I have made over a MILLION in the last 2 MONTHS

My SECRET is having a watchlist for each sector to catch rotations EARLY

HERE IS THE SECTOR ROTATION WATCHLIST:

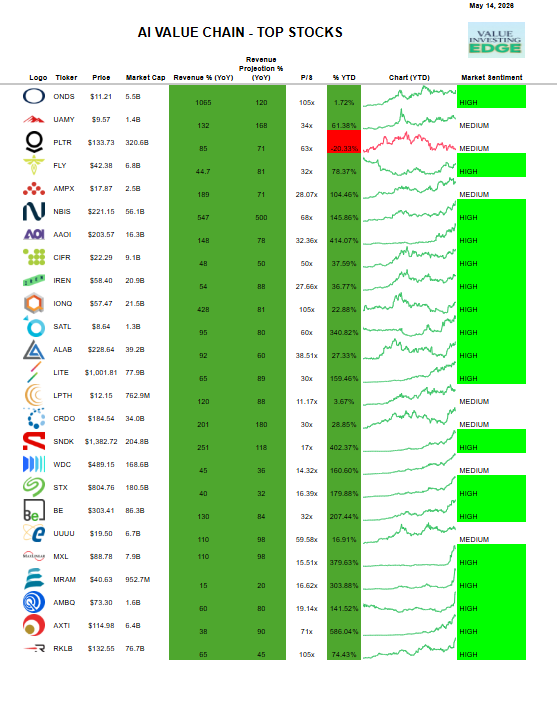

Memory: $MU $SNDK $WDC $STX

Semis: $NVDA $AMD $ARM $INTC

Networking: $AVGO $MRVL $CRDO

Photonics: $AAOI $LITE $COHR $NVTS $GLW

Infrastructure: $DELL $SMCI

Data Centers: $IREN $CIFR $APLD $NBIS

Software: $MSFT $NOW $SNOW

Defense: $PLTR $KTOS $AVAV

Drones: $ONDS $DPRO $UMAC

Robotics: $OUST $SYM $TSLA

Space: $ASTS $RKLB $RDW $LUNR

Quantum: $IONQ $QBTS $RGTI

Nuclear: $OKLO

Fintech: $HOOD $SOFI $AFRM

Copper: $FCX $SCCO $TECK

Autonomous: $JOBY $ACHR

Just as a recap, these were all my core European longs:

1. $SIVE

2. $LPK

3. $SOI

4. $RPI

5. $IQE

6. $ALRIB

7. $XFAB

Sivers: As you know by now, core laser chokepoint over next generation photonics, from 1.6T pluggables to CPO.

Embedded in many hyperscaler suppliers from Jabil to Ayar. Should go brrr 2027 but markets are forward looking, so ramps + qualifications should get priced in now.

LPK Laser - Glass core substrate "monopoly" with LIDE.

"More than 80% of major global players have selected our equipment for process validation, learning and scaling to mass production"

Soitec - Silicon photonics SoI substrate pure monopoly while coming out of legacy drag segments.

Raspberry Pi - Was my fun idea around Raspberry Pis being used for AI hardware deployments.

Previously this thing was mainly educational or hobby boards, but now used for edge/local AI. Just thought revenue increase would be extremely material and it played out well.

IQE - Critical epiwafer player for your Western photonics like Macom, Tower, Lumentum, and others.

Was kinda going under, but thought their latent capacity relative to Landmark was undervalued.

Also given how important it was, I thought that your downstream players + Govs wouldn't let it go under, so it was more of a moonshot idea earlier in the year.

Lot more derisked now, very important.

Riber - Kinda monopoly in the MBE space, exposure to Quantum / quantum dot + silicon photonics.

Found out from OSINT help from a friend latentvalue that Microsoft Quantum was buying their machines, so this was direct hyperscaler validation + kinda de-risked at current MCs.

XFab - SiC foundry backed by EU/US CHIPS Act with power semi upside. (152% Y/Y growth for their sic vertical).

Main growth was their silicon photonics foundry past 2027 that's getting evaled by nvidia. And that they're leading Europe's value chain efforts in photonics, kinda like an early tower semi.

We'll see how this plays out, thought power semi exposure + low P/B would derisk the company until they scale their photbunchonics efforts.

From my own personal thoughts:

Out of the maybe $SOI has already been re-rated the most? But I'm holding anyway.

$LPK and $ALRIB I think are still undervalued despite their monopolies.

$RPI is just kinda seeing how things go at this point, would be hilarious if they ended up like a mini nvidia for low end edge ai.

$IQE probably has a long way to go given new tower long term agreement, alongside macom. And if they convert latent capacity, I still think it has a chance of rerating like landmark.

$XFAB idk if im missing something or are markets missing something. you have nvidia as a direct eval of their silicon photonics foundry, and it's trading below replacement P/B. i think im right though.

$SIVE I see has the highest upside out of all of them given laser company ability to vertically integrate, acquire companies downstream to make their lasers more valuable, etc. Just like coherent/lumentum.

There's like 1-2 more random ones that aren't really material, but just in general.

These are the ones I've liked the most.

$MU. Blue Candle on a -4.7% red day. Next day: +12%.

Beta model. That is the kind of signal we are building toward. Stable data. Promising results. Best system in the world. We meant it.

300+ charts daily. Try it free:

https://t.co/ZQDP5HCFyq

The U.S. government & President Trump have literally been telling you where the next big opportunity is:

SPACE.

These are the 5 layers of SPACE you need exposure to:

1. Launch Infrastructure: $SPCX, $RKLB, $LUNR

2. Spacecraft Hardware: $RKLB, $RDW, $LHX

3. Orbital Infrastructure: $SPCX (Starlink), $ASTS, $IRDM

4. Space Data Processing & AI: $PL, $SPIR, $PLTR

5. Downstream Applications: $LMT, $KTOS, $ONDS

The space race is not a 2026 story. It is a decade-long transformation just getting started.

Which names am I missing?

Which name are you placing your biggest bet on?

There was interesting research published called "Democratization of Retail Trading".

That did a study on 1.6 Million $RDDT WSB comments.

and found:

1. "WSB outperformed almost all investment banks at detecting top-performing stocks."

2. "Their average returns compete with the best investment banks and outperform them in certain cases."

Their conclusion?

"We conclude that WSB may indeed constitute a freely accessible, valuable source of investment advice."

I do find WSB is really early to names like $RKLB, $HOOD, and others, but often get timing extremely wrong (with options).

I think X is where all the alpha is at nowadays.

GUESS WHAT ANON?

After today’s new news with Ayar joining Nvidia NVLink fusion.

$SIVE is now the laser source for likely:

The entire Nvidia’s NVLink CPO listed supply chain ecosystem partners.

From Marvell Celestial, Lightmatter, and now Ayar today (the three listed in NVLink CPO).

This is why I call $SIVE a structural photonics laser chokepoint over CPO and now Nvidia ecosystem supply chains.

-> Celestial was likely a direct customer to Sivers, not through Poet. (2023 investor presentation mapping), then bought by Marvell.

-> Lightmatter was also listed there as a customer in 2023 investor presentation deck mapping.

And… Guess what else?

Then they all happen to use GlobalFoundries.

Which Sivers is now the GFS silicon photonics foundry-level reference laser (also new news yesterday).

Supply chain mapping all starting to make sense now anon?

Sivers is also likely now the primary laser source for Ayar after they removed Macom/Lumentum their laser supply chain section (now just gfs/sivers), as a cherry on top.

Algorithms completely miss this type of image based mapping.

After this announcement, I personally think current valuations are very undervalued:

Given Sivers now holds one of the most important structural laser chokepoint over Nvidia CPO NVLink ecosystem supply chains.

Fun to see my highest conviction Neocloud pick in $NBIS age well.

I wrote a thesis last year on the Neocloud sector becoming a major theme.

And then picked the King.

-> Nebius is #1 out of the entire sector from $IREN to $CRWV.

$84 -> $260.

Thesis validated by markets.

It's funny to see people saying that with photonics and CPO companies like $SIVE $AAOI $COHR etc, you're already late because they've gone up 1000%

It actually makes me laugh hahaha

Let's put it into context:

A company like $NVDA, for example, at one point went from $0.5 to $5 and shot up 1000%

Someone would say it's over, I'm way too late, whoever invests there is a fool

$NVDA still had about 40000% left to go to this day

No, a company's return percentage defines nothing

Instead, it's the MC and the fundamentals/thesis

More comparisons, semiconductor companies like $TSMC $NVDA $AMD $INTC have an MC of ~$300B-$800B on average

With some surpassing $1T, $2T, or even $3T

Memory companies like $MU $SNDK Samsung SK Hynix have an MC of ~$200B-$400B on average

In contrast, photonics/CPO companies like $AAOI $LITE $SIVE $COHR $AXTI have an MC of ~$2B-$25B on average

This makes you realize that even if they go up 1000%, they are still tiny in comparison

And they have a huge way to go and are only at the very beginning

Especially companies like $SIVE with an MC of ~$1B-$1.5B that are so well positioned at the start of the CPO ramp

And have dozens of tier 1 and tier 2 customers

Top 6 growth stock groups for next-generation AI infrastructure buildout in 2026.

Optical sector:

1. $AAOI

2. $AXTI

3. $LWLG

4. $LITE

5. $COHR

Critical Minerals:

1. $USAR

2. $UUUU

3. $MP

4. $UAMY

Memory/Storage:

1. $SIMO

2. $SNDK

3. $MU

4. $WDC

5. $MRAM

Energy:

1. $AMPX

2. $TE

3. $EOSE

4. $BE

Semiconductor:

1. $NVTS

2. $MRVL

3. $AMD

4. $ARM

5. $AMBQ

AI Infrastructures:

1. $NBIS

2. $IREN

3. $CIFR

4. $ALAB

We are still early in the AI buildout phase and these stocks has long runway for growth.

Bookmark and invest in the best ones!

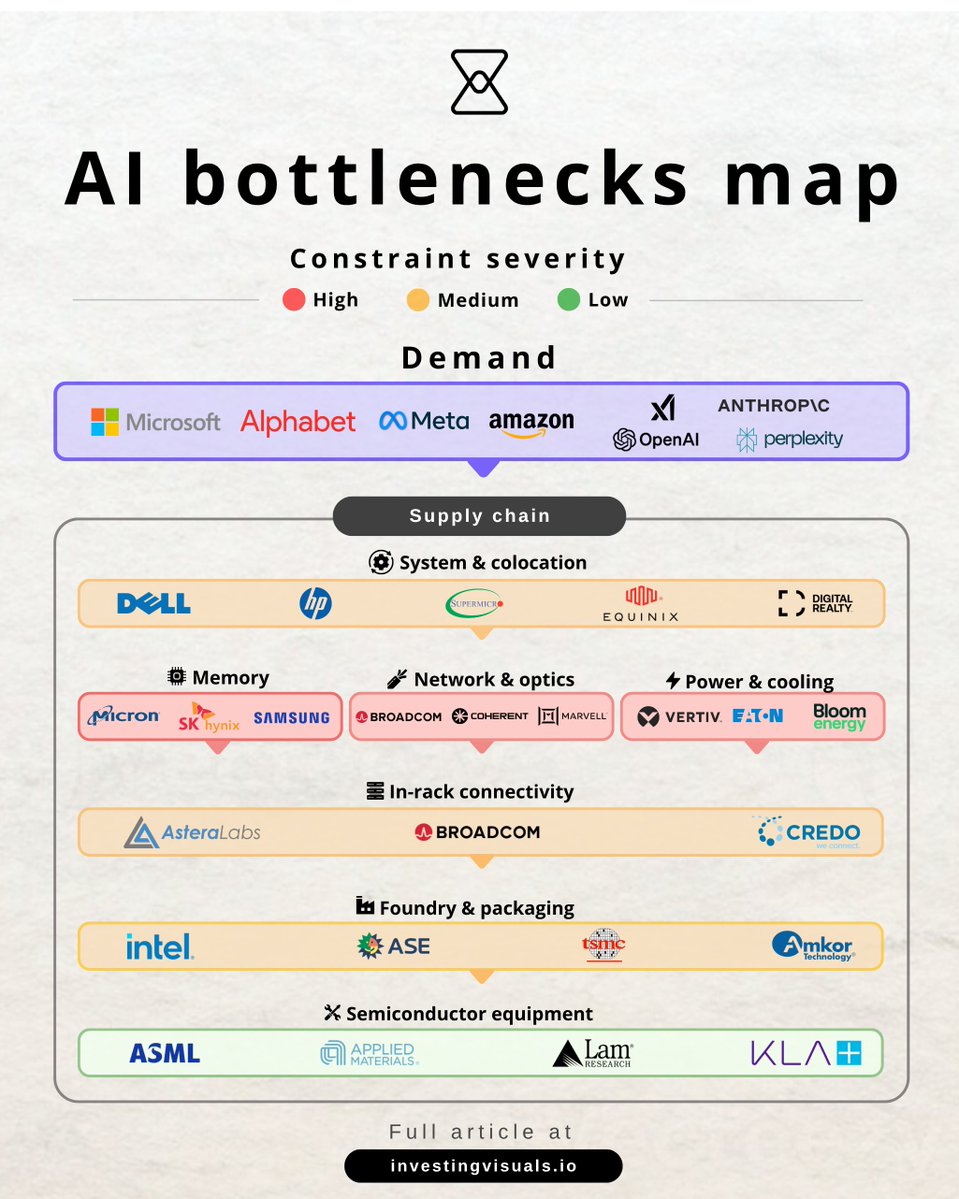

Photonics value chain in 5 layers. The companies building AI’s optical backbone.

$AXTI – Compound semiconductor substrates. Small, cyclical AI photonics supplier.

$AAOI – Optical transceivers for AI data centers. High risk, high upside.

$LITE – Diversified photonics. Stable, slower growth than AAOI.

$ASML – Only maker of EUV lithography machines. Irreplaceable monopoly.

$ONTO – Semiconductor inspection/metrology tools. Smaller KLAC alternative.

I found the next hidden 10x AI stock like $SIVE at $1 and no one is talking about.

Just like I called $NBIS at $20, $ONDS at $1, $ASTS at $20, and many others.

It’s under $1B market cap.

I’ll share it here first so don’t miss out.

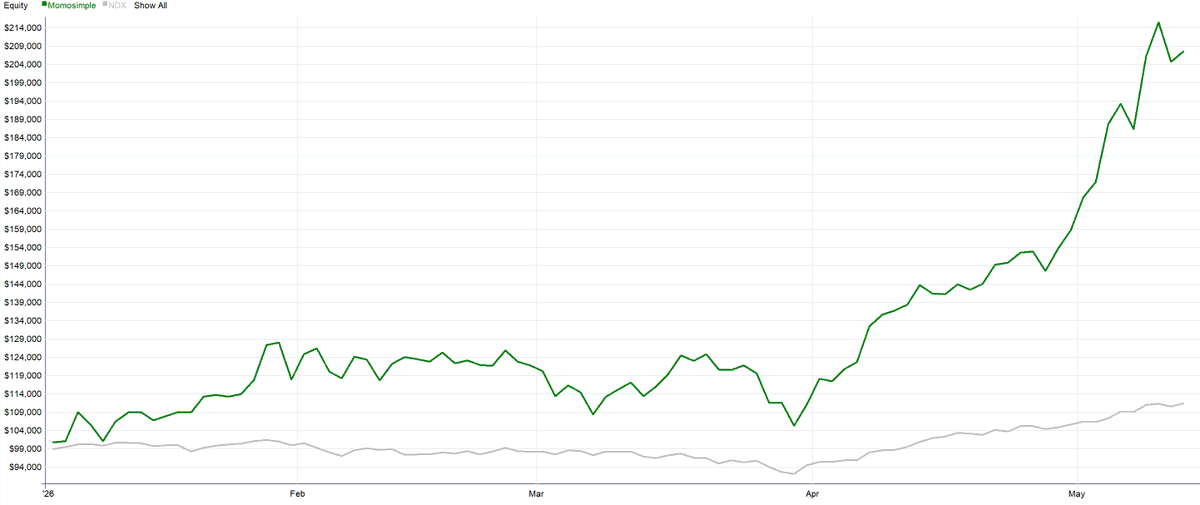

Top momentum Nasdaq stocks are killing NDX this year.

Why hold every stock in QQQ if the edge is in owning only the strongest names?

Same NDX universe. Same Nasdaq regime risk. Much cleaner exposure to winners.

Simple logic:

Universe = Nasdaq 100

Rebalance = month-end

for each stock:

mom = 120-day % change

eligible =

close > $1

and close > 200-day MA

and mom > 0

rank eligible by mom

buy top N

size = 100% / N

exit next month-end

repeat

No news.

No prediction.

No complex AI.

Just momentum, trend filter, monthly rotation, equal sizing.

To trade profitably? Just remove noise until only the rule remains.

$SIVE 2025 annual report analysis.

TLDR: Extremely Bullish.

Sivers main growth vector is CPO, but they've TAM expansioned to pluggable transcivers + multiple new qualifications/development.

1. "We are currently seeing great interest... testing our DFB lasers across multiple manufacturers in pluggable transceivers"

For pluggable angle, we've seen this with $JBL 1.6T LRO already, but annual report hinted they're developing/qualifying with more hyperscaler suppliers.

"Our serviceable markets have now been expanded to include pluggable optical interconnects as well as scale-up and scale-out architectures for co-packaged" (TAM expansion)

2. "Discussions with hyperscalers and pluggable transceiver suppliers indicate a shortage of CW lasers in the coming years"

$LITE already signaled CW laser bottlenecks, and they had to buy externally from competitors. So we kinda guessed CW Laser was a bottleneck.

And this confirmed it, so was wondering about Win semi.

"The partnership announced with high-volume supplier Win Semiconductor in March 2025 now gives us a strong position to meet growing demand"

$SIVE likely has capacity locked in with Win from this nuance, which is exactly what I wanted to know.

This positions Sivers in the CW laser as both a bottleneck and CPO laser architectural leader.

VOLUME PRODUCTION H2 INDICATIONS (BULLISH):

3. "The collaboration positions both companies to address the rapidly growing market for optical AI connectivity, with prototypes to be demonstrated to customers during the first half of 2026 and with the goal of scaling up production by the end of 2026"

H1 is more preproduction, H2 production signaled starting with names like $POET.

4. "We are pleased that our largest LIDAR customer will increase production starting in the fourth quarter of 2026"

$AEVA start of volume production Q4 with $SIVE = bullish for both.

Revenue floor from LIDAR as their CPO scales.

5. Sivers announced a partnership with LIGHTIUM AG to integrate their CW lasers directly onto TFLN wafers. 3.2T+ cycle. (future proofing)

FYI no decent investor cares about last year's 2025 financials from development contracts aside from Swedish Media/Locals.

Especially when you're forward looking for the 2027-2028 CPO supercycle.

But the hint from you can take away from financials + geography that is $NOK is now the high confidence customer of $SIVE.

TLDR:

-> Win Semi implied capacity lock in during CW laser bottleneck

-> Hints of new group of hyperscaler suppliers testing/qualification for pluggable transcivers, which is massive TAM expansion.

-> New customers for CW lasers

-> Volume production scaling starting H2 for both photonics and lidar.

What an insane day for photonics.

$SIVE up 31.3%

$TSEM up 23.1%

$AAOI 20.01%.

It feels like a lot… but this just means you’re early to the next supercycle and there’s a lot of room to go.

Lot of people on X ask what’s next after $SNDK?

Here they are.

$MU $DRAM CPU demand is going up and this is extremely bullish for Micron, Samsung & SK Hynix.

$INTC CEO confirmed CPU to GPU ratio shifting from 1:8 toward 1:1. That is 800% more and it has HUGE implications for memory demand.

These are NOT NVIDIA CPUs. These are standalone Xeon racks running agent orchestration, RAG pipelines, tool calling, and multi-agent coordination alongside GPU clusters.

Traditional servers ran 128 to 256GB of DRAM. AI-optimized servers now ship with 512GB to 1TB or more per node. Every one is a new high-margin server DRAM demand event. Higher margin than HBM. Every server also needs significantly more SSD as model sizes and context windows grow.

The demand multiplier is not 8x. It is closer to 16x or more when you stack both numbers together.

Meanwhile GPU nodes simultaneously need more HBM and SOCAMM as context windows expand.

Two demand vectors. One direction. Neither slowing down.

Valuation Multiples Expansion & Structural Shift Incoming.