Here's my contrarian take on the BTC price: that we have a lot more to fall later in the year and we will still be well below current prices into late 2027.

Consensus from bulls and bears alike seems to be that we have either reached cycle bottom or need a final drop to reach it. Markets like to make the majority look foolish.

Max pain is not just the usual winter, but rather, a crypto Ice Age that breaks all prior cycle patterns.

(I hope it doesn't happen.)

On the day of the SpaceX IPO, let's remember that there are people who mostly talk for a living, and others who mostly do stuff. The latter are way more important than the former.

Space X just started trading. While I believe Space X to be one of the most successful companies in history, the IPO is a tragedy of the American (and thus Global) financial system. In a better system, it would have gone public at a $500M valuation and the public would have had a 3500x return. Instead, private investors captured that return and exited to the public.

Last year I stopped paying taxes from my paycheck and bought BTC instead.

In April I did my taxes; I paid nothing and waited for them to contact me back.

Today I received notice from IRS that I owe them. I was waiting for this. I am choosing to pay over 36 months instead, leaving the money invested in BTC the whole time. I owe $9,740 but since I am taking 3 years (36 monthly payments) to pay it back I will end up paying $10,915 instead. This equates to about 7.55% APR. I'm doing this because I believe BTC will average better than 7.55%.

If I had owed >$10k I would be able to pay it back over 6 years instead of 3 years. I'll fix that next year.

@sunny051488

The most unbelievable thing about Michael Saylor is that the idea of cycles doesn't enter his framework for Bitcoin purchases. I've never heard of him talk about cycles for this highly cyclical asset.

Even the most rudimentary cycle model would have saved him a lot of risk exposure.

Appreciate @TaikiMaeda2’s transparent, real time declaration of trades and positions. One of the few influencers who puts himself on the line publicly and prospectively instead of only highlighting his winners in hindsight.

Hey if anyone's hiring, please let me know.

My marketable skills include:

- Buying the top before the Hades Candle

- Bullposting the top before the Hades Candle

- Being max exposed before the Hades Candle

- Poor Overall Judgment

- Being Japanese

This is a nice summary of the situation, with a couple of modifications:

* Strategy is contractually allowed to lower the STRC dividend 25 bps on a monthly basis, with some allowance for greater decreases should SOFR fall. But the dividend cannot go below the SOFR rate. Lowering the dividend to the SOFR rate (about 800 bps) would take a long time.

* That said, the market is showing that it wants higher, not lower dividends since STRC is below $100. A lowering of dividends could make the STRC price fall more.

* The biggest counterargument to the "overhang" argument is that Strategy selling $2B of BTC to raise cash would make their obligations much easier to fulfill. They have been buying than that each month, and that amount is less that a single day's volume on Coinbase. In other words, there can't be an overhang because Strategy is too small a player.

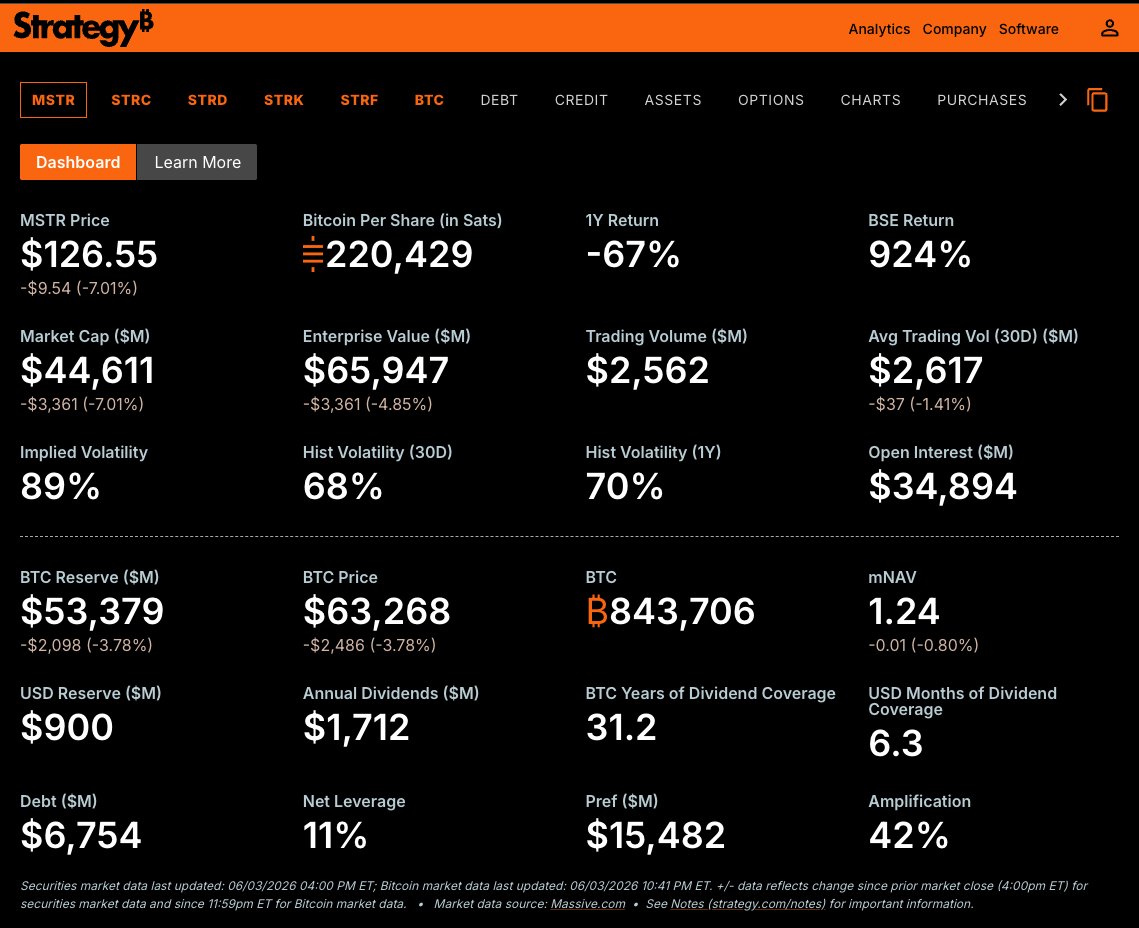

MSTR Summary (As I understand it)

The market basically has an extremely large overhang of a potential BTC seller. Now MSTR has been a big reason why rallies at highs have always continued on longer than it should - it is an essential indicator to track for the health of the bull market - early stage bull = MSTR buys usually was sustained continuous bullish momentum ; late stage bull = MSTR buys would hold price up, before a nuke after the announcement that Saylor has been buying

Now this is potentially unravelling, essentially because the day of reckoning has come - after all, when someone buys, one must ask - how does he get the capital to buy? Saylor has historically funded it through equity financing / convertible notes / term loans / and more recently, preferred equity product financing - and I'll try to explain it simply as how I understand it.

Now for most of the time, equity financing was actually a very sustainable ponzi. Equity had no guarantee of returns. That is a good thing. Of course, this all came at the expense of MSTR shareholders, but the idea that I believe Saylor had, was that "we are selling the stock, to buy something that has more convexity than the stock (BTC), so that, in 10 years, we will end up with a lot more money, and so the stock will be a lot higher" - i.e you're trading short term PA for long term CAGR

This of course assumes a lot of things - 1) that BTC will be higher in 10 years, 2) that BTC has some sort of CAGR, and 3) that stock price will reflect this, and 4) that people will buy the story, and 5) that the market will like it, will reward it (and it has, for the past 4 years)

Now, all's well. This is where we get to the trouble - Saylor launched a bunch of new products recently - STRC / STRD / etc. I'm not an expert in these products, so feel free to correct me where I'm wrong, but these are preferred shares that pay yield. They say: Hey, give me cash. I'll give you yield. This yield varies in order to keep the product at par value ; i.e If today it goes to 90, the yield increases to get people to "buy" it so as to "peg" it there;

I'm not going to go through each product - they all work slightly differently. The rest are fixed yield instead of variable; All you have to understand is at this point, MSTR now began giving out money (i.e having yield)

This is a bad thing and where the story is now. Having obligations means having to spend cash to pay yield, which means, in a company that hinges on an assumption of the 15% CAGR of a magical internet asset with no real cashflows ( other than software biz) - where is the money coming from?

The way I see it, you basically have an extremely huge cloud looming on the horizon. You don't know when the hurricane will start, but you see it. This is enough to prevent BTC from reaching new highs in the first place - it is possible to kick the can down the road, to "look away from the hurricane", but the hurricane is there all the same, just waiting for its reckoning.

He holds $53 BILLION in Bitcoin (Based on Price of 63k), yet only has enough cash for 6 months of dividend coverage (numbers are from https://t.co/Dn0HtZunrC). And back in February they claimed a $2.25 Billion reserve - this reserve has been drawn hard (now it's 900M)

Saylor has 3 ways out. And again - this is just my analysis - I could be missing something:

1. Stop the yield. He can theoretically (since these are all preferreds, correct me if I'm wrong) just stop payments.

2. Somehow finance more $ to pay dividends, either by selling more MSTR, or raising debt.

3. Sell BTC to pay his bills

Now, obviously, the second-order effects of all of these are incredibly bad no matter how you see it.

For 1) if he does that, faith in MSTR would collapse, stock prices would probably go down, STRC goes to Mordor, and maybe he doesn't have to sell BTC, but there are still obligations to pay, so it doesn't fully solve the issue. The thing is - stop paying STRC can be done, but it's like putting a bandaid when your arm gets cut off.

Because what happens here is that (and this is where I'm relying on Claude, who read the offering doc) - he stops the cash from going out, but the obligation still exists - i.e He can stop the payment, but he can't cancel the debt. It's like your landlord coming to you for this month's rent, and you defer it to next month - but you now have to pay two months' worth of rent next month, not just a month's rent

STRC is cumulative - so stopping = you don't pay cash now, but the amount you skipped gets added to a tab and grows. And because STRC is a "Perpetual Stretch Preferred Stock" with perpetual being the key word here, there is no maturity date, it doesn't end, and the only true way to stop it is by buying it back with cash. Else, the dividend just keeps compounding at the back.

Buying back is an option, and according to Claude, the cash redemption price is $101 per share - so $8 Bn if he wanted the whole STRC stack gone. But that's where we come back to the above - he doesn't have the cash!

For 2) It's like rolling your credit card bill. This months bill comes in - you take a new credit card, use it to pay your old one, and for the next month, you're chilling, and you extend the runway. Now if BTC magically goes up to 200k, then you are safe, you can pay your obligations, selling some BTC won't matter.

For 3) This is the worst case scenario. I mean, this is just a doom loop. On 1st June, MSTR already filed a sale of 32 BTC (2.5m), the first strategic / material sale in history. The other sale was in 2022, and that was a tax-loss sale which they bought back immediately. BTC instantly went down by 6-7% on the day, and it's down 12% since then. If they sell more, BTC is just going to go down faster than they would get $ back from selling, and they're basically left holding the bag.

My analysis:

For now, the markets will probably stay at a standstill until this is resolved. Everyone is watching to see what Saylor will do. Again, he owns roughly 4% of all BTC. And what happens if BTC keeps going down? That would be a doom loop playing out. And putting yourself into the mindset of a buyer - why would I buy BTC here, when I know there is a potential seller coming here tomorrow?

I'm reminded of an old joke in the office that our head of trading used to say, that originated on wall street:

A trader thinks that the prices of eggs are going to increase, and so he contacts his broker and asks him to buy 1,000,000 egg futures at $1.70

Sure enough, a week later, the price of egg futures is $2.50, and the trader, happy to ride his winners, places an order for 3,000,000 more egg futures

Next month, at $4.30 a piece, he pats himself on the back and restructures his liquid investments to buy another 10,000,000 egg futures

At the end of the quarter, egg futures are trading at $7, and the trader finally calls up his broker and tells him to sell them all

The broker replies: “To who? You’re the egg man!”

PSA: This is a personal opinion piece written in my individual capacity, not on behalf of or attributable to my employer. It is not investment research, a recommendation, or an offer or solicitation to buy or sell any security or asset.

It does not constitute financial advice and should not be relied upon for any investment decision; readers should do their own research and consult their own advisors. All views are my own as of the date of writing and may change without notice. Factual claims are drawn from public sources and may contain errors or become outdated.

I hold no position, long or short, in BTC, MSTR, or any related security, and have no economic interest in the price of any asset discussed. I receive no compensation from any party in connection with this piece.

The steal is on in California.

In real time.

In front of the world.

Just like in the 2020 Presidential but at least then they had the decency to do it at 3 AM when everyone was asleep.

I lived through the 2nd British Invasion and it was glorious. Adding one more to the list that @nic_carter didn't mention from the 90s: The Verve

My answer is that Anglo civilization has been the creative center of the world for hundreds of years, and the effect is Lindy.

Has anyone ever convincingly explained why Britain was the absolute center of the rock universe in the 60s and 70s and still punched way above its weight in the 80s? The chokehold it had on music culture was just remarkable

60s and 70s:

The Beatles

The Stones

Pink Floyd

Led Zeppelin

Genesis

Yes

Queen

ELO

The Who

The Kinks

Black Sabbath

Supertramp

Eric Clapton

Moody Blues

King Crimson

David Bowie

80s:

The Smiths

New Order

The Cure

The Police

Duran Duran

Dire Straits

Tears for Fears

Iron Maiden

Joy Division

For a relatively small country going through post empire decline the cultural output was just remarkable

It's been a long time coming, but with everyone's current obsession with the macro I've decided to explore S&P 500 cycles during the past 100 years.

I'm calling it the Quartercent Cycles Theory because of the 25 year long cycles in between pauses.

There have been many times that have been deemed as a recession, but I see the true market pauses as the great depression in the 30's, between 66' and 77' and the 2000's dot-com crash to the 2008 housing market crash.

In between these approximately 9 year pauses are 5 different highs which come at certain intervals after the "dawn" which is the final and most devestating correction that begins the next 25-year run.

They are listed by how many years they come from the dawn:

- 6 year top (red)

- 9 year top (orange)

- 12 year top (yellow)

- 15 year top (green)

- 19 year top (blue)

The dates for these tops are further reinforced with Fibonacci time measures between the dawn and the first top of the pause (approx).

Pause periods have two major tops that come about 7 years apart.

This cycles theory has had incredible accuracy with only a few tops not playing out:

- 51' (continued up no correction)

- 54' (continued up no correction)

- 84' (correction came sooner in 83')

What does this mean for now?

If the cycles theory is correct, we have just hit our 15 year high in December 2024. The good news is that previous 15 year high corrections (57' and 84') only lasted a couple of months. By that time frame it could be over soon. It is typical for corresponding highs to act similarly.

The next topping point to watch out for beyond our current is in late 2028.

The next market pause according to the 25 year cycle would be between 2034 and 2043.

A serious correction seems unlikely for quite a while.

Agree with this take. The problem with "only worry about things you can control" is that the world is not split into a stark binary between things you can control and things you cannot.

Stoicism gives you an easy out for goals that are at the very edge of the possible.

Stoicism is popular because apathy is the sickness of our age and stoicism glorifies it. Stoicism is cope for living in a dying society. Stoicism is managed decline. You need to become anti-stoic. You need to become so passionate it’s self-destructive.

The rate is not the rate.

For 400 years, implied vol was flat across strikes. Then Black Monday 1987 taught the market to price tails.

New Crypto Yield Curve: how Aave froze and taught DeFi to price liquidity risk.

Kamino didn't have a credit problem during the Aave-Kelp exploit. It had an equilibrium problem.

New Crypto Yield Curve: DeFi's Diamond-Dybvig moment – why a fully solvent pool can still run.