⏰Time for Market Reform!

We look into critical issues with SROs

"Unveiling Conflicts & Advocating for Change in Capital Markets"

The time is NOW to overhaul the system for free & fair markets!

➡️https://t.co/HVUSZTl1kB⬅️

$MULN $GTii $FNGR $COSM $BBBYQ $GNS $GME $MMTLP $MMAT

Oil CEOs Speak Out on U.S. Energy Future and It Confirms What #MMTLP Investors Have Known for Years 🚨

A new Fox Business segment featured Chevron CEO Mike Wirth sounding the alarm on America’s energy future, and it underscores exactly why thousands of us backed Next Bridge Hydrocarbons and the MMTLP spinout: the strategic value of oil in the Permian Basin. 🇺🇸🛢️

🔍 Let’s break this down:

Wirth made it crystal clear the world still runs on oil and will for decades. “This is a business that continues to grow,” he said. “We’re growing production in the Permian Basin, which is one of the most prolific basins in the world.” 🏜️📈

That’s the same region where Next Bridge Hydrocarbons spun out from Meta Materials, which is tied to the halted trading of $MMTLP and the valuable oil leases that retail investors were locked out of. We saw the opportunity before the oil majors openly doubled down.

Chevron is investing billions into Permian operations and acquiring Pioneer to further entrench its position.

🏛️ Washington is now moving in a different direction under the new administration, unleashing oil independence & prioritizing U.S. production again🇺🇸⚡

It was the previous administration’s SEC leadership and climate-first policies that helped create bottlenecks, regulatory confusion, and a culture of suppression, which contributed to the systemic failures that MMTLP investors were subjected to.

And yet, retail investors who had the foresight to back U.S.-based energy companies in West Texas were silenced, delisted, and effectively locked out of one of America’s most strategic energy assets.

💡 We’re told to “move on.” But how can we?

We invested in real assets, in a region now central to national energy security. Our shares were frozen. Trading was halted without warning. FINRA still hasn’t offered a transparent explanation.

🧾 Every piece of evidence from the S1 filings to trustee updates supports our demand for truth and accountability.

Fox just gave Chevron the spotlight to say what we’ve said since 2021:

⚠️ Permian oil = national security. Economic stability. Strategic power. ⚠️

MMTLP was never “just a stock.” It was a retail-driven investment into the future of U.S. hydrocarbons, and we will not let it be erased.

👁️🗨️ This is bigger than market manipulation. It’s about the silencing of everyday Americans in one of the most valuable energy regions in the world.

#MMTLPFIASCO #NextBridge #PermianBasin #EnergySecurity #OilAndGas #Chevron #FINRA #SEC #RetailInvestors #fairmarketsnow 🛢️🇺🇸📢

There was no federal income tax the first 137 years in America was a country.

Everything changed in 1913 with The Federal Reserve Act & 16th Amendment (Income Tax).

America’s wealth was built on productivity, and stolen by usury.

BlackRock’s shell company scam to skyrocket the cost of entire neighborhoods

BlackRock is buying homes at lower values and then selling those homes to themselves, to shell companies, for hundreds of thousands more. Here’s how the scam works

- Step one, the identify middle class neighborhoods with growth potential

- Step two, they buy hundreds of homes in cash, 20 to 30% above asking price

- Step three, regular families can't compete with unlimited corporate cash, they buy about 50+ homes in the neighborhood

- Step four, once they control enough inventory, they sell a few homes to shell companies that they already own with inflated prices, hundreds of thousands over what they bought them for

- Step five, those inflated sale prices become the new market rate

- Step six, your property taxes. And this is where it gets crazy. Your property taxes triple based on these fake sales

“So the Family that saved for 10 years to buy their first home outbid by a corporation with infinite money. The elderly couple who owned their home for 40 years forced out by property taxes they can't afford. Meanwhile, and this is where all the good money comes in for them, BlackRock rents these homes back to the same families they priced out”

“They're stealing the American Dream”

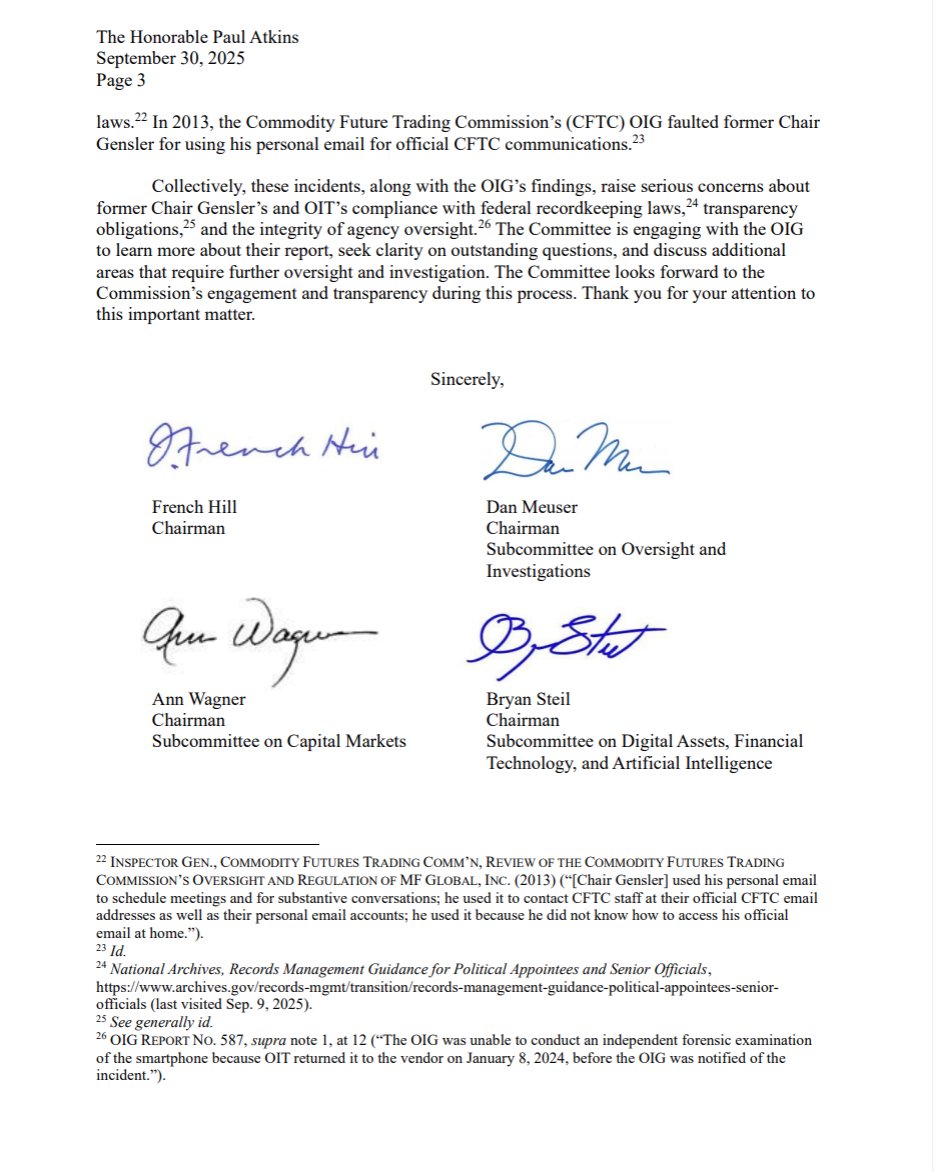

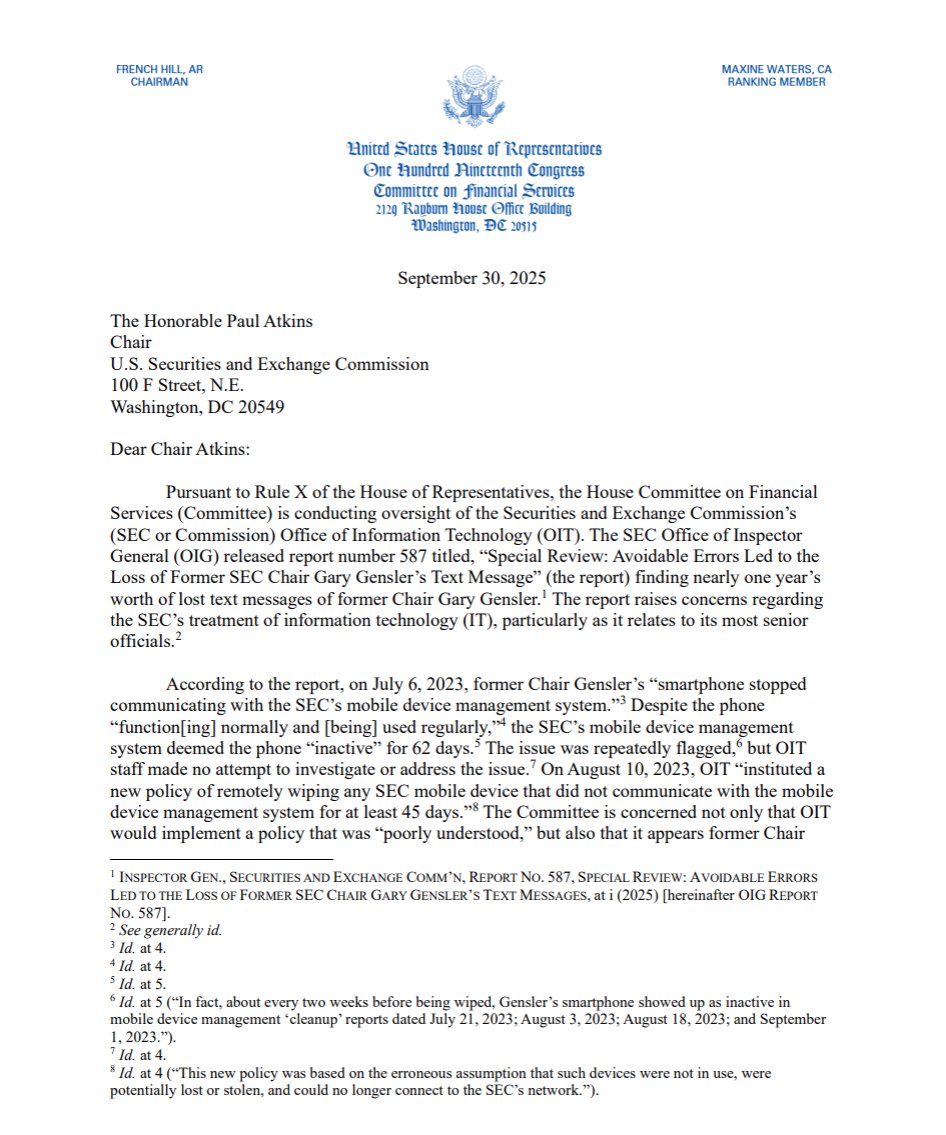

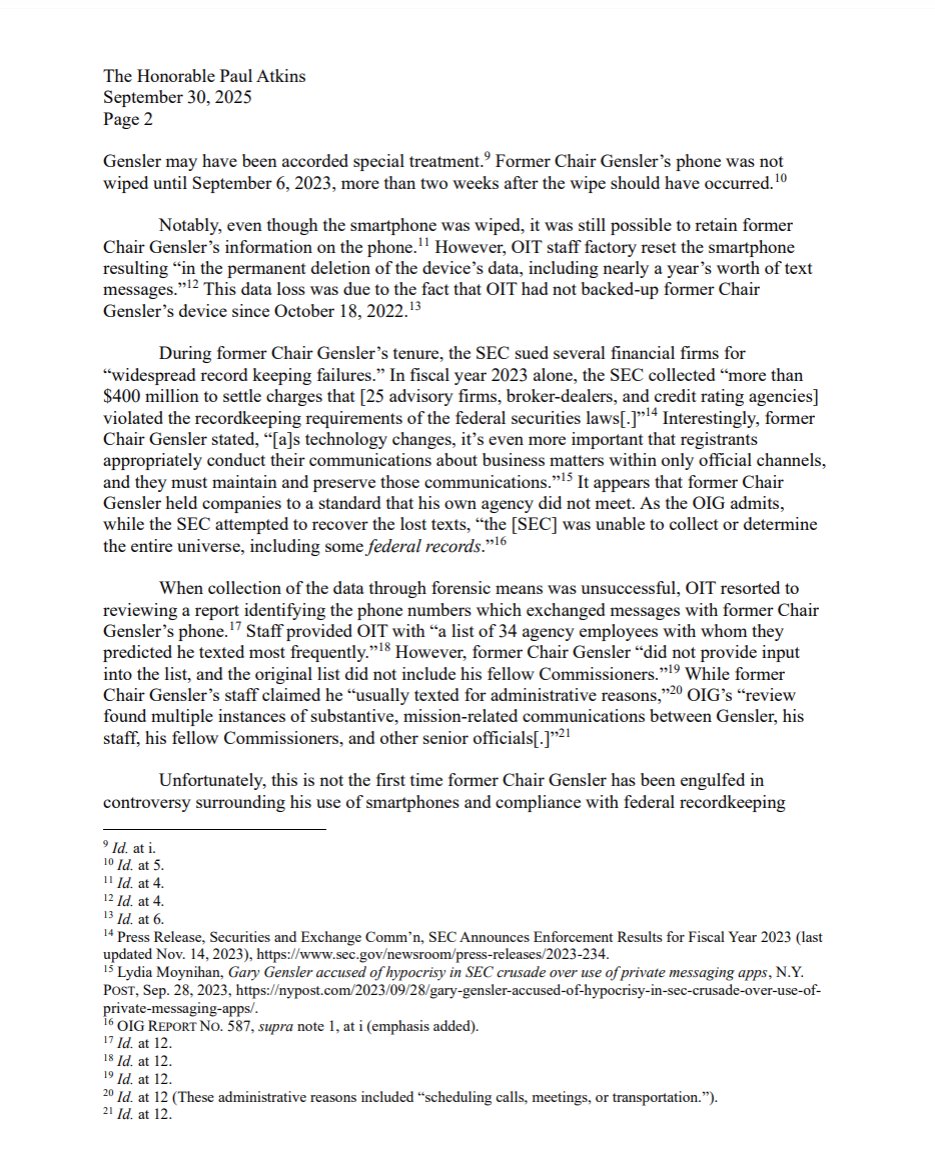

$MMTLP Now @FinancialCmte Chairman @RepFrenchHill is calling for accountability for Gary Gensler’s actions.

French Hill has independent subpoena authority as Chair of the Financial Services Committee. Former SEC Chairman Gary Gensler has lied incessantly for years. It’s beyond time to get the truth.

https://t.co/ya0hPWFRK2

NEW: Chairman @RepFrenchHill, @RepMeuser, @RepAnnWagner, and @RepBryanSteil sent a letter to @SECGov Chair @SECPaulSAtkins to raise concerns about the SEC’s mishandling of former Chair Gensler’s text messages and calls for stronger oversight to ensure compliance with federal recordkeeping laws.

Read more ⬇️🔗

https://t.co/Q75er4wtKh

🚨META MATERIALS BK TRUSTEE FILES OPPOSITION TO CITADEL SECURITIES LLC, ANSON FUNDS MANAGEMENT LP, AND VIRTU FINANCIAL, LLC’S MOTION TO QUASH AND/OR FOR A PROTECTIVE ORDER. DECLARATIONS IN SUPPORT OF TRUSTEE'S MOTION FILED, BURNETT'S INDICATES SCHWAB, TD AMERITRADE, TRADESTATION, THINK OR SWIM AND NASDAQ ALL TURNED OVER DATA IN RESPONSE TO SUBPOENAS. DTCC STILL NEGOTIATING FOR DATA TRANSFER.

TRUSTEE ARGUES: “As the Rule’s text makes clear, the scope of a Rule 2004 examination is unfettered and broad; the rule essentially permits a fishing expedition.... And the examination may extend to third parties who have had dealings with the debtor....Rule 2004 allows for pre-litigation discovery, prior to initiating any adversary proceeding in bankruptcy."

OPPOSITION MOTION: https://t.co/VIFJtqjtzS

BURNETT DECLARATION: https://t.co/ih0EETcm3W

LOVATO DECLARATION: https://t.co/IyxZ3xzKV8

$MMTLP $MMAT $TRCH @Metamaterialtec

🚨META MATERIALS BANKRUPTCY JUDGE RESIGNS FROM CASE, ASSIGNED TO NEW JUDGE GARY SPRAKER. TRAUDT/SPEARS HEARING SCHEDULED FOR TODAY CANCELLED.

$MMTLP $MMAT $TRCH

I hope the retail AMC and GME and MMTLP community understands the reason we’ve had zero action so far in combatting financial market terrorism is because we picked a fight with people at the same level @MikeGil21446788 picked a fight with

It’s rotten to the core and we’re fighting the most powerful people on planet earth

Thankfully, I’ve been told the @DOJCrimDiv now understands the scope of the corruption and that they will step in— even if the oversight orgs and regs are afraid to

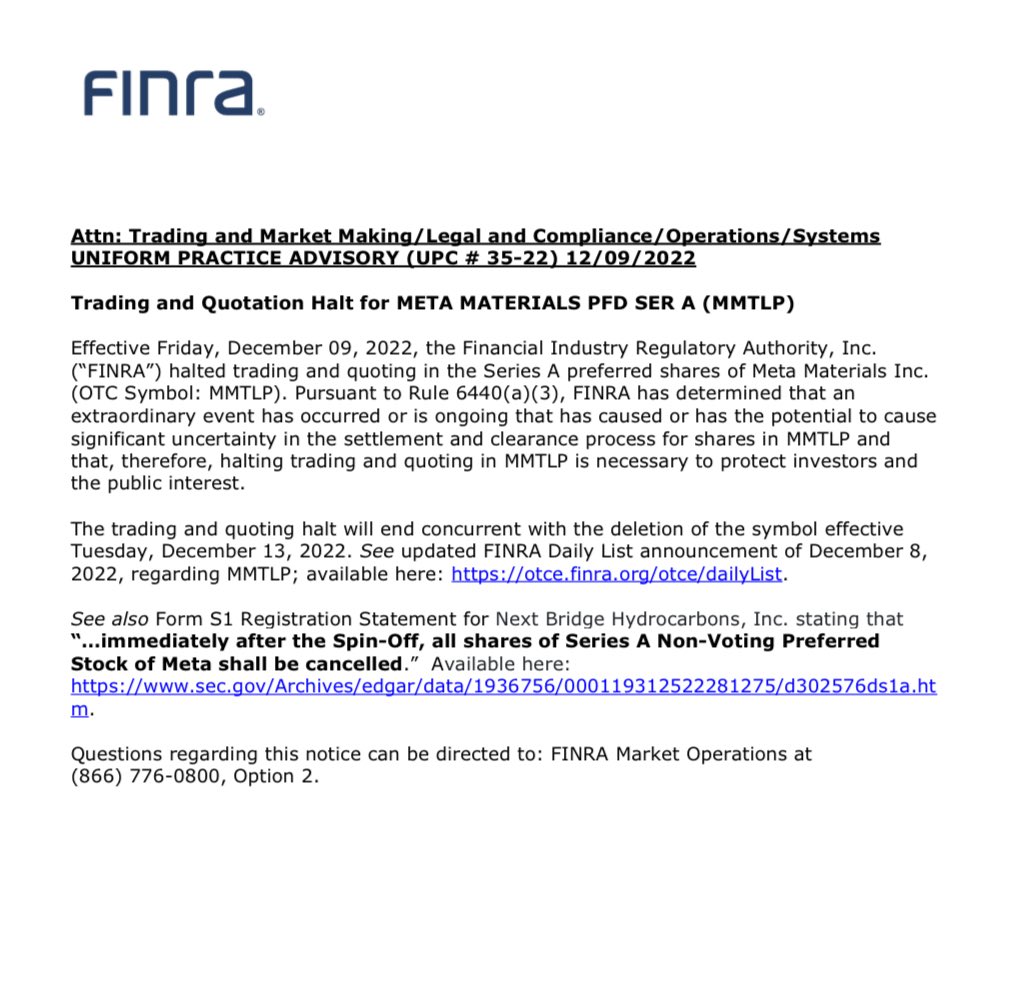

BREAKING🚨 NEXT WEEK WILL MARK 1,000 DAYS SINCE FINRA HALTED $MMTLP

➡️ FINRA abruptly halted $MMTLP on Dec 9, 2022, citing an “extraordinary event.” Regulators have never explained the extraordinary event to this day or approved the companies S-1

They are picking and choosing how to shape the narrative and context.

The @SECGov LITERALLY ADVISED META HOW TO DEAL WITH THE 🐂💩3RD PARTY LISTING OF THE PREFERRED SHARE BY FILING A FORM S1 TO SPIN THE SHARES OUT INTO A NEW PRIVATE (15D), PUBLIC REPORTING(DUE TO THE SIZE OF SHAREHOLDER BASE EXCEEDING 500 PEOPLE) COMPANY, AND IN ONE OF THE AMMENDMENTS, ACTUALLY INSISTED THAT THEY ADD SHORT SQUEEZE LANGUAGE(!) TO THE S1 REGISTRATION FOR THE SPINOUT!

Then they approved it, made the spinout effective and published the company's PROSPECTUS 424B, only for FINRA to VIOLATE THEIR RULE 6490 - TO IGNORE THE LANGUAGE THE COMPANY HAD LAID OUT IN THE PROSPECTUS...

...WHICH THE SEC APPROVED! This CANNOT BE OVERLOOKED...

and create their own language, further violating their rule 6490 by not deeming the corporate action deficient, only to break 6490 AGAIN(!) by revising the corporate action less than 48 hours later and THEN... U3 HALTING their revised corporate action freezing everyone's money in open position!

FINRA AND THE SEC SHOULD STAND FOR "F*** IDIOTS, NOT RETAIL ADVOCATES, AND "SURREPTITIOUSLY ENABLING CRIMINALS", respectively.

HOW CAN ANYONE TAKE THESE CHARGES SERIOUSLY WHEN WE HAVE FOIA's THAT SHOW THE SEC WORKED IN CONCERT WITH @FINRA

ON THIS BEFORE, DURING, AND AFTER THE HALT!?

THESE REGULATORS ARE BLATANTLY CROOKED!

I would LOVE @elonmusk, @lexfridman to weigh in on this. This is the poster child for #RegulatoryCapture.

This is #RICO! We have receipts!

BlackRock and Private Equity Firm housing scam EXPOSED

- They are buying up entire new housing developments, sometimes 500 units

- They’ll buy the houses at $300k per home

- They won’t sell it right away, they’ll keep the area looking like a construction zone for a year

- Let’s say there are 3 different models of homes in the community they bought, then a year later they’ll sell 3 of those houses that they bought for $300,000 to themselves in another fund for $700,000

- That creates 3 comps in the neighborhood

- They do one of each of the models, and now the entire neighborhood, each house is valued at $700,000

- Then they're going to turn them into obscene rentals and simultaneously they're going to have a 2.5x value on that portfolio to borrow against

“And every American in that community was just priced out of everything around that community.”

Today , InvestorTurf officially accuses the DTCC, DTC, and NSCC of orchestrating the biggest fraud in stock market history, and we demand action from the Trump administration.

InvestorTurf accuses the market-plumbing complex—DTCC and its two key arms, DTC and NSCC—of enabling the large-scale manufacture and concealment of “counterfeit” shares created through naked short selling. The DTCC is the broker-dealer-owned holding company, with DTC acting as the depository that holds almost all certificates in its nominee name and keeps member and customer sub-accounts as electronic entries, while NSCC is the central clearer that guarantees settlement and runs the stock-borrow program and Continuous Net Settlement (CNS). This structure lets trades “settle” even when the seller never delivers a real, borrowed share, so the buyer is credited with what call counterfeit share, yet the system treats it as if it were genuine.

NSCC’s stock-borrow and CNS netting process allows the same pool of real shares to be booked across multiple customer accounts at different brokers, inflating the effective float. NSCC guarantees trades and cures fails-to-deliver by borrowing from brokers’ net surpluses at DTC; because only net differences move, the lending broker doesn’t remove specific shares from any named customer, but the borrowing broker credits specific customers—so identical shares appear in more than one account. As long as members keep settling only their net obligations, the system never reconciles to the issuer’s true share count. This “CNS” layer hides “billions” of such counterfeit shares from Regulation SHO, with issuer-level CNS totals available only if DTC is successfully subpoenaed—and even the SEC does not routinely receive those tallies.

DTC is burying historic fails and providing mechanisms that let positions evade buy-ins and clocks. There is a case where roughly 400 million naked shorted shares that “should” have been bought in after a major player’s collapse were instead absorbed into DTC’s system and effectively “grandfathered” into legitimacy, permanently diluting issuers while no longer appearing as fails. The DTC runs or condones programs (described as RECATS) that alert members when positions are about to become fails so they can be shipped offshore or matched elsewhere and then returned with clocks reset—repeating as needed to keep positions naked and out of sight. When public and political pressure forced closure of the formal “grandfather” loophole in 2007, DTC and brokers simply migrated large blocks out of DTC to ex-clearing, where the same economic exposure persists but falls outside what regulators track.

Finally, this plumbing doesn’t just tolerate abuse but powers it at scale: by treating borrowed-from-DTC credits as legitimate and netting away gross imbalances, NSCC and DTC provide a standing reservoir of synthetic supply—ten to twenty times larger than the publicly visible fails in targeted names—that can be drawn on to overwhelm buy pressure, depress prices, and even push companies toward distress, all while appearing settled and compliant on the surface. This reserve of “strategic fails” gets created and maintained alongside profitable stock-lending and one-day “borrows,” and “friends” at the DTC and major clearinghouses” are part of a repeatable playbook used during coordinated short campaigns.

Blackstone didn't buy 274,000 homes to be landlords.

They spent $1 trillion turning homeownership into subscription housing.

They are creating a generation that will own nothing and rent everything.

While families dream of white picket fences, Wall Street dreams of permanent tenants 🧵

MMTLP SHOUT OUT TO @EleanorTerrett (fOXBusiness news ) for her bold reporting on MMTLP! She’s calling out the SEC & FINRA for stonewalling media & Congress, exposing a serious regulatory issue. Keep pushing for transparency! FINRAFRAUD. Time to investigate FINRA CEO robert W Cook.

It looks like FINRA counted on $MMTLP investors NOT finding out about Kit Digital $KITD.

The whole "Oops, we forgot to protect investors that might be able buy after December 8th" excuse!

Yeah, that only works the first time it catches you off guard!

Context in the full video linked below 👇🏾 @SECPaulSAtkins@HesterPeirce@FBIDirectorKash

IT’S TRUE 🚨 Proof the reason veterinarian bills for your pets have skyrocketed recently is because Private Equity Firms have been buying up all the veterinarian clinics throughout America and then raising prices

“Massive corporations and private equity firms have been taking over vet care at an alarming rate, owning up to 50% of clinics and up to 75% of emergency hospitals. They're also snapping up pet insurance companies and even pet food brands.”

“If you're a pet owner, you've probably been noticing that your vet bills have become more and more and more expensive over the years. But it's even worse than you might think. The cost of vet care has gone up by 60%”

“The veterinary industry is a f***ing racket. Animal health care is a f***ing scam. When I started looking into it, I found endless complaints of vet bills through the roof, unexpected charges, and people feeling like they had no choice but to pay up. Veterinary medicine is the gold rush of 2024. I call it the rise of Big Vets.

These massive private equity firms are buying up veterinary clinics in the hundreds all across the United States. We talked to veterinarians and journalists to find out exactly why your vet bill has gotten so high”

“As private equity firms buy up even more clinics and expand into other pet services. Just last year, private equity company Blackstone purchased Rover. It's an online pet sitting and dog walking company. And Jap Consumer Partners is buying up pet insurance.”

All the evidence is in this video, prices are expected to keep rising as private equity firms take over what’s left of the vet care industry

This MUST be stopped. Why is American Government allowing private equity firms to buy everything and DESTROY Americans way of life by skyrocketing prices

‘Private Equity's Ruthless Pet Care Scheme’ - More Perfect Union

🚨HALTED: MMTLP The Scandal They Can’t Explain — and Won’t Investigate.

This is not just a trading halt. This is one of the biggest coverups in modern U.S. market history. Here’s the truth — every date, every document, every name. No more hiding.

📆 October 2021 – The Unauthorized Birth of MMTLP

Somehow, a non‑tradable preferred share dividend placeholder — $MMTLP — appeared for public trading.

Key facts:

- Meta Materials (MMAT) never authorized MMTLP to trade.

- No effective S‑1 registration existed to allow lawful public trading.

- Despite this, @FINRA approved trading and assigned a symbol.

The unanswered questions:

- Who authorized the listing?

- Who paid the initial listing and renewal fees?

- Why won’t FINRA disclose this?

Former $MMAT CEO John Brda immediately raised concerns. @OTCMarkets told him: “Take it up with FINRA.” FINRA told him: “You’re no longer CEO, you have no standing.”

When Meta Materials formally requested that FINRA delist MMTLP due to lack of authorization, FINRA refused — keeping the ticker alive and tradeable.

This opened the door for broker‑dealers to trade and short MMTLP freely, including synthetically created shares with no corresponding real share. These synthetic shares flooded the market without settlement audits or investor warning — a glaring breach of SEC Rule 15c2‑11 and a potential case of collusion or even RICO violations if coordinated between multiple parties.

📆 2022 – The Synthetic Storm

As trading continued, MMTLP’s market activity turned into a glaring anomaly.

The facts regulators can’t deny:

- Abnormally high short volume persisted throughout 2022, despite MMTLP being a preferred equity security with a fixed share cap.

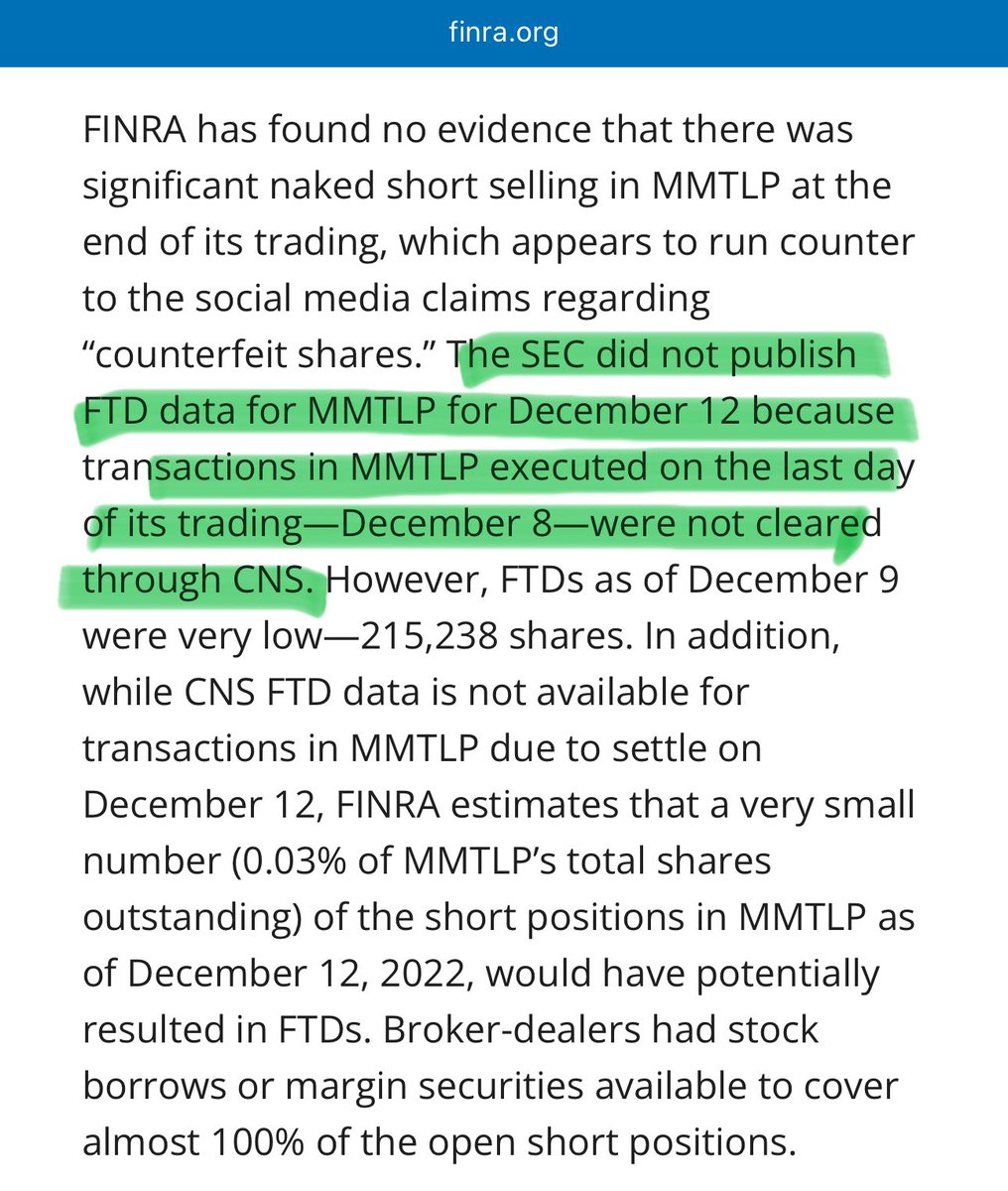

- There was no evidence of T+2 settlement audits being performed.

- Fails‑to‑deliver (FTDs) were never publicly disclosed to investors, depriving them of essential transparency.

MMTLP was heavily shorted and rehypothecated across multiple platforms, meaning the same shares were pledged and re‑pledged — creating synthetic supply well beyond the legitimate float.

Regulatory breakdown:

- FINRA took no action to investigate FTDs or naked shorting, despite clear obligations under SEC Regulation SHO.

- In an astonishing admission, FINRA later acknowledged it had incorrectly published MMTLP on its Threshold Securities List twice in 2022 — somehow missing it at key times when trading data suggests it should have been included.

This isn’t a “clerical error.” The omission hid persistent settlement failures from public view — shielding abusive short selling from scrutiny and allowing the problem to snowball.

📆 July–December 2022 – From Spinout to Sudden Halt

July 2022 – Meta Materials (MMAT) files a Form S‑1 to spin out its oil and gas assets into a private company, Next Bridge Hydrocarbons (NBH).

🔹 Over the next months, the S‑1 goes through four revisions, shaped by @SECGov comments and scrutiny.

🔹 By November 2022, the SEC declares it effective, paving the way for a clean, lawful spinout and a straightforward T+2 settlement process.

🔹 Throughout this, FINRA — fully aware and engaged in the process — raises no public objections and issues no warnings about the settlement process

Everything appeared set for an orderly transition: MMTLP shares would convert into NBH, the ticker would be deleted, and settlement would occur in line with the corporate action.

📆 December 6–8, 2022 – FINRA issues a corporate action notice stating MMTLP shares will be canceled on Dec 13.

- DTCC schedules the symbol deletion accordingly.

- Multiple broker‑dealers send written assurances to clients that trading will continue through Dec 12.

📆 December 9, 2022 – Without any advance notice to the public, FINRA abruptly halts MMTLP trading under U3 code (“extraordinary event”).

🚨 Key Violations & Red Flags:

- FINRA Rule 6470 requires that halt notices for OTC securities be disseminated to the public in advance — no such notice was given.

- The decision was made by the FINRA Uniform Practice Committee (UPC) — a group that includes broker‑dealers who may have had direct exposure to massive uncovered short positions in MMTLP.

- The halt trapped thousands of retail investors, denying them the ability to sell or convert their positions to NBH shares.

The same committee with members potentially responsible for the overselling of MMTLP was in charge of the decision to freeze all trading — conveniently locking in the imbalance and preventing market resolution before the spinout.

📂 FOIA Revelations – The Smoking Gun Emails

Multiple Freedom of Information Act (FOIA) requests have pried loose internal SEC and FINRA communications that blow apart the “nothing to see here” narrative.

What they show is damning:

📆 Nov 2021 – Regulators were aware of MMTLP’s illegitimate OTC listing almost immediately after it appeared. Concerns were raised inside FINRA, yet no action was taken to remove the unauthorized ticker.

📆 June 2022 – FINRA internally escalates regulatory risk warnings about MMTLP, indicating that the issue had moved beyond mere clerical oversight and into active risk management territory.

📆 Dec 5, 2022 – FINRA Senior VP Sam Draddy sends an urgent request for comprehensive trade data (blue sheets), explicitly citing “fraud and manipulation” in MMTLP.

They knew days before the Dec 9 halt that market integrity was in jeopardy — and yet, no public warnings were issued.

📆 Dec 12, 2022 – Just three days after the trading halt, a high‑level FINRA–SEC meeting is set via Zoom. Attendees included:

- Robert Colby – FINRA Chief Legal Officer

- Stephanie Dumont – FINRA Market Regulation

- Racquel Russell – FINRA Communications & Government Affairs

- David Shillman, David Saltiel, Jeffrey Mooney – SEC Division of Trading & Markets

- Mark Donohue – Senior SEC Policy Advisor

This was post‑halt crisis management.

The presence of top legal, regulatory, and communications officials signals this was a coordinated damage‑control effort, not a routine review.

The timing strongly suggests regulators were working to align legal posture and craft a unified public narrative while the issuer, retail investors, and even some brokers were still in the dark about why the Dec 9 halt occurred.

This wasn’t transparency. This was containment — behind closed doors, between agencies, with no meaningful communication to the public whose assets had just been frozen.

📆 March 16, 2023 – The “FAQ” That Wasn’t

Without fanfare, FINRA quietly posted an anonymous “FAQ” on its website, claiming to explain the $MMTLP trading halt. No named author. No press release. No accountability.

FOIA documents tell a different story:

- The FAQ was authored and circulated by Robert Colby, FINRA’s Chief Legal Officer — not investor education staff.

- It was sent directly to SEC leadership:

Haoxiang Zhu – SEC Director, Division of Trading & Markets, David Saltiel – SEC Deputy Director, David Shillman – SEC Associate Director, Heather Percival – Policy Counsel, Office of the SEC Chair

This was not retail investor guidance. This was high‑level regulatory coordination — crafted at the executive legal level, which signals FINRA knew this wasn’t just a “routine halt.” It was a serious legal and political crisis.

🧨 Key Misrepresentations in the FAQ:

1️⃣ “FINRA couldn’t give advance notice of the halt.”

Debunked: They could, and they should have. Rule 6470 and precedent show that OTC halts can be announced in advance when no imminent market disruption exists.

2️⃣ “No reconciliation was needed before the halt.”

Debunked: NBH and multiple brokers later admitted that accounts were oversubscribed — meaning more positions existed than legitimate shares available.

3️⃣ “Short interest was managed and not a concern.”

Debunked: Brokers openly acknowledged they do not hold NBH shares to cover positions, revealing that reported short interest grossly understated true market exposure.

Why this matters:

The March 16 FAQ reads less like an explanation and more like a legal cover‑your‑ass memo. The fact that it was distributed to SEC leadership before public posting — without attribution — suggests the agencies were aligning narratives to minimize liability, not to protect investors.

📂 FIF Meetings – Coordinated Silence

Public records reveal repeated meetings of the Financial Information Forum (FIF) in 2022 involving:

- FINRA, SEC, Large broker‑dealers — many of whom have representatives on the FINRA Uniform Practice Committee (UPC), the same committee that issued the Dec 9 U3 trading halt on $MMTLP.

Meeting agendas confirm that MMTLP and Next Bridge Hydrocarbons (NBH) were discussed multiple times throughout 2022. And yet:

- No public disclosures of these discussions.

- No settlement audits ordered.

- No proactive measures to protect retail shareholders from exposure to massive unsettled positions.

💥 The TradeStation Moment

During one FIF session, TradeStation addressed a recent Next Bridge S‑1 filing — the one that would distribute non‑transferable subscription rights only to holders who register their NBH common stock directly with the company’s transfer agent.

The hypocrisy?

This is the same TradeStation that has told its customers it cannot honor ownership of NBH because the shares were lent out and “aren’t backed by a physical certificate.”

The implication:

- UPC committee members (including conflicted broker‑dealers) were in closed‑door discussions with FINRA and the SEC months before the halt.

- They had ample opportunity to address ownership imbalances and settlement risk.

- Instead, they said nothing publicly — and then the same network of insiders made the decision to freeze trading, locking in the imbalance and protecting their own exposure.

📆 The Ongoing Cover‑Up – Two Years and Counting

The aftermath of the $MMTLP halt has exposed blatant gaps in accountability — and a coordinated effort to keep those gaps hidden.

The facts they can’t spin:

- TradeStation and Schwab have openly admitted to customers: they do not hold the NBH shares that should correspond to client accounts — in some cases because they were lent out, in others because they were never backed by a physical certificate to begin with.

- Next Bridge Hydrocarbons (NBH) itself has confirmed there are buyers seeking to purchase well over the 2.65 million short shares FINRA officially reported — proof the market imbalance is far greater than regulators have admitted.

- In FOIA responses, FINRA has confessed it does not track overseas synthetic liabilities — a convenient blind spot when synthetic shares can be created and parked offshore to dodge settlement.

Congressional Pressure – Ignored

- Congressional offices have now received tens of thousands of letters, calls, and emails from impacted investors.

- Over 15 formal congressional letters — including a bipartisan 74‑member demand — have called for answers, audits, and hearings.

Regulatory Evasion

- Gary Gensler (SEC Chair) has repeatedly punted responsibility to FINRA.

- FINRA claims it lacks audit authority — a blatant falsehood, since FINRA Rule 4140 explicitly gives them the power to demand and conduct an audit of share positions.

- The SEC hides behind the phrase “ongoing investigation” — an excuse it has used for nearly two years without producing a single page of public findings.

No hearing. No public audit. No sworn testimony from the decision‑makers who froze the market.

This is not regulatory oversight. This is regulatory paralysis — or worse, regulatory protectionism for the very entities that created the imbalance. Every day without an audit is one more day the truth stays buried.

⚖️ Regulatory & Legal Violations – The MMTLP Case File

What happened with $MMTLP isn’t just “controversial” — it’s littered with clear rule breaches and systemic conflicts of interest:

📜 FINRA Rule Violations

- Rule 6490 – Unauthorized alteration of issuer‑submitted corporate action notice. FINRA unilaterally changed Meta Materials’ Dec 6, 2022 corporate action notice after private calls with DTCC — without issuer consent — in direct violation of its own rule.

- Rule 6440(a)(3) – Misuse of halt procedures (U3) without proper notice or justification. Halt was issued with no market‑wide imminent disruption explanation — instead protecting short positions from settlement.

- Rule 6470 – Failure to issue public halt notice in advance for OTC securities. Retail received no warning. Brokers were blindsided. Liquidity was trapped.

- Rule 2241/2242 – Improper sharing of material nonpublic information. FINRA insiders on the UPC Committee — some from broker‑dealers with exposure — participated in halt decision‑making with full knowledge of outstanding liabilities.

- Rule 2010 – Failure to observe high standards of commercial honor and equitable trade.

Issuer requests ignored. Investors locked out. Imbalances left unresolved.

- Rule 4140 (Audit Rule) – False claim of no audit authority. FINRA publicly claimed it couldn’t perform an audited share count — yet this rule explicitly empowers them to demand and conduct one.

- FINRA UPC Charter – Conflict of interest in decision‑making. Halt decision was made by a committee including members from firms potentially responsible for the over‑shorting of MMTLP.

📜 SEC Rule Violations

- SEC Rule 15c2‑11 – Allowing quotes and trading without issuer compliance. MMTLP was listed and traded despite no effective S‑1 and without issuer authorization — a direct breach.

- Reg SHO Rule 203(b)(1) – Failure to locate shares before shorting. Market saw massive fails‑to‑deliver, with synthetic positions openly admitted by brokers and confirmed in bluesheet data.

- Section 10(b) of the Exchange Act – Fraudulent and manipulative market behavior. Repeated omission of material facts to the public, misrepresentation of share reconciliation status, and concealment of settlement risk.

📜 Other Breaches

- Investor Protection Standards – Investors were denied the right to exit, offered no compensation, and no reconciliation for overages was performed.

- FOIA Transparency Standards – Systematic delay, redaction, and outright denial of public information requests, concealing regulatory discussions and decision processes.

- Breach of Fiduciary Duty – Broker‑dealers knowingly oversold positions they could not deliver, creating liability for customers and systemic settlement risk.

- Failure to Deliver (FTD) / Synthetic Share Abuse – Confirmed through FINRA’s own blue sheet data and FOIA admissions; unresolved to this day.

🚨 The $MMTLP Halt – Not Routine, Not Accidental

The December 9, 2022 halt of $MMTLP was not a routine market safety measure — it was a coordinated containment maneuver designed to lock in an unresolved imbalance and shield the system from exposure. It was:

- A coordinated freeze to contain systemic risk — executed by a FINRA committee with members from the very broker‑dealers potentially responsible for the overselling of MMTLP.

- A regulatory failure involving multiple agencies — the SEC, FINRA, DTCC, and conflicted market participants, all with foreknowledge of settlement risk, yet no preemptive action.

- A breach of public trust — denying thousands of investors access to their lawfully held shares and, in effect, freezing constitutional property rights without due process.

The burning questions regulators can’t answer:

- If this was “routine,” why so many closed‑door meetings before and after the halt between FINRA, SEC, and brokers?

- Why the FOIA denials, heavy redactions, and multi‑month delays in producing basic records?

- Why the legal shielding and refusal to provide transparency to courts, Congress, and the investing public?

This wasn’t routine. This wasn’t transparent.

It took retail investors, citizen researchers, and whistleblowers to uncover evidence that Congress and regulators have refused to surface themselves — from internal emails, to meeting agendas, to proof of massive short exposure.

And that fact alone should terrify anyone who still believes the market is fair.

📢 We Demand Immediate Action

1️⃣ A Full Congressional Investigation

- Armed with subpoena power to compel the release of all FINRA and SEC internal communications related to $MMTLP.

- Inclusion of a whistleblower protection and review process so insiders can safely disclose what they know.

- Pursuit of legal accountability if evidence confirms market manipulation, negligence, or regulatory misconduct.

The timeline is clear — this was a deliberate closing of ranks after something broke that could not be fixed before the deadline.

2️⃣ A Full Public Audit

- An independently verified audit of all $MMTLP short positions, synthetic shares, and trade settlements, both domestic and offshore.

- Inclusion of blue sheet data and reconciliation across all clearing firms, not just U.S. markets.

3️⃣ Sworn Testimony Under Oath from Key Figures:

- Robert Colby – FINRA Chief Legal Officer

- Stephanie Dumont – FINRA Market Regulation

- David Shillman – SEC Trading & Markets

- Haoxiang Zhu – SEC Director of Trading & Markets

- Patti Castimates – FINRA Transparency Services

- Various FINRA UPC Committee Members – including those from broker‑dealers with potential conflicts of interest

🔥 Final Thought:

If there’s truly nothing to hide… Then show us the shares. @RepOgles@MarshaBlackburn@AGTennessee@RepJohnRose

💬 To the loudest voices trying to bury $MMTLP:

- You say it’s worth nothing.

- You say it’s over.

- You say it’s dead.

- So why are you still here?

There are literally thousands of actively trading tickers you could waste your breath on… and yet, you keep circling this one — the one you insist is “finished.”

Here’s a thought: why don’t you join us in demanding a full, independently audited share count?

If you’re so confident there are no overages, no unsettled positions, no synthetic or counterfeit shares… this is your chance to prove it. Show the world how “right” you are.

But you won’t.

Because deep down, you already know:

That audit won’t prove you right.

It will prove we were right.

And until that day comes… drip… drip… the truth keeps leaking out — and with every leak, the cover‑up looks worse.

⚠️ Disclaimer

The following outline is compiled exclusively from publicly available information, including:

- Documents obtained via the Freedom of Information Act (FOIA)

- Publicly issued FINRA and SEC FAQs

- Corporate disclosures

- Broker communications

Every detail included is sourced from verifiable, unclassified public records.

This summary represents only a fraction of the full picture. To date, thousands of FOIA requests have been denied, heavily redacted, or delayed without justification. Imagine the scale of the story — and the level of accountability it could demand — if full transparency were granted.

The American investing public deserves answers.