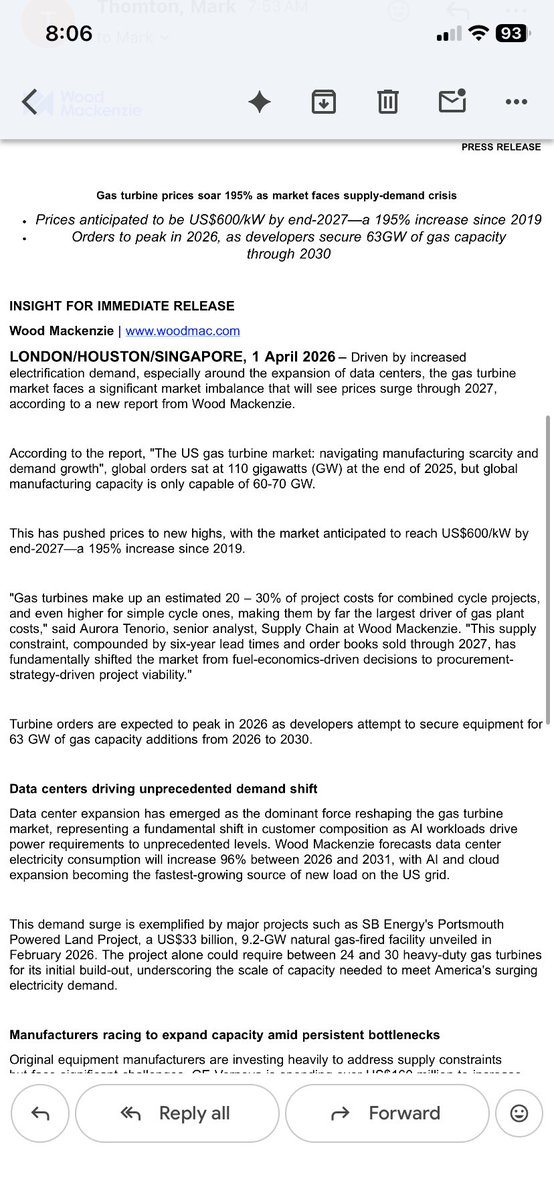

Bold calls from WoodMack on gas turbine supply bottlenecks. New WoodMac report lays it out:

-Global orders at 110 GW. Manufacturing capacity: 60-70 GW

-Prices heading to $600/kW by end-2027. Up 195% since 2019

-Lead times six years. Order books sold through 2027

-Data center power demand up 96% between 2026-2031

-GE Vernova, Siemens, Mitsubishi all expanding capacity but the real chokepoint is single-crystal blade production. Only a handful of suppliers globally can do it at scale

Per BNEF, Microsoft is in exclusive talks with Chevron and Engine No. 1 for a ~$7B natural gas power plant near Pecos, TX. Initial capacity of 2,500 MW, potentially expanding to 5,000 MW. Site sits in the Permian Basin close to cheap gas supply. Could be operational by 2027. Chevron and Engine No. 1 already secured seven GE Vernova large gas turbines.

There’s a growing amount of excitement and trepidation around off-grid data centers.

I’m not convinced many will actually go fully off-grid -- probably as a bridge in most cases. But it’s surfacing a more interesting tension about how we build the system.

As @ceboudreau detailed, that tension played out on stage at CERAWeek between Fermi and Google.

Fermi is leaning into the “power island” model that pairs data centers with dedicated generation, starting with gas and potentially nuclear. The idea is to move faster, avoid interconnection bottlenecks, and not push costs onto the broader system.

Google pushed back on that framing. Their view is that once you start building isolated systems, you end up overbuilding for reliability and tie up more capital into assets that run a fraction of the time. And none of that investment actually improves the grid. There’s also a concern that it could lead to higher system costs over time if those resources aren’t shared.

We will clearly see some version of both of these approaches, but I agree more with Google's @AmandaCorio on this one: “We are focusing too narrowly on this moment and the bottlenecks, and not thinking collectively as a system in 10 years."

More detail on the Meta-Entergy plans... Meta is funding 7 new gas plants through Entergy Louisiana to power Hyperion, its largest data center. Total buildout now 10 plants, 7+ GW of generation. 5 GW for compute, rest for campus. Meta also paying for 240 miles of new transmission lines, battery storage, nuclear uprates, and committing to fund up to 2.5 GW of renewables. Entergy says Meta pays full cost of service with $2B+ in ratepayer savings over 20 years. Seven new plants still need state regulatory approval.

Cowen note this AM:

-Hyperscale DC demand strong but bank financing is seeing a flight to quality. Only MSFT, AMZN, GOOGL, META, and NVDA can secure 200MW+ at scale. That makes credit wrappers essential for AI labs and GPUaaS providers.

>Google is providing credit wrappers on Anthropic leases. Checks indicate Anthropic is signing DC leases directly, with Google stepping in to provide credit wrappers on those leases. Anthropic pays Google ~$200M/GW/yr for the backstop, and Google is also taking warrants in the DC companies and projects Anthropic leases from.

>Early signals that MSFT may backstop OpenAI leases in major markets. NVDA leasing 200MW+ directly across multiple requirements and may sub-lease or assign to GPUaaS providers.

>On the enterprise side, agentic AI and customer care workloads are driving record leasing pipelines. 1Q26 enterprise leasing expected to set a record. Enterprise DC pricing rising. Agentic workloads also creating incremental CPU constraints and pushing CPU pricing expectations higher, though not at the pace of recent memory price moves.

New forecasts from BNEF on 2035 PJM energy prices in Virginia’s “Data Center Alley”, relevant to affordability

- No expedited new supply + no flex: ~$88/MWh

- 100% (!) flex from data centers: ~$85/MWh, ~3%🔻

- Build new generation in PJM’s Expedited IX track: $64/MWh, ~27%🔻

- "What if you did both" also $64/MWh ("Base")

Reminder: adding demand w/o new supply = clear higher up the supply curve = higher energy prices

BNEF: 'expedited FTM supply has a larger effect on prices than DR, and the incremental benefits of flexibility diminish beyond a certain point'

But more DR can help in capacity market (note recent participation has trended down) as well as Polar vortex like stress events (note would require 13 GW of data centers flexing)

BNEF expects ~19GW of new avg hourly load in PJM by 2035 from data centers alone

Hard to overstate the role shale gas has played in lowering inflation and spurring American industry. Were we a net importer today as forecast in the 2000s, domestic nat gas & power would be at multiples of current pricing, serving as a huge tax on individuals and companies.

1/5

Robotic solar installation is quickly becoming real. Planted, Maximo and others all deploying automated construction platforms. This Maximo machine just installed 100 MW of solar power https://t.co/M1NSKOSVMT

Great find @ns123abc

Google is backing a multibillion-dollar data center campus in Texas leased to Anthropic, offering construction loans to operator Nexus Data Centers. Initial phase financing could exceed $5B. The 2,800-acre site targets 500 MW by late 2026 with expansion potential to 7.7 GW. Proximity to major gas pipelines from Enterprise, Energy Transfer, and Atmos positions it for behind-the-meter power.

PJM has proposed a bunch of new rules to enable co-location of large loads like data centers with generation.

These are an important start, but in an affidavit to FERC yesterday with @AndrewLevitt7, we identified enhancements to fully achieve FERC/Admin priorities on large loads. I'm an engineer not a lawyer so sticking to the details in planning, where rubber meets the road.

1- PJM is offering co-located non-firm load access to the grid only when co-located gen is on outage. Limiting access to the grid only in outage periods is inefficient: it would push load to only co-locate with baseload resources and precludes peakers/storage, as those would be more expensive than energy in the PJM market in most hours. It is not technology neutral.

Instead: allow non-firm load customers to request non-firm grid reservation in all hours. PJM would still have the right to a) deny a contract during the study phase if even non-firm load cannot be served reliably b) deny reservations based on operational evaluations ahead of time AND c) curtail the load in real time if necessary. There is no adverse impact on reliability from extending the reservation eligibility to all hours but there is a significant benefit in terms of lower costs.

2- PJM's proposal to curtail non-firm load all the way to gross zero results in unnecessary curtailment. PJM should distinguish between curtailments for resource adequacy (RA) and curtailments for Tx security. Curtailment for Tx security should be tied to NET withdrawals from the grid from the load and its co-located generator, not gross load. That would mean 'do-no-harm'.

For RA, it depends. We agree with PJM that if generation has an existing capacity market obligation, it cannot provide RA to the non-capacity backed load so curtailment of gross load makes sense. But PJM should clarify that generation dedicated to the co-located load without a capacity market obligation can serve the load during RA events, so PJM curtailment should be limited to NET withdrawals from the grid.

3- PJM should provide more clarity on interconnection studies for co-located load and supply. What is important: load and generation should be studied independently but in the presence of each other, non-firm load should be studied as dispatchable and incorporated into SCED, and storage + non-firm load should be allowed to nominate joint withdrawal limits to enable maximum contractual and operational flexibility.

We also suggest more reasonable penalties for failure to curtail and implementation of these new co-location options on a faster timeline than June 2029.

Crusoe locked in two battery deals at CERAWeek.

>Form Energy will supply 12 GWh of iron-air storage starting 2027 for future AI campuses. Iron-air systems can reportedly discharge for up to 100 hours using iron, water, and air instead of lithium.

>Redwood Materials is scaling its second-life EV battery microgrid from 12 MW to 20 MW after hitting 99.2% uptime on the original deployment powering modular compute units in Nevada

This should be no surprise. People have been floating these prices for months/years now, bound to materialize at some point.

Roth: "Earlier this year, some were wondering if PJM PPA prices could push past $80-85/MWh. Our checks this past week suggest deals being offered by power generators are now $90 or even $100. Our source comes from a contact connected to utility PPA buyers."

Seems like so many of the corporate deals they do are such large and risky investments that only work in exchange for driving revenue demand. So are margins actually what the income statement shows or is a big chuck of CapEx and JV investment really customer acquisition cost and OpEx? With added risk of creating vampire squid like entity with so many JVs with unclear economics and commitments.

If there’s clearly so much demand to redeem, don’t managers have a fiduciary duty to quickly cut NAV or do tenders at discounts to NAVs as not to wipe out non-redeeming holders?

Seems like under current path at 5% redemptions per quarter they’ll liquidate their best assets first that can sell near NAV while retaining the ones furtherest off.

@negligible_cap Who came up with this concept of LTV on private credit? Value of a non-traded software company is one of the biggest guesses you can make in this whole equation. From a lender perspective, DSCR and leverage ratio seems exponentially more important.