits.

2.USDe is a tokenized hedge fund product.

Ethena raises capital via a so-called “stablecoin,” deploys it into index arbitrage and algorithmic trading strategies, and tokenizes the resulting fund. The token can then be deposited on exchanges to earn yield.

3.USDe is fundamentally different from products such as

BlackRock BUIDL and Franklin Templeton BENJI, which are tokenized money market funds with low-risk profiles.

USDe, by contrast, embeds hedge-fund-level risk. This difference is structural, not cosmetic.

4.Binance users were encouraged to convert USDT and USDC into USDe to earn attractive yields, without sufficient emphasis on the underlying risks. From a user’s perspective, trading with USDe appeared no different from trading with traditional stablecoins—while the actual risk profile was materially higher.

5.Risk escalated further as users:

•converted USDT/USDC into USDe,

•used USDe as collateral to borrow USDT,

•converted the borrowed USDT back into USDe,

•and repeated the cycle.

This leverage loop produced artificial APYs of 24%, 36%, and even 70%+, widely perceived as “low risk” simply because they were offered by a major platform. Systemic risk accumulated rapidly across the global crypto market.

https://t.co/IK2gW4xUOP that point, even a small market shock was sufficient to trigger a collapse.

When volatility hit, USDe depegged quickly. Cascading liquidations followed, and weaknesses in risk management around assets such as WETH and BNSOL further amplified the crash. Some tokens briefly traded near zero.

The damage to global users and companies—including OKX customers—was severe, and recovery will take time.

⸻

Why this matters

I am discussing the root cause, not assigning blame or launching an attack on Binance. Speaking openly about systemic risks is sometimes uncomfortable, but it is necessary if the industry is to mature responsibly.

I expect there may be significant misinformation and coordinated FUD directed at OKX in the near future. Even so, speaking honestly about systemic risk is the right thing to do—and we will continue to do so.

As the largest global platform, Binance has outsized influence—and corresponding responsibility—as an industry leader. Long-term trust in crypto cannot be built on short-term yield games, excessive leverage, or marketing practices that obscure risk.

The industry needs leaders who prioritize market stability, transparency, and responsible innovation—not a winner-take-all mentality where criticism is treated as hostility.

Crypto is still early.

What we choose to normalize today will determine whether this industry earns lasting trust—or repeats the same mistakes again.