Ever wondered how some companies grow stronger because they cut prices? $wise $dlo

Most businesses fight to raise margins. But there’s a rare type of company that flips the script.

It’s called the Flywheel Effect of Shared Economies of Scale 🧵

Nick Sleep returned 921% over 13 years at Nomad by mastering a single, counter-intuitive concept:

Scale Economies Shared.

To measure it, he invented the "Robustness Ratio" – a tool that calculates exactly how much value a company gives back to its customers relative to what it keeps for shareholders.

Costco $COST famously operates at a ratio of around 5:1 (back when Sleep did his calculations at least).

"At Costco, we think the customer saving is around five dollars, compared to shopping at most supermarkets, for every dollar retained by the company."

But there’s a fintech disruptor that just listed in the US that is weaponizing this exact formula today at an even higher clip; a firm led by @kaarmann that just listed on the NASDAQ last week. In $WISE's NASDAQ listing presentation, we got some fresh numbers, helping me to update the robustness ratio Wise produces.

So let’s update my calculations on Wise ($WISE) from around two years ago (I'll link my post from back then in a comment below).

Back then, in FY23, Wise saved its customers £1.5 billion while retaining £114 million in net income – yielding a jaw-dropping robustness ratio of 13.2.

It was a textbook example of a company aggressively choosing market share and customer goodwill over short-term margin gouging.

How does that "moat" look today? Let's refresh the math using their latest financial disclosures:

✅ Customer Value Proposition (Savings): $3.3 billion

✅ Preliminary FY26 Revenue Estimate: $2.5 billion

✅ Net Income Margin: 18% (based on their H1 FY26 financial profile)

✅ Estimated Net Income: $450 million

Robustness Ratio = $ Retained for Shareholders / Customer Value Proposition (Savings or Benefits)

So when you divide that $3.3 billion in customer savings by the estimated $450 million in shareholder profit, Wise lands at a current robustness ratio of 7.33.

This decline in the Robustness Ratio isn't a sign of Wise losing its edge – it's the footprint of a business successfully diversifying its empire. Back in FY23, cross-border remittance was Wise's main engine, driving around 70% of total revenue. Today, cross-border has stepped down to 52%, while Interest Income and Card Services have scaled up to command a massive 48% combined share of the mix. Even with these new profit centers lifting shareholder returns, a robustness ratio of 7.33 is an absolute powerhouse. It means that for every $1.00 Wise retains in profit, it still leaves over $7.00 in its users' pockets compared to traditional banks.

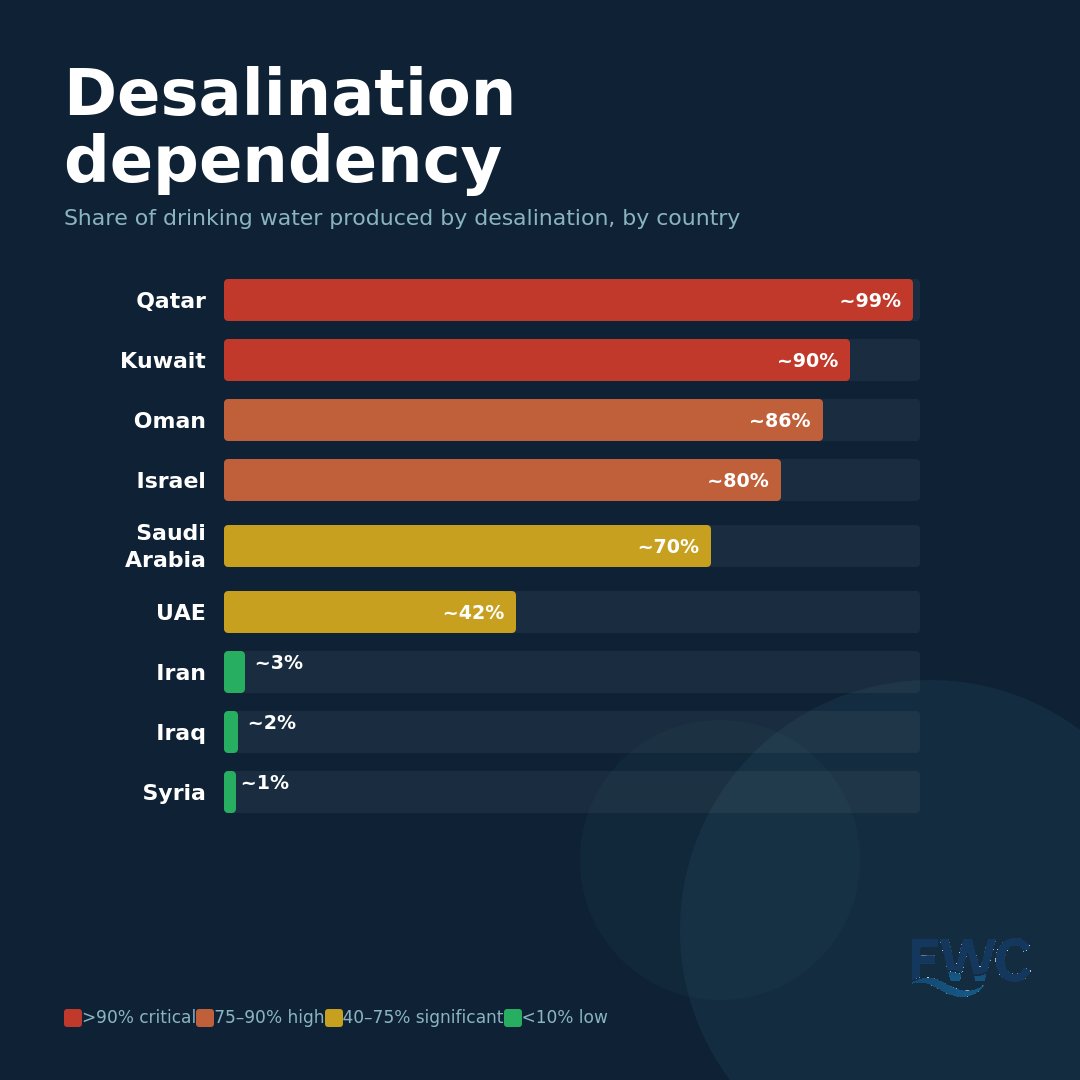

Around 400 desalination plants in the Gulf produce roughly 40% of the world's desalinated water, with a significant share concentrated near the Strait of Hormuz.

That concentration creates vulnerability. And in modern warfare, vulnerability gets weaponised.

Qatar depends on desalination for ~99% of its drinking water. Kuwait ~90%. Iran? ~3%.

That gap is a strategic advantage.

An interesting article:

https://t.co/xSK00ndVaB

I've just been listening to the Andrew Dudum $hims interview with Harry Stebbings.

Interesting comments from Andrew when asked about about the exposure of the core business to GLP1s. His reponse...

Everyone said Hims was just an ED company. Then a hair loss company. Then a weight loss company. A year from now they'll call it a peptides company.

Peptides will become the next growth engine.

And the reality? Hims is now a platform with 12+ segments scaling simultaneously.

The narrative chases the headline. The business builds the future.

Former Constellation Software Portfolio Head on why software is much more than the cost of writing code $CSU $TOI :

AI dramatically lowers the cost and time to write software. That software development capex moat erodes to zero in an extreme case. Then what happens is all of the other moats around a software business are still very much intact to the extent they have them. I'll give you an example. If you're mission-critical software serving a vertical market like defense, which is also regulated workflow, you need to be certified as a software provider. Your customers need to trust you with not just the workflow but also the data. In that incumbency position, you are in an ideal spot to adopt the technology and drive better margin internally as well as better value for your customer by building new product. The likelihood of an AI-native startup encroaching in your territory is still there, but it's low - it's too hard. You have much more time. However, if you are selling a web app, like a productivity app that appends itself to Outlook to help you schedule meetings, I think your monetization is going to go to zero pretty quickly, or Outlook is going to roll out that feature. One person could build that in an hour. Stay away from those types of businesses.

Wise expanding deeper into Thailand $wise $wise.l

‘first nonbank to secure the five licenses required to operate locally, including regulatory approvals from the Bank of Thailand and The Ministry of Commerce’

This strengthens Wise’s presence in Asia-Pacific 👌

Revenue from this geography currently make up 16% of its total revenue

Wise’s new licences in Thailand enable full integration with domestic payment infrastructure, allowing it to connect directly to systems such as PromptPay and Thai QR payment networks. This means transfers can be executed via real time local clearing rails rather than correspondent banking networks, enabling instant or near instant THB settlement, lower FX and processing costs, and improved payment reliability.

Hold THB, receive via PromptPay, pay with QR like a local account. Wise will have lower costs, fewer intermediaries and deeper integration into Thailand’s payment system.

Changes take effect after 19 May 2026

https://t.co/8r6tp8x7KT

🇳🇱 Topicus $TOI is Europe’s quiet compounder.

It owns 100+ niche vertical market software (VMS) businesses across 40 sectors in 26 countries.

These aren’t flashy SaaS plays — they’re mission-critical, deeply embedded, and boring, tedious even, but in the best possible way.

Here are 5 that AI will struggle to disrupt 👇

BREAKING: Dutch Minister of Finance to change the paper gains tax.

WE DID IT!!!

Dutch minister of finance: “I don’t think the law can pass in its current form,” Heinen said, expressing understanding for the criticism of the new legislation.

“I think something simply went wrong here and the current law needs to be adjusted.”

I am 100% sure that everything we’ve done over the past weeks, swayed our politicians to admit that they were wrong and rewrite this law for the better.

I’m so proud of all my fellow Dutchies that we’ve made this happen!! 🇳🇱

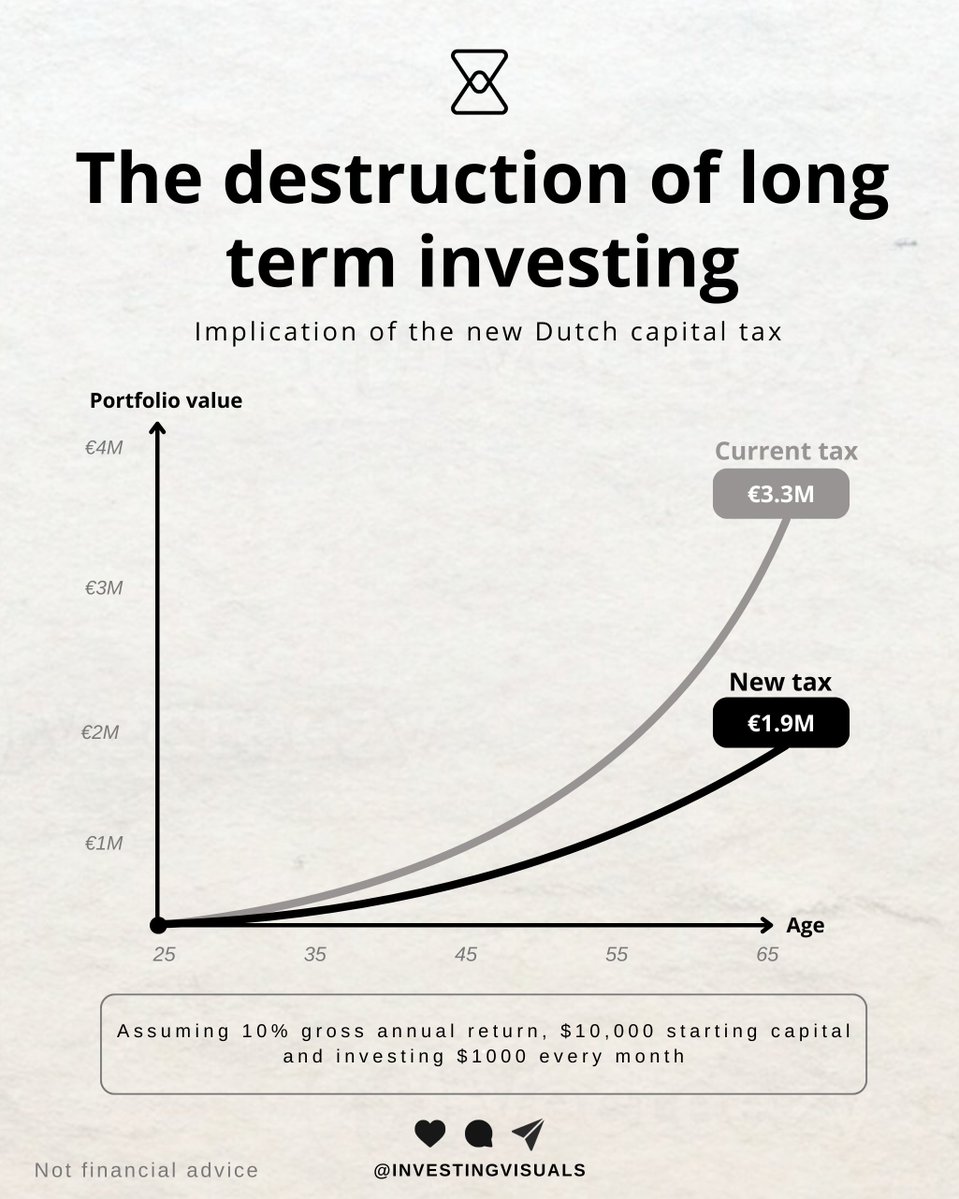

The Dutch government is destroying long term compounding by introducing a 36% tax on unrealized gains.

As a Dutch citizen and long term investor, I’m at a loss for words about the lack of vision behind this new tax. I normally don’t post anything politically related, but what our government is planning to do is disastrous for long term investors.

This is the sad truth.

Most people here start investing to protect themselves against inflation and ever rising pension ages. They’re trying to put hard earned money to work, hoping they can retire before the age of 71. And they had a real shot at that before this bill.

If you started at 25 with €10,000 and contributed €1,000 every month, you could compound to €3,320,000 over 40 years. If you lived prudently, you could retire early and live off it for the rest of your life.

With the new capital tax? After 40 years of compounding, you’d end up at €1,885,000. That’s a €1,435,000 difference.

This tax denies generations the chance of early retirement, punishes those who take risks, and introduces severe liquidity issues for people who have been compounding successfully for years. And to what end? To fill a €2.4 billion tax hole.

I’m beyond words.

If you’re Dutch like me, please share this visual with fellow investors to increase awareness.

Hopefully we can make our politicians understand the severity of this tax, and the breadth and depth of its destructive implications.

~ Jan

Konsorcjum Inwestorów wesprze dalszy rozwój InPost Group!

Konsorcjum złożone z firm: Advent Investment, A&R Investments Ltd., @FedEx Corporation oraz PPF Group zawarły porozumienie w sprawie oferty nabycia wszystkich akcji InPost S.A. po cenie 15,60 EUR za akcję

Transakcja pozwoli wesprzeć kolejny etap rozwoju InPost, w tym kontynuację ekspansji na rynkach europejskich. Współpraca z inwestorami finansowymi i strategicznymi zrzeszonymi w Konsorcjum, którzy doskonale znają naszą działalność oraz specyfikę branży i którzy mają horyzont inwestycyjny pozwalający na budowanie wartości w długim okresie, zapewni nam dostęp do wiedzy, stabilności i zasobów niezbędnych do wykorzystania sprzyjających trendów rynkowych. Wspólnie wzmocnimy naszą sieć i dotrzemy do większej liczby konsumentów, oferując szybkie i elastyczne opcje dostaw oraz kontynuując jednocześnie redefinicję europejskiego sektora e-commerce.

Co ważne, pozostaję w pełni zaangażowany w kierowanie Grupą InPost. Nasza główna siedziba, kadra zarządzająca oraz kluczowe kompetencje innowacyjne pozostaną w Polsce, która nadal będzie stanowić centrum realizacji skutecznej strategii Grupy🇵🇱

Wierzę, że przy wsparciu partnerów możemy w pełni uwolnić potencjał InPost i dalej wzmacniać naszą pozycję wiodącego dostawcy innowacyjnych usług dla sektora e-commerce w Europie Zachodniej.

If you’re a $wise investor, I highly recommend listening to this podcast with the CEO Kristo Käärmann, released a few days ago.

Some takeaways:

Regulators and $wise are aligned. Both want the customer to move money at a low cost in a fair way. This is an underrated competitive advantage.

The shift from B2C to B2B represents a significant growth opportunity. Through Wise’s platform, payments volume can scale efficiently as a white-label solution. At their core, both segments share the same end-user needs: speed, low cost, and transparency.

In the consumer space, Wise currently serves 5% of the market with the remaining using banks for their payment transactions. We are in the early days and Wise has a big runway ahead. 🫡

https://t.co/iz6mYwT5pY