Loved this chat with Ruffer FM @DuncanMacInnes8

Macro aware value investing and the outlook for financial markets. A tour de force.

Please enjoy ...

https://t.co/FJSEq7z23D

Gross incompetence? Fraudulent promotion? I hope as a CFA you know, Tasha, that an investment recommendation must be made with a reasonable basis. Otherwise you lose your charter for violating the Standards of Practice and Code of Ethics. A $7-$10.9 trillion market cap expected range by 2029 makes ARK perhaps the biggest charlatan of the modern era of fleecing the retail investor. Apple, Microsoft and Nvidia are today valued at “only” $9.6 trillion. The whole S&P is valued at $44 trillion and 24 times forward earnings. Your 2029 4.1% free cash yield suggests a 24 multiple to earnings for the car company, suggesting $450 billion in 2029 profits (today’s REVENUES are $95 billion). Holy delusion, Batman. You couldn’t help yourself by topping last year’s ridiculous predictions by 25% despite flat revenues and fast-declining margins and profits.

This one is is a doozy: “Our research suggests that generalizable humanoid robots represent a ~$24 trillion global revenue opportunity at scale.” You do realize the entirety of global GDP is just over $100 trillion?

That Tesla Insurance continues to make an appearance in your factually devoid analysis brings humor to the entire episode of the promotion of your book and the car company. Suggesting the insurance business will be nearly as large as Progressive is today? Have you seen the 40% operating losses on the so minuscule book of auto insurance that it doesn’t merit mention in the company’s financial statements? Three years ago you predicted a 40% operating profit in insurance. I guess you meant losses, which actually makes sense.

Not sure why @SECEnfDirector hasn’t descended on ARK’s offices in St. Pete or why @CFAinstitute is apparently disinterested in investigating a lack of reasonable basis in your “research” but one thing remains - ARK sure does know how to put a spin on the promote while eviscerating retail investment capital. At least you guys have gotten rich with more than $400 million in management fees while losing literally tens of billions. Grifters gonna grift.

Enjoyed this recent piece from Ruffer on gold/silver equities.

As interest rates rose ppl took money out of gold equities/ETFs, but since the Ukraine invasion foreign central banks/emerging market savers have been buyers of the actual metal.

If interest rates come down/inflation goes back up money likely flows back into gold stocks.

Despite all the heat the UK gets as a basket case and for the death of the LSE (no tech, funds underweight, outflows) there's a buyer stepping up

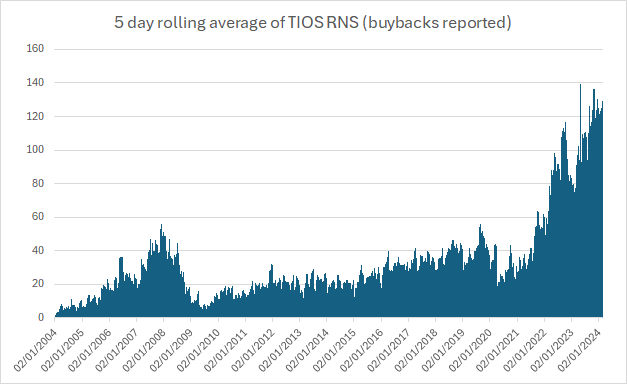

I scraped the data for UK company "transaction in own shares" RNS announcements, issued every time a company buys back its own shares

Essential for anyone investing in Investment Trusts.

Great insights from @DuncanMacInnes8 from Ruffer and Chris Hart from @RockwoodStrat

Ruffer is my Ying (with PNL and CGT) to my wider Yang portfolio.

@MoneyMakersITs https://t.co/jVWPiJU7NN

@AtlasPulse@jamesonthechain Don’t put me in the haters camp please.

My position is better characterised as ambivalence rather than bearish. At close to $1 trillion market cap, I just don’t think it has the same asymmetry and the whole debate has too much heat and not enough light. Merry Christmas!

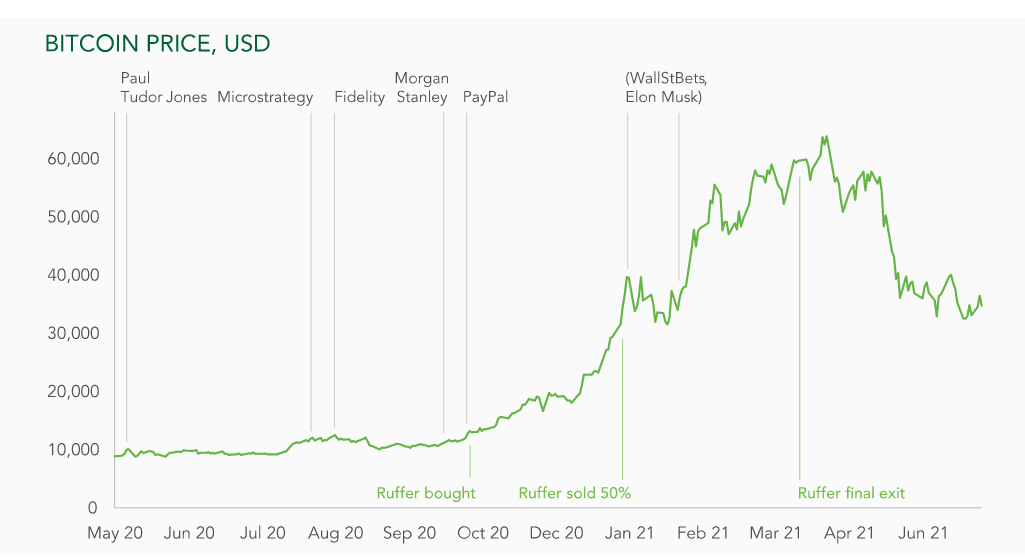

I still think what #Ruffer pulled off was one of the best #bitcoin trades ever from an unlikely player. Even after this year's gains, it has not reached the levels Ruffer got out at in 2021 with a cool $1 billion. @DuncanMacInnes8 https://t.co/cfFD4Y2YmJ

Money’s too tight to mention 🎶

Investment Director at Ruffer, @DuncanMacinnes8, explores how, in 2023, liquidity is being drained from the financial system, yet nobody seems to have told markets.

#AJBellInvestival

🎥In this interview, @DuncanMacInnes8, fund manager at Ruffer, covers key insights like why the Japanese Yen looks interesting, the oil sector, and Megacap tech including TSMC Alibaba, Meta & Amazon.

🔗Watch here: https://t.co/IolI3ksLkE

#AIM

Want to stop a bank run? In the old days you could just get tellers to count the money twice before handing it over (sharp thinking from JP Morgan...). You can't do that now (no tellers). Times have changed (maybe too much) says @DuncanMacInnes8 New pod https://t.co/wXsbQppeXd

@davidcundell@MerrynSW Fair point. Short term rates are still negative after inflation (call it 5% rates and 6% inflation).

However longer term real rates are positive in the UK & US. US TIPS will pay you inflation plus 1.5%. That’s a decent safe haven!

New podcast. Times have changed.. you don't have to take much risk to get a good yield anymore. 7%? Easy. I talk to @DuncanMacInnes8#MerrynTalksMoney https://t.co/VGPpsXXexw

Policymakers have a choice between competing goals.

Ease the pain in markets and manage contagion versus containing inflation.

The first requires easing, the second requires tightening.

Sooner or later all these support packages look like QE!

Nice article from Ruffer LLP on the Silicon Valley Bank situation, and what is the more interesting element for investors to pay attention to (versus the less useful hype around moral hazard and whether not its right to "bail out" the tech sector)

https://t.co/x2joFrdUY8