Hope everyone enjoys a fabulous 4th of July celebration of the 250th anniversary of the founding of this great country. Those of us who are U.S. citizens are so privileged to live here!

However, we cannot become too complacent. Our brilliant founders warned us, including Ben Franklin, who was asked at the conclusion of the Constitutional Convention in Philadelphia whether our new government would be a republic or monarchy, Franklin replied: "A republic if you can keep it."

Today, there are modern leaders who would prefer other forms of government - as they try to move the country towards monarchy/despotism or a "socialist democracy."

Also from Franklin: "When the people begin to think they can vote themselves money, it will herald the end of the republic."

John Adams: “Remember Democracy never lasts long.

It soon wastes, exhausts and murders itself.

There never was a Democracy yet, that did not commit suicide. It is in vain to say that Democracy is less vain, less proud, less selfish, less ambitious or less avaricious than Aristocracy or Monarchy. It is not true in Fact and nowhere appears in history."

For the big spenders in the Executive branch and Congress that have brought us to a $39.3 trillion dollar National Debt, here's a pertinent comment from Scottish historian and author, Alexander Fraser Tytler (1747-1813): “A democracy is always temporary in nature; it simply cannot exist as a permanent form of government. A democracy will continue to exist up until the time that voters discover that they can vote themselves generous gifts from the public treasury. From that moment on, the majority always votes for the candidates who promise the most benefits from the public treasury, with the result that every democracy will finally collapse due to loose fiscal policy, which is always followed by a dictatorship.”

And another quote from Tytler: "The average age of the world's great civilizations has been two hundred years. These nations have progressed through the following sequence: from bondage to spiritual faith, from spiritual faith to great courage, from courage to liberty, from liberty to abundance, from abundance to selfishness, from selfishness to complacency from complacency to apathy, from apathy to dependency, from dependency back to bondage."

A final quote from Charles Louis de Secondat, baron de La Brède et de Montesquieu, a French political philosopher (1689-1755) best known for developing the theory of separation of powers (our founding fathers understood this concept so well): "The deterioration of every government begins with the decay of the principles on which it was founded."

Even though it's absolutely no surprise to see virtually all the Wall Street firms issuing glowing reports today on what is one of (if not the) most ridiculously expensive stock IPO ever (SpaceX - 110x revenues), it doesn't make it any less revolting to see the "analysts" contort themselves coming up with all sorts of justifications to own this.

SpaceX represents “the apex of civilizational ambition, oftentimes expressed in steel and fire, bending the arc of history.”

Don't worry about the valuation because: "a planetary infrastructure company does not compete within existing markets"

Also: SpaceX is “paving the superhighway to the stars.”

Credit to MoffettNathanson (likely not one of the IPO book runners) for stating the truth: "There is simply no credible financial model that can support what is at the time of this writing a roughly $2 trillion valuation."

Do you know what's in your ETF?

https://t.co/24YdNyLqYd

The Declaration rests on a simple principle: we created government to protect our rights, which makes it our employee, not our parent. We pay its bills and are responsible for teaching it to be moral, not the other way around, says Cato’s @TimothySandefur.

The Founders didn't build a government to solve your problems. They built one to stay out of your way.

Thomas Jefferson said it plainly — and 250 years later, it still cuts right to the heart of what America is meant to be.

One of the biggest cons the far-left ever pulled is posturing themselves as the authentic voices of minority voters, when minority voters tend to be far more moderate. Big chunks of the far-left tend to be rich and white.

You’re right, I can’t tell you these things because this is all bs. NYC spends $44k per student. America spends massively on healthcare, poverty, etc. And, of course, Israel isn’t committing genocide and the amount of aid money it receives is a rounding error on what we spend on welfare and entitlement programs. This woman panders to the know-nothing populist left, the way the Benny Johnson crowd panders to the know-nothing right. But at least Johnson’s not going to Congress.

This was Gaza on October 7.

Palestinians were kissing the floor with joy as Hamas paraded dead Jews through the streets.

Remember this the next time you see someone call them the victims.

This is the wall that Egypt built on the border with Gaza to prevent Palestinian refugees.

There are 57 Muslim-majority countries, not a single one has taken any Palestinian refugees. Ever wondered why?

NYC Mayor Mamdani lashed out at Israel yesterday for eliminating Ahmed Wishah, an Al Jazeera “journalist”

Palestinians posted an obituary of Wishah, the journalist 👇🏻

This is not just how you break an economy, this is also how you break a stockmarket bull market.

When @johnauthers was at the FT, he always used to highlight equity yields should be compared to real, not nominal bond yields.

Central banks reported buying 16 tonnes of gold last quarter. The World Gold Council, tracking the actual metal through refineries, puts the real number near 244, roughly fifteen times the official figure. And the buying surged into the worst gold crash since 2013.

Gold fell about 24 percent from its January peak of 5,589 dollars an ounce, on a surging dollar, an oil-driven inflation shock, and a Fed pricing out every rate cut. Western investors read it as the top. Goldman cut its target. Gold ETFs bled for a month and the headlines turned bearish.

The official sector did the opposite. A record 45 percent of central banks now plan to add gold to their own reserves, the highest reading in the survey's history. 89 percent expect global official gold to keep rising. 74 percent expect the dollar's share of reserves to fall. They bought the crash at the highest conviction ever recorded.

The number the press watches is the wrong one. The gold market financial media tracks is Western ETF flows, and they have become a rounding error. This month's celebrated Western ETF recovery was 5 tonnes. Central banks have averaged 1,000 tonnes a year for four years, double the prior decade. One side trades the headline. The other sets the trend, and does not sell.

There is a reason the buying is quiet and relentless at once. Gold is the one reserve asset no government can freeze, no issuer can switch off, and no settlement system can reject. After 2022 proved that dollars and bonds can be made unusable by decree, the assets that cannot be revoked became the ones worth holding. Buying them openly signals the intent to leave, which invites the exact pressure you are hedging against. So the biggest reshaping of reserves in a generation is running mostly unreported, quarter after quarter.

The crash did not break the gold thesis. It sorted the holders. Price-sensitive Western money sold into the decline. Price-insensitive sovereigns bought it at record conviction. The weak hands set the price. The strong hands set the direction.

Ownership stopped meaning control in dollars and bonds. Gold is the one reserve asset where it still does, and central banks are buying it faster than they will admit.

Another private credit fund limits redemptions:

“The firm’s $15bn Apollo Debt Solutions fund pitched to wealthy individual investors reported roughly $2.4bn of withdrawal requests in the most recent period. The fund met less than 30 per cent of the withdrawals it faced in the quarter, capping redemptions at 5 per cent of the value of the vehicle” — Financial Times

#privatecredit #markets #investing #investors

On September 15, 2008, Lehman Brothers filed for bankruptcy, and you were told this was the moment the system "let one fail." A noble act of discipline. Tough love from Washington. Lehman failed because Hank Paulson, a former Goldman Sachs CEO, had personal and political reasons to draw the line at that particular firm on that particular weekend.

Look at what happened on either side of Lehman. Bear Stearns got a $29 billion backstop in March so JPMorgan could swallow it. AIG got $85 billion the day after Lehman died, then billions more, because AIG owed money to the right people (Goldman collected $12.9 billion through the AIG bailout, at par). Fannie and Freddie got nationalized on September 7. Then came the $700 billion TARP, the alphabet soup of Fed lending facilities, and trillions in emergency liquidity. Lehman was not the rule. Lehman was the exception that let everyone pretend a rule existed.

This is what discretionary central planning actually looks like. Not a market clearing bad bets, but a handful of men in a conference room deciding who lives and who dies based on relationships, optics, and the phone calls they took that night. Free market economists have warned about this for a century: once you build a lender of last resort, you do not get neutral rules. You get favoritism dressed as crisis management. The Fed picks winners. Always has.

The real scandal is that Lehman was the single institution forced to obey the law of consequences while everyone around it got a printed-money parachute. Failure is the only honest feedback a market gives. Bad firms holding worthless paper should die, and their creditors should eat the loss. That is how capital gets reallocated to people who do not set fire to it.

The next time someone tells you 2008 proved capitalism needs adult supervision, ask them why the adults rescued every reckless gambler except the one whose CEO Paulson happened to dislike. You will not get a coherent answer. You will get a lecture about systemic risk from the people who built the system.

"A traditional IRA lets you make pretax contributions and taxes the withdrawals. A Roth IRA flips it: after-tax dollars in, tax-free out. The result is similar: Tax the money going in or tax it coming out, but not both.

Trump Accounts do both." https://t.co/gCdSJHzrKt

I still can't wrap my mind around the fact that 6,000 Palestinian terrorists invaded Israel and proudly live-streamed themselves slaughtering Jewish families on October 7th, yet many around the world still believe they are the victims.

Has the world lost its sense of clarity?

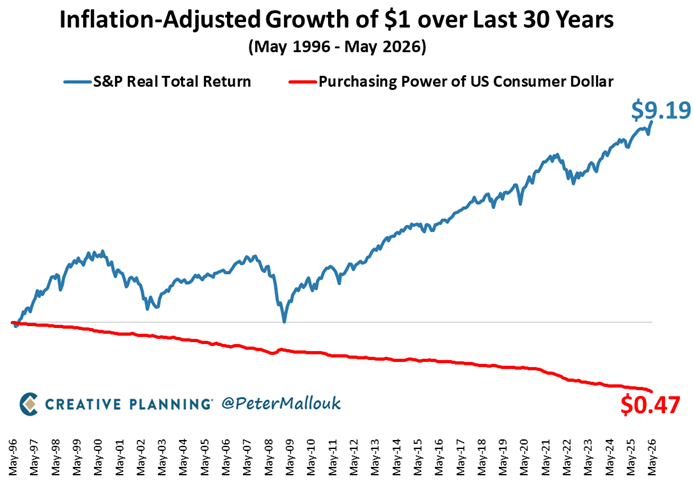

Inflation is the silent thief.

Over the last 30 years, it cut the value of $1 in half.

But $1 invested in the S&P 500 grew to over $9 – AFTER adjusting for higher prices.

That’s the power of ownership.

Andrew Yang wants a tax on computing power. Bill Gates wants robots to pay taxes. A Nobel laureate wants a computer tax to slow down automation. The AI panic is producing terrible tax ideas, argues Cato’s @adamnmichel.

An AI or capital tax would fall on the very workers the policy is intended to help.

https://t.co/xKuxHUYrnV

I feel proud that I'm a self-made man

Though I feel conflicted about it.

I've made the wealth I have the hard way: a LOT of disciplined hard work, saving & investing. I'm proud of that.

But even though I lived in the SF Bay Area for 3 decades, I didn't own real estate or have a major Tech equity windfall

Missing those 2 "easy" paths to wealth was pretty hard to do, when I think about it. So I feel kinda dumb for missing those trains to riches.

I'm not complaining. And I'm very grateful for what I have and how I got here.

And hopefully my story gives others faith they'll get there, too, without having to rely on a winning lottery ticket.

But man, the path sure would have been easier if I'd just learned to love the moneyprinter & bought the f'ing dip during the QE era...

Marine Le Pen, anuncia que luchará contra el Islam:

"Francia tomará todas las medidas necesarias.

Se cerrarán mezquitas radicales y se expulsará a los predicadores del odio.

El salafismo y la Hermandad Musulmana serán liquidados".